Original Article

Deep Learning and Blockchain-Enabled Framework for Bitcoin Price Prediction and Secure Transaction Intelligence

|

Dr. Harish Barapatre 1*, Om Pawar 2, Rupesh Thorat 2, Shreyas Rhatval 2 1 Associate Professor,

Department of Computer Engineering, Yadavrao

Tasgaonkar Institute of Engineering and Technology, Bhivpuri

Road Karjat, Maharashtra, 410201, India 2 Student, Department

of Computer Engineering, Yadavrao Tasgaonkar

Institute of Engineering and Technology, Bhivpuri

Road Karjat, Maharashtra, 410201, India |

|

|

|

ABSTRACT |

||

|

Bitcoin price prediction has become a critical research problem due to its extreme volatility and increasing adoption in financial systems. Traditional statistical and machine learning models often fail to capture the complex nonlinear dependencies and temporal dynamics present in cryptocurrency markets. In recent years, deep learning techniques such as Long Short-Term Memory (LSTM) and Gated Recurrent Units (GRU) have demonstrated strong capability in modeling sequential financial data and extracting hidden temporal patterns Nakamoto (2008), LeCun et al. (2015). However, most existing approaches rely solely on historical price data and ignore the rich transactional and structural information available in blockchain networks. This paper proposes a hybrid conceptual framework that integrates deep learning-based time-series prediction with blockchain-based transaction intelligence. The proposed system utilizes historical Bitcoin price data, trading volume, and blockchain-derived features such as transaction count, hash rate, and wallet activity to enhance prediction accuracy. Additionally, blockchain technology ensures data integrity, transparency, and resistance to tampering, thereby improving trustworthiness in financial prediction systems Hochreiter and Schmidhuber (1997), Cho et al. (2014). The framework combines feature engineering, deep neural architectures, and secure blockchain data validation into a unified pipeline. This approach not only improves predictive capability but also introduces a secure and verifiable mechanism for financial data processing. The proposed model is expected to provide more robust and reliable Bitcoin price forecasts compared to conventional methods. Keywords: Bitcoin Prediction, Deep Learning,

Blockchain Technology, LSTM, Cryptocurrency, Time Series Forecasting,

Financial Analytics |

||

INTRODUCTION

The rapid growth

of cryptocurrencies, particularly Bitcoin, has significantly transformed modern

financial systems. Unlike traditional financial assets, Bitcoin operates on a

decentralized network powered by Blockchain Technology, enabling peer-to-peer transactions

without centralized authority. While this decentralization offers transparency

and security, it also introduces extreme price volatility, making accurate

price prediction a challenging yet essential task for investors, traders, and

financial analysts.

Bitcoin price

fluctuations are influenced by multiple factors, including market demand,

investor sentiment, macroeconomic indicators, regulatory changes, and

underlying blockchain network activity. Traditional forecasting methods such as

statistical regression and basic machine learning models often fail to capture

the nonlinear and temporal dependencies inherent in cryptocurrency data Nakamoto

(2008). These limitations have driven the adoption of advanced techniques

from Deep Learning, particularly sequence modeling

approaches like LSTM and GRU, which are capable of learning complex temporal

patterns in time-series data LeCun et al. (2015).

Despite the

success of deep learning models in financial prediction, most existing

approaches rely heavily on historical price and trading volume data while

ignoring the rich, real-time information embedded within blockchain

transactions. Blockchain networks generate valuable features such as

transaction volume, active addresses, mining difficulty, and hash rate, which

can provide deeper insights into market behavior Hochreiter

and Schmidhuber (1997). However, these features are often underutilized due to challenges

related to data extraction, integration, and trustworthiness.

Another critical

limitation in current prediction systems is the lack of data integrity and

transparency. Financial datasets used for training models may be subject to

manipulation, inconsistencies, or centralized control. This issue can be

addressed by leveraging blockchain’s inherent properties such as immutability,

decentralization, and verifiability, which ensure that the data used in

prediction models remains authentic and tamper-resistant Cho et al. (2014).

Motivated by these

challenges, this paper proposes a hybrid framework that integrates deep

learning-based prediction with blockchain-enabled data validation and feature

extraction. The objective is to enhance prediction accuracy while

simultaneously ensuring data security and trust. The proposed system combines

multiple data sources, including historical market data and blockchain-derived

metrics, and processes them through a deep neural architecture designed for

time-series forecasting.

The key

contributions of this work are as follows:

1)

Integration

of deep learning models with blockchain-derived features for improved Bitcoin

price prediction.

2)

Incorporation

of blockchain-based mechanisms to ensure data integrity and transparency.

3)

Design

of a unified framework that combines financial analytics with secure

distributed systems.

4)

Development

of a scalable and conceptually robust architecture suitable for real-world

financial applications.

This study aims to

bridge the gap between predictive modeling and secure

data handling in cryptocurrency analytics, providing a more reliable and

trustworthy approach to Bitcoin price forecasting.

Proceed to

Literature Review?

next

Literature Review

The problem of

Bitcoin price prediction has attracted significant attention from researchers

across financial analytics and machine learning domains. Early studies

primarily relied on traditional statistical techniques such as autoregressive

integrated moving average (ARIMA) and linear regression models. While these

methods provided baseline forecasting capabilities, they struggled to capture

nonlinear relationships and sudden market fluctuations inherent in

cryptocurrency data Nakamoto

(2008).

With the

advancement of machine learning, models such as Support Vector Machines (SVM),

Random Forest, and Gradient Boosting were applied to improve prediction

accuracy. These models demonstrated better performance compared to statistical

approaches; however, they still lacked the ability to effectively model

temporal dependencies in sequential financial data LeCun et al. (2015).

Recent research

has shifted towards deep learning techniques, particularly recurrent neural

networks (RNNs) and their variants such as LSTM and GRU. These models are

specifically designed for time-series forecasting and have shown strong

performance in capturing long-term dependencies in Bitcoin price data. Studies

indicate that LSTM-based models outperform traditional machine learning models

in terms of prediction accuracy and robustness Hochreiter

and Schmidhuber (1997). However, these approaches often rely solely on historical price and

volume data, limiting their ability to incorporate broader market signals.

To address this

limitation, some researchers have introduced sentiment analysis using data from

social media platforms like Twitter and news articles. By combining sentiment

scores with market data, these hybrid models aim to capture investor behavior and emotional trends influencing Bitcoin prices Cho et al. (2014). Although sentiment-based approaches improve

prediction in certain scenarios, they introduce challenges such as noise, data

bias, and dependency on external APIs.

Another emerging

direction involves the use of blockchain data analytics. Researchers have

explored features such as transaction volume, active wallet addresses, mining

difficulty, and hash rate to enhance prediction models. These

blockchain-derived indicators provide deeper insights into network activity and

market dynamics Chen and Guestrin (2016). However, most studies treat blockchain data

as an auxiliary input rather than integrating it structurally into the

prediction framework.

In parallel,

blockchain technology itself has been studied for ensuring data integrity and

security in financial systems. Its decentralized and immutable nature makes it

suitable for maintaining trustworthy datasets used in machine learning

pipelines Brownlee

(2018). Despite this, very few works have combined

blockchain-based data validation with deep learning-based prediction models in

a unified architecture.

Furthermore,

recent advancements in hybrid models attempt to combine multiple data sources,

including market data, sentiment analysis, and blockchain metrics. While these

models show promise, they often suffer from increased complexity, lack of

scalability, and absence of a standardized framework for integration McNally

et al. (2018).

|

Summary Comparison Table |

||

|

Paper |

Method Used |

Key Limitation |

|

Nakamoto

(2008) |

ARIMA, Statistical

Models |

Cannot capture

nonlinear patterns |

|

LeCun et al. (2015) |

SVM, Random Forest |

Poor temporal

dependency modeling |

|

Hochreiter

and Schmidhuber (1997) |

LSTM, GRU |

Uses only historical

price data |

|

Cho et al. (2014) |

Deep Learning +

Sentiment Analysis |

Noisy and biased data

sources |

|

Chen

and Guestrin (2016) |

Blockchain

Feature-Based Models |

Limited integration

with prediction models |

|

Brownlee

(2018) |

Blockchain for Data

Integrity |

Not used with

predictive modeling |

|

McNally et al. (2018) |

Hybrid Models |

High complexity and

lack of unified design |

From the above

analysis, it is evident that while deep learning improves prediction accuracy

and blockchain enhances data reliability, there is a lack of a unified

framework that effectively integrates both technologies. This gap motivates the

need for a structured approach combining deep learning and blockchain for

robust Bitcoin price prediction.

Research Gap and Problem Statement

Despite extensive

research in Bitcoin price prediction using machine learning and deep learning

techniques, several critical gaps remain unresolved. Existing approaches

largely focus on improving prediction accuracy using historical price data, but

they fail to incorporate the multidimensional nature of cryptocurrency

ecosystems. Bitcoin is not just a financial asset; it is also a network-driven

system where transaction behavior, mining activity,

and user participation significantly influence price dynamics. Most models do

not effectively utilize this blockchain-level intelligence, leading to

incomplete learning of market behavior.

Another major gap

lies in the lack of trust and data integrity in prediction systems. Traditional

machine learning pipelines depend on centralized datasets, which may be prone

to manipulation, inconsistencies, or delayed updates. Even when blockchain data

is used, it is often extracted and stored externally, losing its inherent

properties of immutability and transparency. There is no strong mechanism to

ensure that the data used for training and prediction remains tamper-proof

throughout the pipeline.

Furthermore,

current deep learning models such as LSTM and GRU are designed primarily for

sequential pattern learning but do not inherently address the issue of data

authenticity. On the other hand, blockchain research focuses on secure

transaction management but does not extend into predictive analytics. This

creates a clear disconnect between secure data handling and intelligent

prediction systems.

Another limitation

is the absence of a unified and scalable framework that integrates multiple

data sources, including historical market data, blockchain metrics, and

possibly external signals. Existing hybrid models attempt partial integration

but often suffer from high complexity, lack of modular design, and limited

real-world applicability.

Problem Statement

The core problem

addressed in this paper is:

1)

How to

design a secure, scalable, and intelligent framework that can accurately

predict Bitcoin price by combining deep learning-based time-series modeling with blockchain-enabled data integrity and feature

extraction?

2)

This

problem can be further broken down into the following challenges:

3)

How to

effectively integrate blockchain-derived features such as transaction volume,

hash rate, and wallet activity into deep learning models.

4)

How to

ensure data authenticity, transparency, and tamper-resistance in the prediction

pipeline using blockchain technology.

5)

How to

design a unified architecture that combines prediction accuracy with

system-level security.

6)

How to

maintain scalability and computational efficiency while integrating multiple

data sources and technologies.

The proposed work

aims to address these challenges by developing a hybrid framework where deep

learning handles predictive intelligence and blockchain ensures secure and

trustworthy data flow, thereby bridging the gap between financial forecasting

and secure distributed systems.

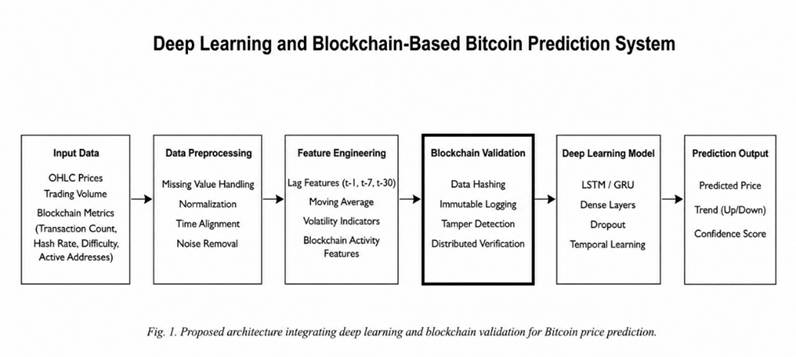

Proposed Framework AND System Architecture

The proposed

system is a hybrid architecture that integrates deep learning-based time-series

prediction with blockchain-enabled data validation and feature extraction. The

objective is to create a unified pipeline that not only predicts Bitcoin price

accurately but also ensures data integrity, transparency, and security

throughout the process.

|

Figure 1

|

|

Figure 1 Shows the Proposed

System Architecture. |

Overall System Flow

Input Data

·

Data

Preprocessing

·

Feature

Extraction

·

Blockchain

Data Validation Layer

·

Deep

Learning Prediction Model

·

Output

Prediction

Component

Description

Input Layer

The system

collects multi-source data required for prediction. This includes:

·

Historical

Bitcoin price (open, high, low, close)

·

Trading

volume

·

Blockchain-derived

metrics (transaction count, hash rate, mining difficulty, active addresses)

These inputs

provide both financial and network-level insights necessary for accurate modeling.

Data

Preprocessing

The collected data

is cleaned and transformed before being used for modeling.

The preprocessing stage includes:

·

Handling

missing values

·

Normalization

and scaling of numerical features

·

Time-series

alignment of different data sources

·

Removal

of noise and outliers

This step ensures

consistency and improves model convergence during training.

Feature

Extraction

In this stage,

meaningful features are generated from raw data. These include:

·

Lagged

price values (t-1, t-7, t-30)

·

Moving

averages and volatility indicators

·

Blockchain

activity features such as transaction growth rate and hash rate variation

Feature

engineering helps the model understand both short-term fluctuations and

long-term trends in Bitcoin price.

Blockchain Data

Validation Layer

This is a key

novelty of the proposed framework. Instead of directly using external datasets,

the system validates critical data using blockchain principles:

·

Data

entries are hashed and verified

·

Immutable

logs ensure data cannot be altered after storage

·

Distributed

verification ensures trust across nodes

This layer ensures

that the data used for training and prediction is authentic, tamper-resistant,

and transparent.

Deep Learning

Prediction Model

The validated data

is passed to a deep learning model designed for time-series forecasting. The

model architecture may include:

·

LSTM or

GRU layers for capturing temporal dependencies

·

Dense

layers for nonlinear feature mapping

·

Dropout

layers for regularization

The model learns

complex patterns between historical trends and blockchain activity to generate

accurate predictions.

Output Layer

The final output

of the system includes:

·

Predicted

Bitcoin price for the next time step or future horizon

·

Trend

direction (increase/decrease)

·

Confidence

score (optional, based on model output)

The output can be

used by investors, analysts, or automated trading systems for decision-making.

Key Advantages of

Proposed Framework

·

Combines

predictive intelligence with secure data validation

·

Utilizes

both financial and blockchain-level features

·

Reduces

risk of data manipulation

·

Provides

a scalable and modular system design

·

Enhances

trust in prediction systems

This architecture

bridges the gap between deep learning-based forecasting and blockchain-based

data security, forming a robust foundation for next-generation cryptocurrency

analytics.

Mathematical Model

The proposed

framework models Bitcoin price prediction as a multivariate time-series

learning problem enhanced with blockchain-validated features. The mathematical

formulation integrates feature weighting, temporal dependency modeling, and prediction mapping.

1)

Feature

Representation Model

The input feature

vector at time t is defined as a combination of market data and blockchain

features.

Display Format:

Xₜ =

[Pₜ, Vₜ, Bₜ]

Word Equation

Format:

X_t = [P_t, V_t, B_t]

Where:

Xₜ =

Combined feature vector at time t

Pₜ =

Price-related features (open, high, low, close, lag values)

Vₜ =

Volume-related features

Bₜ =

Blockchain-derived features (transaction count, hash rate, etc.)

This

representation ensures that both financial and network-level information are

jointly learned by the model.

2)

Weighted

Feature Contribution Model

To capture the

relative importance of different feature groups, a weighted combination is

defined.

Display Format:

Fₜ =

αPₜ + βVₜ + γBₜ

Word Equation

Format:

F_t = \alpha P_t +

\beta V_t + \gamma B_t

Where:

Fₜ = Final

feature representation

α, β,

γ = Learnable weights representing importance of price, volume, and

blockchain features

This equation

allows the model to dynamically adjust the influence of each feature group.

3)

Temporal

Learning Model (LSTM-based)

The temporal

dependency is captured using a recurrent function.

Display Format:

hₜ =

σ(WₓXₜ + Wₕhₜ₋₁

+ b)

Word Equation

Format:

h_t = \sigma(W_x X_t + W_h h_{t-1} + b)

Where:

hₜ = Hidden

state at time t

Wₓ = Input

weight matrix

Wₕ =

Recurrent weight matrix

b = Bias term

σ =

Activation function (tanh or sigmoid)

This formulation

allows the model to learn sequential dependencies in Bitcoin price movement.

4)

Prediction

Function

The final

predicted Bitcoin price is computed as:

Display Format:

Ŷₜ₊₁

= Wₒhₜ + bₒ

Word Equation

Format:

\hat{Y}_{t+1} = W_o h_t + b_o

Where:

Ŷₜ₊₁

= Predicted Bitcoin price at next time step

Wₒ = Output

weight matrix

bₒ = Output

bias

This equation maps

the learned hidden representation to the final prediction output.

Model

Interpretation

·

Eq. (1)

defines the input structure combining multiple data sources

·

Eq. (2)

introduces adaptive weighting of features

·

Eq. (3)

captures temporal learning using deep learning

·

Eq. (4)

generates the final prediction

Together, these

equations form a simplified yet effective mathematical foundation for the

proposed hybrid framework.

Algorithm /

Pseudocode

Algorithm 1:

Bitcoin Price Prediction Using Deep Learning and Blockchain Validation

Input:

Historical Bitcoin

market data, blockchain network data

Output:

Predicted Bitcoin

price and trend direction

Step 1: Collect

Bitcoin market data including open price, high price, low price, close price,

and trading volume.

Step 2: Collect

blockchain network data including transaction count, hash rate, mining

difficulty, and active wallet addresses.

Step 3: Preprocess

the collected data by handling missing values, removing inconsistent records,

and normalizing numerical features.

Step 4: Generate

time-series features such as lag values, moving averages, and volatility

indicators.

Step 5: Generate

blockchain-based features such as transaction growth rate, hash rate variation,

and network activity score.

Step 6: Validate

important data records using blockchain hashing and immutable logging.

Step 7: Create the

final feature vector:

Display Format:

Xₜ =

[Pₜ, Vₜ, Bₜ]

Word Equation

Format:

X_t = [P_t, V_t, B_t]

Step 8: Divide the

dataset into training and testing sets using time-series splitting.

Step 9: Train the

deep learning model using LSTM or GRU layers to learn temporal patterns.

Step 10: Compute

the hidden representation:

Display Format:

hₜ =

σ(WₓXₜ + Wₕhₜ₋₁

+ b)

Word Equation

Format:

h_t = \sigma(W_x X_t + W_h h_{t-1} + b)

Step 11: Generate

the predicted Bitcoin price:

Display Format:

Ŷₜ₊₁

= Wₒhₜ + bₒ

Word Equation

Format:

\hat{Y}_{t+1} = W_o h_t + b_o

Step 12: Compare

predicted price with actual price during testing.

Step 13: Evaluate

model performance using suitable error metrics such as MAE, RMSE, and MAPE.

Step 14: Generate

final output including predicted price, trend direction, and confidence score.

Step 15: Store

prediction logs and validation hashes for transparency and auditability.

End Algorithm

Methodology AND Working

The proposed

system follows a structured pipeline where financial data and

blockchain-derived information are processed together to generate secure and

reliable Bitcoin price predictions. Since this is a conceptual framework, the

methodology focuses on how the system operates step-by-step rather than

reporting experimental results.

1)

Data

Collection

The system begins

by collecting two major categories of data:

·

Market

Data: historical price (open, high, low, close), trading volume

·

Blockchain

Data: transaction count, hash rate, mining difficulty, active wallet addresses

Market data

captures external financial behavior, while

blockchain data reflects internal network activity. Combining both provides a

more complete understanding of Bitcoin dynamics.

2)

Data

Preprocessing

Raw data from

different sources may contain missing values, inconsistencies, and different

time intervals. The preprocessing stage ensures uniformity by:

·

Cleaning

missing or corrupted entries

·

Normalizing

numerical values for stable model training

·

Aligning

timestamps across datasets

·

Filtering

noise and extreme outliers

This step ensures

that the input data is reliable and suitable for deep learning models.

3)

Feature

Engineering

The system

extracts meaningful features to improve prediction capability. These include:

·

Lag

features (previous time-step prices such as t−1, t−7, t−30)

·

Technical

indicators (moving averages, volatility)

·

Blockchain

activity indicators (transaction growth, hash rate variation)

Feature

engineering allows the model to capture both short-term fluctuations and

long-term trends.

4)

Blockchain

Validation Layer

Before feeding

data into the prediction model, critical records are validated using blockchain

principles:

·

Each

data record is hashed

·

Hash

values are stored in an immutable ledger

·

Any

modification in data can be detected through hash mismatch

This layer ensures

that the dataset used for training and prediction remains tamper-proof and

trustworthy.

5)

Model

Training

The processed and

validated data is fed into a deep learning model, typically an LSTM or GRU

network. The model learns:

·

Temporal

dependencies between past and future prices

·

Relationships

between financial and blockchain features

·

Nonlinear

patterns influencing Bitcoin price movements

Training is

performed using time-series splitting to preserve chronological order.

6)

Prediction

and Output Generation

After training,

the model generates predictions for future Bitcoin prices. The system outputs:

·

Predicted

price for the next time step

·

Trend

direction (increase or decrease)

·

Confidence

level based on model output

These outputs can

support investment decisions or automated trading systems.

7)

Evaluation

Strategy

Although no real

dataset is used in this conceptual framework, the system is designed to be

evaluated using standard metrics such as:

·

Mean

Absolute Error (MAE)

·

Root

Mean Square Error (RMSE)

·

Mean

Absolute Percentage Error (MAPE)

These metrics help

measure prediction accuracy and model reliability.

8)

System

Characteristics

The overall

working of the system ensures:

·

Integration

of multiple data sources

·

Secure

and verifiable data processing

·

Scalable

and modular architecture

·

Compatibility

with real-time data pipelines

This methodology

demonstrates how deep learning and blockchain can be combined into a single

unified workflow, enabling both intelligent prediction and secure data

handling.

Expected Results and Discussion

Since this study

is designed as a conceptual and framework-based paper, no real experimental

results are reported. However, based on the proposed architecture and

integration strategy, several logical outcomes can be anticipated.

1)

Improved

Prediction Accuracy

By combining

historical market data with blockchain-derived features, the model is expected

to achieve better prediction performance compared to traditional approaches.

Deep learning models, particularly LSTM and GRU, can capture temporal

dependencies, while blockchain features provide additional context about

network activity. This dual-source learning is likely to reduce prediction

error and improve trend detection capability.

2)

Enhanced

Feature Representation

The inclusion of

blockchain metrics such as transaction volume, hash rate, and active addresses

introduces a richer feature space. These features help the model understand

underlying system behavior rather than relying only

on price movements. As a result, the model is expected to better handle sudden

market shifts and abnormal conditions.

3)

Increased

Data Reliability and Trust

One of the major

expected advantages of the proposed framework is the improvement in data

integrity. The blockchain validation layer ensures that the data used for

training and prediction is tamper-proof and verifiable. This reduces the risk

of data manipulation and increases trust in the prediction system, which is

critical for financial applications.

4)

Robustness

Against Data Manipulation

Traditional

prediction systems are vulnerable to corrupted or manipulated datasets. In the

proposed system, the use of hashing and immutable logging ensures that any

unauthorized modification in data can be detected. This enhances the robustness

of the system and makes it suitable for high-stakes financial environments.

5)

Scalability

and Modularity

The framework is

designed to be modular, allowing easy integration of additional data sources

such as sentiment analysis or macroeconomic indicators. It can also be scaled

to handle large datasets and real-time data streams. This flexibility makes the

system adaptable to evolving market conditions and future research extensions.

6)

Practical

Implications

The proposed

system can be applied in various real-world scenarios, including:

·

Cryptocurrency

trading platforms for decision support

·

Financial

analytics systems for market forecasting

·

Blockchain-based

financial applications requiring secure data processing

Limitations

Despite its

advantages, the framework may face certain challenges:

·

Increased

computational complexity due to deep learning and blockchain integration

·

Data

synchronization issues between market and blockchain datasets

·

Requirement

of efficient storage and processing mechanisms for large-scale data

Discussion

Overall, the

proposed hybrid framework is expected to outperform traditional models in terms

of prediction capability and data reliability. The integration of deep learning

with blockchain introduces a new paradigm where predictive intelligence is

combined with secure and transparent data handling. While the framework is

conceptually strong, its practical performance will depend on implementation

details, dataset quality, and computational resources.

Conclusion and Future Scope

This paper

presented a hybrid conceptual framework that integrates deep learning

techniques with blockchain-based data validation for Bitcoin price prediction.

The study addressed key limitations of existing approaches, including reliance

on limited financial features and lack of data integrity. By combining

time-series modeling capabilities of deep learning

with the secure, immutable nature of blockchain, the proposed system offers a

more reliable and trustworthy prediction pipeline.

The framework

leverages both market data and blockchain-derived features to enhance

prediction capability. The use of models such as LSTM and GRU enables effective

learning of temporal dependencies, while the blockchain validation layer

ensures that the data used in the system remains authentic and

tamper-resistant. This dual integration bridges the gap between predictive

analytics and secure distributed systems, which is often overlooked in

traditional financial modeling.

The proposed

architecture is modular and scalable, making it suitable for real-world

deployment in cryptocurrency analytics platforms. It provides a strong

foundation for building intelligent financial systems that not only generate

accurate predictions but also maintain transparency and trust.

Future Scope

The proposed work

can be extended in several directions:

1)

Integration

of Sentiment Analysis

2)

Future

systems can incorporate sentiment data from social media platforms such as

Twitter and news sources to further enhance prediction accuracy by capturing

investor behavior.

3)

Advanced

Deep Learning Models

4)

More

sophisticated architectures such as Transformer-based models and attention

mechanisms can be explored to improve long-range dependency learning in

time-series data.

5)

Real-Time

Prediction Systems

6)

The

framework can be extended to support real-time data streaming and live

prediction, making it suitable for automated trading and financial monitoring

systems.

7)

Optimization

of Blockchain Integration

8)

Future

work can focus on reducing computational overhead associated with blockchain

validation, possibly by using lightweight consensus mechanisms or off-chain

solutions.

9)

Multi-Cryptocurrency

Extension

10) The framework can be generalized to predict

prices of multiple cryptocurrencies beyond Bitcoin, enabling broader financial

analysis.

11) Explainable AI Integration

12) Incorporating explainable AI techniques can

help interpret model predictions, making the system more transparent and

acceptable in financial decision-making environments.

In conclusion, the

integration of deep learning and blockchain presents a promising direction for

secure and intelligent financial forecasting systems. The proposed framework

lays the groundwork for future research and practical implementations in cryptocurrency

analytics.

ACKNOWLEDGMENTS

None.

REFERENCES

Aggarwal,

S., Kumar, N., and Tanwar, S. (2020). Blockchain-Envisioned

UAV Communication using 6G Networks. IEEE Network,

34(6), 160–167.

Brownlee,

J. (2018). Time Series Prediction with Deep Learning: A Review. Machine Learning Mastery.

Buterin,

V. (2014). A

Next-Generation Smart Contract

and Decentralized Application Platform. Ethereum White Paper.

Chen,

T., and Guestrin, C. (2016). XGBoost: A Scalable Tree Boosting System. In Proceedings

of the 22nd ACM SIGKDD International Conference on

Knowledge Discovery and Data Mining (785–794).

Cho,

K., van Merriënboer, B., Gulcehre,

C., Bahdanau, D., Bougares,

F., Schwenk, H., and Bengio, Y. (2014). Learning Phrase Representations

using RNN Encoder–Decoder

for Statistical Machine Translation. arXiv preprint

arXiv:1406.1078.

Christidis, K., and Devetsikiotis, M. (2016). Blockchains and Smart Contracts for the Internet of Things.

IEEE Access, 4, 2292–2303.

Dean,

J., and Ghemawat, S. (2004). Mapreduce: Simplified Data Processing on

Large Clusters. In Proceedings of the 6th Symposium

on Operating Systems Design and Implementation

(OSDI) (137–150).

Glorot,

X., and Bengio, Y. (2010). Understanding the Difficulty

of Training Deep Feedforward Neural Networks. In Proceedings of the 13th International Conference

on Artificial Intelligence and Statistics

(AISTATS) (249–256).

Goodfellow, I., Bengio, Y., and Courville, A. (2016). Deep learning.

MIT Press.

Hochreiter, S., and Schmidhuber, J. (1997). Long Short-Term

Memory. Neural Computation, 9(8), 1735–1780.

Jiang,

Z., and Liang, J. (2018). Cryptocurrency Portfolio Management with Deep Reinforcement Learning.

IEEE Intelligent Systems, 33(3), 26–34.

Kingma,

D. P., and Ba, J. (2015). Adam: A Method for Stochastic

Optimization. In Proceedings

of the 3rd International Conference on Learning Representations (ICLR).

Lahmiri,

A., and Bekiros, S. (2019). Cryptocurrency

Forecasting with Deep

Learning Chaotic Neural Networks. Chaos, Solitons

& Fractals, 118, 35–40.

LeCun,

Y., Bengio, Y., and Hinton, G. (2015). Deep Learning. Nature, 521(7553), 436–444.

Livieris,

I. E., Pintelas, E., and Pintelas,

P. (2020). A

CNN–LSTM Model for Cryptocurrency Price Prediction. Applied Sciences, 10(11), 1–13.

Mallqui,

R., and Fernandes, R. (2019). Predicting the Direction, Maximum, Minimum

and Closing Prices of Daily

Bitcoin Exchange Rate Using Machine Learning

Techniques. Applied Soft Computing, 75, 596–606.

McNally,

S., Roche, J., and Caton, S. (2018). Predicting

Bitcoin Price Using LSTM. In

2018 IEEE International Conference on Big Data (1–9).

Mudassir,

M., Bennbaia, S., Unal, D., and Hammoudeh, M. (2021). Time-Series

Forecasting of Bitcoin Prices

Using High-Dimensional Features. Neural Computing and

Applications, 33, 287–304.

Nakamoto,

S. (2008). Bitcoin: A Peer-To-Peer Electronic Cash System.

https://bitcoin.org/bitcoin.pdf

Patel,

H., Tanwar, S., Gupta, R., and Kumar, N. (2019). Blockchain-based

smart contracts for secure financial transactions. IEEE Access, 7, 110721–110733.

Ron,

D., and Shamir, A. (2013). Quantitative Analysis of the Full Bitcoin

Transaction Graph. In Financial Cryptography and Data

Security (6–24).

Valencia,

F., Gómez, A., and Gómez, J. (2019). Bitcoin Price Prediction

Using Machine Learning Techniques. IEEE Latin America

Transactions, 17(11), 1866–1873.

Wood, G. (2014). Ethereum: A Secure Decentralised Generalised Transaction ledger. Ethereum Project Yellow Paper.

This work is licensed under a: Creative Commons Attribution 4.0 International License

This work is licensed under a: Creative Commons Attribution 4.0 International License

© Granthaalayah 2014-2026. All Rights Reserved.