|

|

|

|

WORKING CAPITAL MANAGEMENT - IT’S IMPACT ON LIQUIDITY AND PROFITABILITY - A STUDY OF KERALA MINERALS AND METALS LTDDr. Sunilraj N.V *1

|

|

|

|

Article Type: Case Study

Article Citation: Dr. Sunilraj N.V.

(2020). WORKING CAPITAL MANAGEMENT - IT’S IMPACT ON LIQUIDITY AND PROFITABILITY

- A STUDY OF KERALA MINERALS AND METALS LTD. International Journal of Research

-GRANTHAALAYAH, 8(5), 199-207. https://doi.org/10.29121/granthaalayah.v8.i5.2020.82s

Received Date: 13 May 2020

Accepted Date: 31 May 2020

Keywords:

Current Assets

Working Capital

Return on Capital Employed

Liquidity

Profitability

ABSTRACT

Working capital management involves the various steps for the proper management of current assets and current liabilities which avoids the risk of a shortage of funds for meeting short-term obligations and eliminates the blocking of funds in current assets on the other hand. The present study makes an attempt to give a conceptual insight on working capital management and assess its impact on liquidity and profitability of Kerala Minerals and Metals Ltd. A proper tradeoff between profitability and liquidity is necessary for every enterprise to survive in any kind of environment. The study also made an attempt to analyse the liquidity and profitability position of KMML. For this, correlation and spearman’s rank has been used. The study covers ten-year data from 2009-10 to 2018-19. The correlation and spearman’s ranking method exhibits a weak correlation and negative relationship between liquidity and profitability. The Motaal’s test has also been applied to test the liquidity position. The liquidity ratios such as the current ratio and liquid ratios are higher than the benchmark which means that the liquidity position is good. The study indicates that the liquidity position of the enterprise has enhanced over the period of study.

1. INTRODUCTION

In the era of modern competitive world, it has become a challenge to maintain financial strength of business houses on a day to day basis. Every enterprise wishes to make out themselves financially better placed. The attributes of financial discipline such as liquidity, profitability and solvency can be ensured thorough the efficient practicing of the principles of working capital management. Working capital is quite essential in every enterprise for supporting and carrying out the routine activities of the enterprise. The results of many empirical studies indicate that inefficient handling of working capital as one among the root causes of industrial backwardness or sickness. Therefore, in order to achieve financial soundness, an organiastion must have efficient management of working capital in place.

Fundamentally, two concepts are there for working capital, namely, the operating cycle concept and balance sheet approach. The concept of operating cycle supports the operational activities of the enterprise whereas the balance sheet concept includes the gross and net working capital. The total amount of all the investments in the current assets is known as the gross working capital concept. Net Working Capital is the excess of current assets over current liabilities. Operating cycle is the period taken for the conversion of raw material into cash. The different stages involved in this process are the conversion of raw material-work in progress-finished goods-sales-debtors-cash.

The most common problem which is confronting a financial manager is to strike a balance between liquidity and profitability. Thus, for ensuring liquidity in an organisation, forecasting and management of both inflow and outflow of cash are very much necessary.

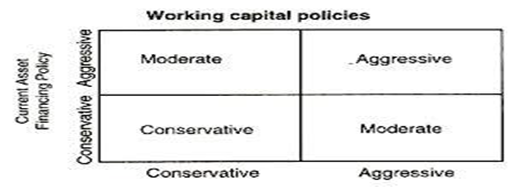

1.1. WORKING CAPITAL POLICIES

All business houses have to manage its working capital strictly in order to meet its short-term fund requirements. As the firm grows, it should have the alertness about the amount of investment in the working capital. Effective policies on working capital management can be framed by the enterprises to operate their business efficiently. A company shall frame separate polices on the different constituents of working capital.

1.1.1. AGGRESSIVE STRATEGY

This strategy completely concentrates on the profitability part of the enterprise. It is often called high profit, high risk approach. Here, all the funds from fixed sources are mainly invested in the fixed assets and no buffer is kept for the working capital requirements.

1.1.2. CONSERVATIVE STRATEGY

Under this approach, a major portion of the working capital is financed with the help of funds from long term sources and is characterized by low profit and low risk. Here, the firms aim to play safe.

1.1.3. MODERATE STRATEGY

In this strategy also, a portion of the long-term funds are employed in the different constituents of working capital and is featured by moderate risk and returns. This approach is a combination of both the aggressive and conservative policies. So it is often considered as a midway approach between conservative and aggressive approaches.

Liquidity and profitability are the two major hurdles for any organisation to deal with in the competitive business world. As generally accepted, these liquidity and profitability decisions are conflicting and inverse to each other for the finance department and for organisations. Liquidity means the capability of an enterprise to pay its financial obligations whenever it arises. Profitability means the ability of an enterprise to earn maximum profit with the use of capital employed. If an enterprise keeps enough funds to maintain liquidity, it will lower the profitability of the enterprise; and on the other hand it goes for more profit by investing all its funds the firm will find it difficult to meet its obligations. Lack of liquidity in certain situations will lead the enterprise to insolvency. Therefore, financial managers have to take suitable steps to keep a proper balance between the liquidity and profitability. An enterprise has to make sure the right inflow of cash into the business in due time by taking into account the outflow of cash. So, the financial managers of the enterprise must devise appropriate policies on working capital management so as to attain the most wanted objective of liquidity and profitability.

A number of methodological studied had find it that it is difficult for the PSEs to repay their borrowings and to offer sufficient return to their investors and hence in the verge of winding up. The studies further observed that a large number of PSEs has been incurring huge cash loss causing due pressure on the economy of the State. Even though, a number of studies have been conducted in the field of working capital management but, only very few studies have been carried out on public sector in general and company specific in particular. The study aims to study the working capital management of Kerala Minerals and Metals Ltd, to examine the liquidity position of Kerala Minerals and Metals Ltd. The study also aims in examining the relationship between the liquidity and profitability of the selected enterprise i.e., KMML. Thus, the present study is an effort to contribute to the existing literature.

2. LITERATURE REVIEW

The public sector enterprises have to imbibe professional management practices supported by sound management information system in PSUs in order to attain competitive advantage to tally its counterparts in the private sector. Misra and Sahu (2000) in their study concluded that financial leverage is a double-edged sword. Financial leverage is beneficial and helpful for maximising returns to the shareholders of the organisation only when there exist good economic factors. In unfavorable economic conditions, lesser financial leverage is preferable as it would lessen the chance of loss of wealth. These facts may present the logic and validate the preference for lower debt-equity levels by Indian corporates.

Mishra, R.K. (200l) in his study concluded that the public sector enterprises depended more on external source of finance, whereas the enterprises in the private sector depend more on internal resources. Moreover, the employment of short-term obligations as a source of finance is less in public enterprises as compared to their counterparts in the private sector. The cost of capital is at the center of every decision in the private sector, whereas in the public sector enterprises much importance is not given to the aspect of the cost of capital.

Biji James (2002) studied the profitability performance of companies from the viewpoint of gross profit. The study concluded that profitability performance from the point of view of gross profit is found to be satisfactory in all enterprises. But in the case of operating and net profit, performance of the state sector enterprises is not appraisable. The study also observed that modern management practices and techniques are not applied to these enterprises.

Mathuva (2010) examined the effect of working capital management on companys’ profitability and established that there is a highly negative relationship between the debtors’ velocity and profitability. The study concluded that the firms with shortest period of debtors’ velocity are more profitable.

Sharma and Kumar (2011) studied the effect of working capital on profitability of Indian firms. Data required for the study were collected from about 263 non-financial BSE 500 firms listed at the Bombay Stock (BSE) and analysed the same using OLS multiple regression. The result exhibited that there exists a positive correlation between working capital management and profitability in Indian companies.

Maradi, Salehi and Arianpoor (2012) made a comparative study of working capital management of two groups of listed companies in Tehran Stock Exchange (TSE), which consisted of chemical industry and medicine industry and analyzed the collected data using OLS multiple regression. The findings of the study showed that, the impact of debt ratio on reduction of net liquidity is more in medicine industry as compared to the enterprises in the chemical industry.

The government of Kerala (2016) in the economic review reported that erosion of working capital, limited product diversification, lack of up gradation of technology; increase in the cost of production, stiff competition, mounting financial obligations had resulted in the poor performance of the PSEs. The report suggested that it is extremely essential to focus more on the concentrated and timely action for bringing out good changes in the performance of the state level public sector enterprises.

Shivakumar, N Babitha Thimmaiah (2016) studied about working capital management and its influence on liquidity and profitability by taking a study of Coal India ltd. as a sample enterprise and concluded that the performance indicators such as current ratio, liquid ratio, working capital turnover ratio ROCE, stock turnover ratio have revealed a positive result except debtor’s turnover ratio and debtors velocity, where the trend is negative. The results also showed that there is a negative relationship between liquidity and profitability.

3. METHODOLOGY

The company selected as sample for the study is Kerala Minerals and Metals Ltd. which is one among the major public sector enterprises in Kerala. The study is primarily done on the basis of secondary data which is mainly collected from the annual reports and accounts of Kerala Minerals and Metals Ltd. The period of study is ten years, i.e. the data from 2009-10 to 2018-19 is being collected to understand the performance of the company. To study the working capital performance of the company, the performance drivers such as current ratio, quick ratio, inventory turnover ratio, working capital turnover ratio, ROCE, ROE, mean, standard deviation and variance were used. In order to assess the liquidity position of the company MOTAALS Comprehensive Test was used. Spearman’s rank correlation method and t test were used to study the relationship between the liquidity and profitability.

4. KERALA MINERALS AND METALS: BRIEF PROFILE

Kerala Minerals and Metals ltd. is one of the leading public sector companies in India. The company was started in the year 1932, with the name F. X. Perira and Sons (Travancore) Pvt. Ltd. In 1956, the Government of Kerala took over the enterprise and brought under the control of the industries department, government of Kerala. In the year 1972, the enterprise was converted into a limited company under the name ‘The Kerala Minerals and Metals Ltd.’ with the following broad objectives.

1) Optimal utilisation of mineral wealth found along the sea coast of Kollam-Alappuzha Districts.

2) Large scale generation of employment in the state in general.

3) Overall growth and development of the local area in particular and the state in general.

“A Brief History, KMML”.

The Titanium Dioxide Pigment plant

using chloride technology was commissioned in 1984 as the first and only

integrated Titanium Dioxide Plant in the world. Today, with over 2000 employees

and a range of products, KMML has become part and parcel of local and

international life. With the inauguration of

Titanium Sponge Plant, India became the 7th country in the world having the

technology for producing titanium sponge, which is the raw material for

titanium metal. On 6th September 2011, KMML TSP manufactured the 1st Batch of

Titanium sponge & now the production is in full swing. “A Brief History, KMML”.

KMML is now in the aerospace

industry & Defence applications with the

commissioning of the Titanium Sponge Plant. The TSP is a joint venture of KMML,

Vikram Sarabhai Space Centre (VSSC) and the Defence

Metallurgical Research Laboratory (DMRL). As a result

KMML has become a strategic Supplier of country’s present requirements of

Titanium for its prestigious space missions. Titanium sponge is known for its

high strength but low weight, making it an ideal material for aircraft

manufacture, including fighter aircraft. The material is also used in nuclear

plants, Engine parts, Ocean platforms, Reactors, Heat Exchangers and to make

dental implants and artificial bones. “A Brief

History, KMML”.

KMML touches our everyday life in numerous ways. The

products of KMML are everywhere, It is there in the dress we wear, the cosmetics we use,

the medicines we take, the paints we decorate our home with or the utility

plastic products,. Eco-friendly & socially committed, it is the only

integrated Titanium Dioxide facility having mining, mineral separation,

synthetic rutile and pigment-production plants. Apart from producing rutile

grade Titanium Dioxide pigment for various types of industries, it also

produces other products like Illmenite, Rutile,

Zircon, Sillimenite, Synthetic rutile etc. “A Brief History, KMML”.

5. RESULTS AND DISCUSSIONS

5.1. WORKING CAPITAL PERFORMANCE

The following ratios were used to study about the working capital performance of the enterprise.

Table 1: Performance drivers and measures used

|

Performance Drivers |

Measures Used |

|

Current Ratio |

Current Assets/Current

Liabilities |

|

Quick Ratio |

Quick Assets/Current

Liabilities |

|

Stock Turnover Ratio |

COGS/Average Inventory |

|

Stock Velocity (Days) |

365/Stock Turnover Ratio |

|

Working Capital Turnover

Ratio |

Sales/Working Capital |

|

Return on Capital Employed |

EBIT/ Capital Employed |

|

Return on Equity |

Net Profit/Net worth |

The working capital performance of the Kerala Minerals and Metals ltd are explained in table 2.

Table 2: Working capital performance

|

Year |

Current Ratio |

Quick Ratio |

Stock Turnover Ratio |

Stock Velocity (Days) |

Working Capital Turnover |

WCCA |

ROCE |

ROE |

EBIT |

Capital Employed |

|

2009-10 |

2.35 |

2.19 |

17.40 |

20.98 |

2.55 |

57.42 |

25.19 |

12.56 |

9264.62 |

36773.01 |

|

2010-11 |

1.45 |

1.38 |

23.82 |

15.32 |

4.38 |

31.13 |

18.37 |

5.71 |

6285.88 |

34210.42 |

|

2011-12 |

1.69 |

1.35 |

8.95 |

40.78 |

3.06 |

40.68 |

37.06 |

19.86 |

15450.52 |

41691.3 |

|

2012-13 |

2.87 |

2.00 |

4.32 |

84.44 |

1.76 |

65.17 |

14.16 |

5.90 |

7959.05 |

56215.99 |

|

2013-14 |

3.11 |

2.41 |

4.27 |

85.57 |

1.75 |

67.85 |

4.28 |

2.30 |

2682.86 |

62749.88 |

|

2014-15 |

3.22 |

2.25 |

4.08 |

89.50 |

1.57 |

68.91 |

-1.45 |

-4.22 |

-882.04 |

60677.91 |

|

2015-16 |

2.22 |

1.33 |

2.82 |

129.65 |

1.54 |

54.95 |

2.76 |

2.46 |

1556.57 |

56474.6 |

|

2016-17 |

2.36 |

1.83 |

2.90 |

125.66 |

2.07 |

57.68 |

10.87 |

2.00 |

6252.03 |

57527.21 |

|

2017-18 |

2.41 |

1.56 |

3.17 |

115.19 |

1.79 |

58.47 |

27.81 |

17.41 |

18525.66 |

66609.26 |

|

2018-19 |

2.57 |

2.05 |

3.41 |

107.00 |

1.78 |

61.03 |

23.62 |

13.54 |

17555.84 |

74333.24 |

|

CAGR |

0.89 |

-0.66 |

-15.03 |

17..69 |

-3.53 |

0.61 |

0.64 |

0.75 |

0.75 |

7.29 |

Source: Ten Years financial highlights, KMML.

The study shows that (table 2) the current ratio during the period of study gives a satisfactory performance in comparison with the usual standard of 2:1 except for the years 2010-11 and 2011-12 where the values are 1.45 and 1.69 respectively whereas the quick ratio is somewhat higher, but acceptable. The current ratios have increased from 2.35 in the year 2009-10 to 2.57 in the year 2018-19. In the case of quick ratio, it shows a decreasing trend from 2.19 in the year 2009-10 to 2.05 in the year 2018-19. The Compound Annual Growth Rate (CAGR) for current ratio is increasing at the rate of 0.89 while the CAGR for quick ratio is decreasing at the rate of 0.66.

The stock turnover ratio has decreased during the period of study from 17.40 to 3.41 from 2009-10 to 2018-19 which warrants for a proper and improved administration of inventory. The stock velocity during the period of study has increased from 20.98 days to 107 days also necessitates for a better inventory management system within the organisation. The Compound Annual Growth Rate (CAGR) for stock turnover ratio is decreasing at the rate of 15.03 while the CAGR for stock velocity in days is increasing at the rate of 17.69. The working capital ratio has shown a downward trend over the period which is not a good sign for the company. Therefore, it has to improve to a level where the company can manage working capital efficiently. The CAGR for working capital turnover ratio is decreasing at the rate of 3.53 while the CAGR for working capital for current assets is increasing at the rate of 0.61.

The profitability indicators such as return on capital employed (ROCE) and equity (ROE) have revealed a fluctuating trend over the past ten years. The figures for ROCE and ROE in the year 2009-10 and 2018-2019 respectively were 25.19 and 12.56 and it declined to a negative figure in the year 2014-15 and 2015-16 and after that it showed an increasing trend. The important pointer of profitability like EBIT has also improved which shows that the position of the firm is better. The CAGR for return on capital employed is increasing at the rate of 0.64 and also the CAGR for return on equity is increasing at the rate of 0.75. The capital employed by the company also showed an increasing trend during the period of study. It increased to Rs. 74333.24 in the year 2018-19 from Rs. 36773.01 lakhs in the year 2009-10. The CAGR for capital employed also shows an increasing trend at the rate of 7.29 during the period of study. (Table 2)

Table 3: Measures of working capital performance

|

Particulars |

Mean |

Standard Deviation |

Co-efficient of Variation |

|

Current Ratio |

2.42 |

0.41 |

23.25 |

|

Quick Ratio |

1.84 |

7.28 |

22.07 |

|

Stock Turnover Ratio |

7.51 |

41.95 |

96.92 |

|

Stock Velocity (Days) |

81.41 |

0.90 |

51.53 |

|

Working Capital Turnover |

2.23 |

0.41 |

40.24 |

The study revealed that (table 3) the average current and quick ratios are higher than the usual standard of 2:1 and 1:1 respectively which shows the firm has ability to pay its current liabilities as and when they arise. Also, the coefficient of variation is not too high (23.25, 22.07). It is to be noted that the average stock turnover ratio is not too high and also the period for the stock velocity is on higher side which warrants for more proficient management of inventory. Here, the Coefficient of variation for stock turnover ratio and stock velocity is on the higher side. It reflects the greater level of dispersion of mean. At the same time, it is important to note that the working capital ratio shows a good result indicating the efficient utlisation of the investments in working capital.

5.2. LIQUIDITY AND PROFITABILITY

The variables used for studying the correlation between liquidity and profitability are the Current Ratio and Return on Capital Employed. Spearman’s rank method and t test were used to measure the correlation between the two selected variables, Current Ratio and Return on Capital Employed.

Hypothesis:

Null Hypothesis: There

is a negative relationship between liquidity and profitability.

Table 4: Spearman’s

rank method

|

Year |

CR |

Rank |

ROCE |

Rank |

D (Rank Difference) |

D² |

|

2009-10 |

2.35 |

7 |

25.19 |

3 |

4 |

16 |

|

2010-11 |

1.45 |

10 |

18.37 |

5 |

5 |

25 |

|

2011-12 |

1.69 |

9 |

37.06 |

1 |

8 |

64 |

|

2012-13 |

2.87 |

3 |

14.16 |

6 |

3 |

9 |

|

2013-14 |

3.11 |

2 |

4.28 |

8 |

6 |

36 |

|

2014-15 |

3.22 |

1 |

-1.45 |

9 |

8 |

64 |

|

2015-16 |

2.22 |

8 |

-2.76 |

10 |

2 |

4 |

|

2016-17 |

2.36 |

6 |

10.87 |

7 |

1 |

1 |

|

2017-18 |

2.41 |

5 |

27.81 |

2 |

3 |

9 |

|

2018-19 |

2.57 |

4 |

23.62 |

4 |

0 |

0 |

|

Total |

228 |

|||||

![]()

𝑝=1−6⅀228/10(10²-1)

= 1 – 6*228/10*100-1

= 1 – 1368/10*99

= 1 – 1368/990

= 1 – 1.38

= -0.38

t- Test analysis:

𝒕=𝒓√𝒏−𝟐/√𝟏−𝒓²

= 0.38√10-2 / √1-0.38²

= 0.38√8 / √1−0.1444

= 0.38*2.828 / 0.9249

= 1.074 / 0.9249

= 1.1620

The table value of the t at 5% significance level of ((n-2)), (10-2) is 2.306 and the calculated value is 1.1620 which is smaller than the table value, therefore, the null hypothesis can be accepted. So, it can be concluded that there is a negative relationship between Profitability and liquidity.

Table 5: Correlation between working capital performance indicators

|

|

CR |

QR |

ITR |

WCT |

ROCE |

ROE |

|

CR |

1 |

|||||

|

QR |

0.82816 |

1 |

||||

|

ITR |

-1.2618 |

-0.21166 |

1 |

|||

|

WCT |

-1.62987 |

-0.4618 |

0.89523 |

1 |

||

|

ROCE |

-0.59494 |

-0.37916 |

0.32933 |

0.45138 |

1 |

|

|

ROE |

-0.49121 |

-0.36599 |

0.16171 |

0.26228 |

0.33106 |

1 |

The study also exhibits (table 5) the degree and amount of correlation between various working capital performance indicators. In the case of current ratio and ROCE, there is a highly negative correlation but in the case of quick ratio and current ratio, the correlation is a positive. There is a negative correlation between quick ratio and other ratios like inventory turnover ratio, working capital turnover ratio, ROCE and ROE. The study also shows a high positive correlation between working capital turnover ratio and both the return ratios.

5.3. MOTAALS COMPREHENSIVE TEST FOR ANALYZING LIQUIDITY POSITION

In order to analyse the liquidity

position, the variables such as Working Capital, Stock, and Liquid Assets are

used as a percentage of Current Assets. In

order to analyse the liquidity position of the Kerala

Minerals and Metals ltd., the Motaal’s test is

applied. (Table 6). On the basis of the Motaal’s test

ultimate ranking, it is clear that the liquidity position was best in the year

2014-15 followed by 2013.14 and 2012-13. In the year 2010-11and 2011-12 there

is a reason for anxiety regarding the liquidity position of the concern.

Overall, the test reveals that liquidity position of the company has improved

over the past years, i.e., during the period of the study.

Table 6: MOTAAL’S comprehensive test of liquidity

|

Year |

WC to CA |

Rank |

Stock to CA |

Rank |

LA to CA |

Rank |

Total Rank |

Ultimate Rank |

|

2009-10 |

57.42 |

7 |

6.65 |

9 |

93.35 |

2 |

18 |

7 |

|

2010-11 |

31.13 |

10 |

4.68 |

10 |

95.32 |

1 |

21 |

10 |

|

2011-12 |

40.68 |

9 |

19.72 |

8 |

80.28 |

3 |

20 |

9 |

|

2012-13 |

65.17 |

3 |

30.39 |

3 |

69.61 |

8 |

14 |

3 |

|

2013-14 |

67.85 |

2 |

22.40 |

5 |

77.60 |

6 |

13 |

2 |

|

2014-15 |

68.91 |

1 |

30.14 |

4 |

69.86 |

7 |

12 |

1 |

|

2015-16 |

54.95 |

8 |

40.25 |

1 |

59.75 |

10 |

19 |

8 |

|

2016-17 |

57.68 |

6 |

22.36 |

6 |

77.64 |

5 |

17 |

6 |

|

2017-18 |

58.47 |

5 |

35.38 |

2 |

64.62 |

9 |

16 |

5 |

|

2018-19 |

61.03 |

4 |

20.01 |

7 |

79.99 |

4 |

15 |

4 |

5.4. MANAGERIAL IMPLICATION

Liquidity and profitability are the two difficult terms for any organisation to deal with in the competitive business world. In order to survive and to be a leader in the modern competitive world, enterprises have to manage its funds effectively; particularly the short-term funds. This study pinpoints the facts that working capital management can be made effectively by keeping the stock velocity and debtor’s velocity within a reasonable level or equal to the standard level acceptable to the industry.

6. CONCLUSION

It is correct to say that working capital affects almost all the activities of the enterprises and it is difficult to highlight all the factors affecting working capital as these factors may vary from time to time and is industry dependent. The selected performance indicators in this study have shown an optimistic trend except for debtor’s turnover ratio and stock velocity. The liquidity ratios like current ratio and liquid ratios are higher than the benchmark indicating that the liquidity position of the firm was better. Working capital turnover ratios have shown a satisfactory performance. The test for correlation using the spearman’s rank method exhibited a negative relationship between liquidity and profitability which is significant at 5% (2-tailed) and revealed that the firm maintains excess liquidity over the period. The result derived from the correlation matrix revealed a negative relationship between current ratio and ROCE and also a positive relation between working capital ratio and return ratios. The result of the Motaal’s test for measuring liquidity indicates that the liquidity position of the company was superior in the year 2014-15and 2013-14 compared to other years. In total, it can be concluded that there is an improvement in the performance of the company in terms of profitability and liquidity. But, it is important to note that the firm has to improve its performance in relation to the ratios like debtors and stock velocity which will help the enterprise to enhance the liquidity and profitability position which will eventually help in the overall growth and development of the enterprise.

The results are generalizable with

the results replicated in other studies conducted under different

business environment settings. Shivakumar, and. N Babitha

Thimmaiah (2016) observed that there is a negative relationship between

liquidity and profitability and also a negative relationship between the

current ratio and the profitability ratios. Mathuva

(2010) studied the influence of working capital management on corporate

profitability and observed that there is a highly significant negative

relationship between the debtors’ velocity and profitability. The study

concluded that the firms with shortest period of debtors’ velocity are more

profitable.

SOURCES OF FUNDING

None.

CONFLICT OF INTEREST

None.

ACKNOWLEDGMENT

The authors would like to thank the officials and employees of the public sector enterprises in Kerala Minerals and Metals limited for providing the necessary data for establishing the objectives and for conducting the study. However, all the contents in this paper are of the authors’ responsibility.

REFERENCES

[1] “A Brief History, KMML”. http://kmml.com/php/showContent.php?linkid=10&partid=1

[2] Biji James (2002). A study on financial strength, profitability and productivity of public sector chemical enterprises in Kerala, Ph. D Thesis, Thiruvananthapuram: University of Kerala.

[3] Maradi, Salehi and Arianpoor (2012). A comparative study of working capital management of two groups of listed companies in Tehran Stock Exchange. International Journal of Advanced Research in Management and Social Sciences ISSN: 2278-6236 Vol. 1, No. 3, September 2012, www.garph.co.uk IJARMSS.

[4] Government of Kerala (2016). Economic Review. Kerala, State Planning Board, Thiruvananthapuram.

[5] Mishra R.K. (2001). Financial Management in Public Enterprises; Present Scenario and Challenges to Transition. Finance India, Vol. XV, No.2, pp. 546-547.

[6] Misra, R.N, & Chinmay, Sahu (2000). A study on the preferred debt equity mix among Indian industries. Management Accountant, January 2000, pp. 48- 50.

[7] Pandey, S. (2008). Impact of Working Capital Management in the Profitability of Hindrance Industries Limited, the ICFAI University Journal of Financial Economics, Vol. 36.

[8] Shivakumar, and. N Babitha Thimmaiah. (2016). “working capital management - it’s impact on liquidity and profitability - a study of Coal India ltd.” International Journal of Research - Granthaalayah, 4(12), 178-187. https://doi.org/10.5281/zenodo.223836.

[9] Singh, P. (2008). Inventory and Working Capital Management: An Empirical Analysis, The Icfai University Journal of Accounting Research, Vol. 35. Singh, J.P.

[10] Sur, D. (2006). Efficiency of Working Capital Management in Indian Public Enterprises during the Post-liberalization Era: A Case Study of NTPC, The ICFAI Journal of Management Research, Vol. 34.

[11] Kerala Minerals and Metals Limited. (2020). Ten-year financial highlights. Retrieved from Kerala Minerals and Metals Limited. website: http://kmml.com/php/showContent.php?linkid=66&partid=1.

|

|

This work is licensed under a: Creative Commons Attribution 4.0 International License

This work is licensed under a: Creative Commons Attribution 4.0 International License

© Granthaalayah 2014-2020. All Rights Reserved.