Original Article

Financial Literacy in the Digital era: The role of Technology and Innovation in Transforming Investment Decisions

|

Dr. Renati Jayaprakash Reddy 1*, Pushpa M 2 1 Professor, Acharya

Institute of Management and Sciences, Bangalore, India 2 AIMS Centre for Advanced Research Centre,

University of Mysore, India |

|

|

|

ABSTRACT |

||

|

This study examines the significance of technology and innovation in enhancing financial literacy (FL) in the digital era and transforming investment decisions (ID) among Private Higher Educational teachers in Bengaluru Urban. Primary data was collected through self- administered questionnaire from 128 respondents and tested using SPSS Version 26. The reliability of the data was measured using “Cronbach’s alpha”, descriptive statistics to estimate mean and SD for the demographic data and Regression Analysis to validate the association among variables. The study’s finding reveals the significant role of Technology and Innovation in improving FL, thereby exerting a direct effect on individual's ID. The study highlights the need for educational institutions to conduct practical- oriented sessions for teachers on the integration of technology and innovation in the area of FL. The adoption of financial tools and applications is essential as teacher serves as a learner and also a facilitator in enhancing the next generation to be more rational and sustainable in their financial choices. The government should initiate subsidized access to e-learning platforms, digital tools and financial planning software for teachers to support continuous learning. Keywords: Financial Literacy, Technology and

Innovation, Investment Decisions. |

||

INTRODUCTION

The financial

sector has transformed significantly due to the new paradigm of Industry 4.0,

which is based on emerging technologies such as Artificial Intelligence (AI),

cyber-physical systems, and Internet of Things (IoT). Gunasekaran

et al. (2024), Bai et al. (2022) and subsequently has created the phenomenon

of financial technologies (FinTech), which provide new tools and innovations to

enable individuals in managing their personal finances and facilitate

investment decisions Islam

and Khan (2024). Robo-advisors and digital wallets are

lowering the cost and complexity of financial services as these technologies

enable people to manage their investments. However, the eventual success of

those services will depend mainly on the users’ FL and the education that

surrounds digital financial competences Ariwangsa et

al. (2024). Additionally, Lal et al. (2025) identifies three drivers of DFL being

economic resources, educational background, and digital involvement, and also

argues that inequality in access to digital resources may magnify distinctions

in levels of financial decision-making. These findings support the need to

investigate FL not as discrete and isolated rather as a function of digital

competencies that influence the investment behavior

in the digital age.

The rapid growth

in digital technology is changing the financial landscape and allowing

individuals to access information and financial services Darwish

et al. (2025). Hassan

et al. (2024) demonstrate that Fintech self-efficacy

moderates the FL investment behavior, implying that

literacy and digital confidence together shape the technology

based investment choices. Bai et al. (2023) reveals that FL contributes to investment

decision making and thus enhances wellbeing, while Luo et al. (2023) draw on micro-level evidence from China to

show that the FL of households increases the likelihood of profit in equity

investments. Mishra

et al. (2024) demonstrate that women who possess a high

level of DFL will be more likely to adopt Fintech services and make better

investment decisions, illustrating how DFL can lessen gender disparities in

financial inclusion.

Xie and Chen (2024) also indicated, households with a high level

of DFL are more likely to be entrepreneurs and investors, underscoring the

larger societal economic impacts of being digitally competent. Similarly, Olajide

et al. (2024) examined multiple generational differences

on usage of social media for investment advice, and

found that younger generations are more influenced by digital content for

investment decisions, which impacts their financial satisfaction. These studies

demonstrate the influence of both formal and informal digital networks in

shaping investment choices. Along with these transformations, individuals must

learn to comprehend and effectively manage financial products and platforms.

Although technology is widely available, an inadequate FL and behavioral biases can still lead to adverse financial

outcomes Aftab et

al. (2025). Therefore, FL is needed to minimize risks

associated with digital tools, leading to more prudent financial decisions.

Individuals who possess greater FK are better able to analyze

risks, diversification opportunities, and evade fraudulent schemes.

The study is

focused on examining the impact of technology and innovation in enhancing FL in

the digital era and transforming investment decisions among private higher

educational teachers in Bengaluru urban. As the academic space continues to

change, the role of the teacher is not just delivering static knowledge, rather

developing the digital and financial skills to navigate complex information

system. Therefore, studying their perception becomes essential.

Review of Literature

Technology and Innovation in Enhancing FL

Technology and

innovation have emerged as fundamental drivers to enhance FL in this digital

era. For example, Digital Financial Literacy (DFL), extends existing knowledge

and skills of FL to locate and tailor digital financial services, and is

increasingly referred to as a necessity for effective financial decision-making

Khatri

et al. (2025). In addition, an empirical study supported

the mediating effects of DFL on financial decision making. Kumar et

al. (2022), describes DFL as a component of individual

financial wellness, and suggests that collaborative educational and policy

responses are necessary. Technological advances, such as fintech, have been

demonstrated to improve accessibility to budgeting tools, expense tracking, and

savings habits Cahyono

and Susbiyani (2025). The following discussions indicate the

effects of fintech and digital tools on personal finance management behavior. Waliszewski

and Warchlewska (2020) concluded that social-economic

characteristics were significantly impacted the satisfaction level in AI-based

financial planning, while Gautam

et al. (2022) reported the fintech adoption through credit

card schemes that were positively

correlated to digital literacy, especially in contexts with unskilled

populations. In accordance with this, Zhang

and Fan (2024) reported that mobile FinTech usage can

enhance financial well-being when paired with adequate literacy levels.

Researchers have also shown that simulation-based learning methods sustain

student interaction and retention of the information around financial concepts

more effectively than traditional instruction Belgacem

et al. (2024). Using the Technology Acceptance Model

(TAM), Jariyapan et

al. (2022) found that perceived usefulness is the most

significant predictor of behavioral intention to

adopt crypto currencies, with FL and perceived risk being significant

explanatory factors. Despite the growing body of literature, there is still

inadequate study on the combined effects of technology and innovations on FL

within the digital age, particularly in the context of private higher education

teachers in Bengaluru City. To address this gap, the hypothesis considered in

this study is:

H1: Technology and

innovation is positively associated in enhancing FL in

the digital era.

Impact of FL on Investment decisions

The advancements

of digital technologies, along with behavioral

finance, have created decision-making determinants beyond the FL components,

such as attitudes, risk tolerance, and technology-based platforms. Seraj, Alzain, and Alshebami (2022)

found that FL significantly improved investor decisions, particularly when

moderated by overconfidence of investors. Andersson

et al. (2023) revealed that FK, when mediated by behavioral finance variables, helps capital market

investors make informed decisions. Rahmiyati and Somodiharjo (2025) expanded on this study and confirmed

evidence of a relationship between FL, behavioral

biases, and individual investment performance in Indonesia. Innovative methods

were also used to further support the relationship. Jariyapan et

al. (2022) emphasized the need of FL in the high-risk,

technology-driven investment space. Kumar et

al. (2023) explored the behavioral,

psychological, and demographic-based factors of household investment decisions,

offering evidence that digital financial literacy (DFL) serves as a partial

moderator between financial capability and decision-making and included

psychological and behavioral aspects of investment

decisions for a sustained financial future. Likewise, Aisa (2021) also investigated FL and the use of technology-based investment

platforms on students’ intention to invest in the capital market. Both FL and

the usage of the investment platform were determined to have a significant

relation to investment intentions, and it was concluded that early use of

financial investment tools would prompt students to actively engage with

financial decision-making. Likewise, Zaimovic et al.

(2023) systematically reviewed the relationship between FL and FB by

highlighting DFL as a growing determinant of improved decision-making.

Stressing these digital investment preparedness gaps, Yeo et al. (2023) extended the literature by introducing behavioral finance concepts to the Theory of Financial

Planning Behavior (TFPB) within a descriptive

contextual model that provides a more accurate account of investment

decision-making across diverse contexts. The existing work has explored the

impact of FL on investment decisions; limited studies have investigated this

relationship in the context of technology and innovation-driven improvements in

FL. There is a need to examine how technology-enabled advancements in FL lead

to informed investment decisions. Thus, the study postulates the following

hypothesis:

H2: FL

significantly influences investment decisions.

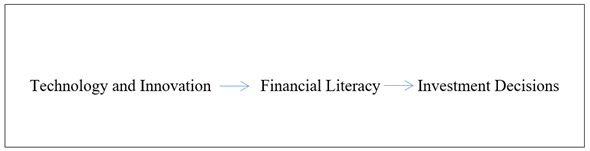

Conceptual

Framework

Research Methodology

The present study

adopts the framework of descriptive and explanatory research design. The

descriptive design was employed to analyze the

demographic characteristics and the explanatory design was used to examine the

effect of Technology and Innovation on FL and its impact on ID. The population of the study comprised

teachers working in private higher educational institutions in Bangalore Urban.

Using non- probability convenience sampling, a total of 128 respondents were

selected to represent the study sample. Data was collected with a structured

questionnaire that included three items measuring Technology and Innovation,

Financial Literacy, and Investment Decisions. Data was analyzed

using SPSS Version 26: The reliability of the questionnaire was measured using

“Cronbach’s alpha”, descriptive statistics to estimate mean and variability for

the demographic data and Regression Analysis to validate the association among

variables.

Results

Reliability Results

|

Table 1 |

|

Table 1 Reliability Statistics for the Overall measure |

|

|

Reliability Statistics |

|

|

Cronbach's Alpha |

N |

|

0.93 |

29 |

|

Source: SPSS 26 |

|

Table 1 presents the internal reliability of the

scale. The overall reliability of the 29 items indicates Cronbach’s Alpha of

.930, validating strong internal consistency. In general, Cronbach’s Alpha

above .70 demonstrates the stated variables are good to use. Nunnally

(1975)

|

Table 2 |

|

Table 2 Reliability Statistics for Individual

Constructs |

||

|

Constructs |

Reliability Statistics |

|

|

|

Cronbach's Alpha |

N |

|

Financial Literacy |

.826 |

5 |

|

Technology and

Innovation |

.914 |

10 |

|

Investment Decisions |

.893 |

14 |

|

Source: SPSS 26 |

||

Table 2 outlines the reliability scale per

construct. The Cronbach’s Alpha for Financial Literacy (5 items) = .826;

Technology and Innovation (10 items) = .914; and Investment Decisions (14

items) = .893 results show the items in each construct are highly consistent

and reliable.

|

Table 3 |

|

Table 3 Demographic Profile |

|||

|

Demographic Profile |

Frequency |

Percent |

|

|

< 30 years |

22 |

17.2 |

|

|

31-40 years |

64 |

50 |

|

|

41-50 years |

30 |

23.4 |

|

|

Age |

> 50 years |

12 |

9.4 |

|

Male |

44 |

34.4 |

|

|

Gender |

Female |

84 |

65.6 |

|

Post Graduate |

96 |

75 |

|

|

Educational

Qualification |

Doctorate |

30 |

23.4 |

|

Post-Doctoral |

2 |

1.6 |

|

|

Years of Work

Experience |

< 5 years |

14 |

10.9 |

|

6-10 years |

44 |

34.4 |

|

|

11-15 years |

32 |

25 |

|

|

16-20 years |

20 |

15.6 |

|

|

>20 years |

18 |

14.1 |

|

|

Unmarried |

22 |

17.2 |

|

|

Marital Status |

Married |

102 |

79.7 |

|

Divorced |

4 |

3.1 |

|

|

Nuclear |

72 |

56.3 |

|

|

Type of family |

Joint |

46 |

35.9 |

|

Single Parent |

10 |

7.8 |

|

|

< 5lakh |

42 |

32.8 |

|

|

Annual income |

5 to 10 lakh |

64 |

50 |

|

10 Lakh to 15 lakh |

12 |

9.4 |

|

|

>15 lakh |

10 |

7.8 |

|

|

Note: N = 128 |

|||

Table 3 summarizes the demographic profile of the

respondents.

A total of 128

respondents represented demographic characteristics. The sample shows that the

majority (50%) was aged 31-40 years, 23.4% were 41-50 and 9.4% are above 50

years. The gender distribution includes 65.6% female and 34.4% male. Regarding

education, 75% hold post graduate, 23.4% are with Doctorate and 1.6%

post-doctoral. In terms of work experience, 34.4% have 6-10 years, 25% with

11-15 years and 10.9 less than 5 years. 79.7% of the respondents are married,

and 56.3% were in a Nuclear Family. Income level indicates 50% of them earn

between 5 to 10 lakhs, 32.8% below 5 lakhs, and 7.8% above 15 lakhs.

|

Table 4 |

|

Table 4 Descriptive Statistics |

|||

|

Constructs |

Descriptive Statistics |

||

|

No of items |

Mean |

Std. Deviation |

|

|

Statistic |

Statistic |

||

|

Financial Literacy |

5 |

3.625 |

.81289 |

|

Technology and

Innovation |

10 |

3.1578 |

.83446 |

|

Investment Decisions |

14 |

3.7857 |

.61908 |

|

Output:

SPSS 26, Note* N=128 |

|||

The descriptive

statistics of the constructs are presented in Table 4 FL, measured with the scale of 5 items, shows a mean of 3.63 (SD =

0.81), suggesting moderate financial knowledge among the respondents.

Technology and Innovation, based on the set of 10 constructs has a mean of 3.16

(SD = 0.83), indicating moderate average with more spread in responses compared

to Financial Literacy. Investment Decisions measured with the set of 14 items,

had the highest mean of (M = 3.79, SD = 0.62) with lower variability.

Regression Analysis

|

Table 5 |

|

Table 5 Technology and Innovation in Enhancing FL in the Digital Era |

||||||

|

Coefficientsa |

||||||

|

Model |

Unstandardized

Coefficients |

Standardized

Coefficients |

t |

Sig. |

||

|

B |

Std. Error |

Beta |

||||

|

1 |

(Constant) |

2.049 |

0.243 |

8.419 |

0 |

|

|

Technology and

Innovation |

0.499 |

0.075 |

0.512 |

6.696 |

0 |

|

|

Dependent Variable:

Financial literacy |

||||||

Table 5 demonstrates the regression results. The

regression analysis studied the effect of Technology and Innovation on

Financial Literacy. In which financial literacy is taken as the dependent

variable, technology and innovation as the independent variable. The results

reveals that Technology and innovation is significantly associated with

Financial Literacy (B = 0.499, t = 6.696, p < .001.The standardized

coefficient (β = .512) indicates the increase in Technology and Innovation

will likely improve Financial Literacy levels.

|

Table 6 |

|

Table 6 Impact of FL on Individuals ID |

||||||

|

Coefficientsa |

||||||

|

Model |

Unstandardized Coefficients |

Standardized Coefficients |

t |

Sig. |

||

|

B |

Std. Error |

Beta |

||||

|

1 |

(Constant) |

2.253 |

0.21 |

10.749 |

0 |

|

|

Financial Literacy |

0.423 |

0.056 |

0.555 |

7.494 |

0 |

|

|

Dependent Variable: Investment Decisions |

||||||

The model shows

Investment decision as a dependent variable and financial literacy as a

predictor. The results from regression analysis indicates a strong positive

influence of FL on Investments decisions (B = .423, t = 7.494, p < .001).

The standardized coefficient (β = .555) reveals that respondents with

higher level of financial literacy leads to a sound investment decisions.

Overall, the

regression results provide evidence for the proposed hypotheses, showing the

important role of Technology and Innovation on improving Financial Literacy,

thereby exerting a direct effect on an individual's investment decision.

|

Table 7 |

|

Table 7 Hypotheses Testing

Results |

|||||

|

Hypotheses |

Relationship Tested |

Standardized Beta

(β) |

t-value |

Sig. (p-value) |

Conclusion |

|

H1 |

Technology and Innovation ➝ Financial Literacy |

0.512 |

6.696 |

0 |

Accepted |

|

H2 |

Financial Literacy ➝ Investment Decisions |

0.555 |

7.494 |

0 |

Accepted |

|

Source: Authors Computation |

|||||

The hypotheses

results are presented in Table 7 Technology and Innovation have a significant impact in increasing

financial literacy in the digital age (β: .512, t-value: 6.696, p-value:

.000). Hence H1 is supported. Similarly Financial Literacy significantly

influences Investment decisions (β: .555, t-value: 7.794, p-value: .000)

supporting H2.

Discussion

The study examined

financial literacy in the digital era and investigated the role of technology

and innovation in shaping investment decisions among private higher educational

institutions teachers in Bengaluru urban. The findings obtained from a regression

analysis indicates the significance of Technology and Innovation in enhancing

FL, suggesting that digital tools

support individuals in comprehending and managing financial ideas. This aligns

with the work of Ferilli et al.

(2024) where DFL is claimed to be a key factor in

enhancing financial well-being and promoting effective decision making.

Moreover, Furinto et al.

(2023) states that the development of FL was

successful and the fintech aspects were a major element in contributing to the

improvements. Moreover, the results suggest that Technology and innovation is

significantly related to FL, and these findings are consistent with recent

works, namely, Ariwangsa et

al. (2024) found FL as a main influencer of investment

decisions made by small and medium businesses, with technology representing a

moderating aspect to strengthen the relationship between FL and ID making. Futhermore, Raut and Kumar (2023) explains that an individuals

who has a high FL, can be characterized as a rational investor, as they evaluates risk and return before making any investment

decision. Overall, the discussion emphasizes that increasing financial

knowledge using technology can support better financial conduct and sustainable

investments.

Conclusion

In the present

study, the emphasis was made on three important variables- Technology and

Innovation, FL and ID. The evidence suggests that teachers in private higher

educational institutions with increased access to digital equipment and

technological advances can enhance their financial literacy and make better

informed investment decisions. The adoption of financial tools and applications

is essential as teacher serves as a learner and also a facilitator in enhancing

the next generation to be more rational and sustainable in their financial

choices. The study highlights the need

for educational institutions to conduct practical- oriented sessions for

teachers on the integration of technology and innovation in the area of

financial literacy. The government should initiate subsidized access to digital

tools, e-learning platforms, and financial planning software for teachers to

support continuous learning.

The study is

limited to the teachers of private higher educational institutions in Bengaluru

urban. The relationship between the study’s variables was tested using

regression analysis. Future studies can explore the mediating role of FL

between technology and ID across different regions. This can provide a better

understanding of the relationship between digital innovations and financial

knowledge in affecting investment behavior.

ACKNOWLEDGMENTS

None.

REFERENCES

Aftab, R., Fazal, A., and Andleeb, R. (2025). Behavioral Biases and Fintech Adoption: Investigating the Role of Financial Literacy. Acta Psychologica, 257, 105065. https://doi.org/10.1016/j.actpsy.2025.105065

Aisa, N. N. (2021). Do Financial Literacy and Technology Affect Intention to Invest in the Capital Market in the Early Pandemic Period? Journal of Accounting and Investment, 23(1), 49–65. https://doi.org/10.18196/jai.v23i1.12517

Andersson, H. (2023). The Influence of Demographic Factors and Financial Literacy on Investment Decisions Mediated by Behavioral Finance (Empirical study: On Capital Market Investors in DKI Jakarta). Journal Research of Social Science Economics and Management, 3(04). https://doi.org/10.59141/jrssem.v3i04.588

Ariwangsa, N. I. O., P, N. K. W. S. P., and P, N. K. W. L. (2024). The Impact of Financial Literacy on Investment Decisions: The Moderating Role of Financial Technology. UPI YPTK Journal of Business and Economics, 9(3), 16–22. https://doi.org/10.35134/jbe.v9i3.274

Bai, C., Li, H. A., and Xiao, Y. (2022). Industry 4.0 Technologies: Empirical Impacts and Decision Framework. Production and Operations Management. https://doi.org/10.1111/poms.13813

Bai, R. (2023). Impact of Financial Literacy, Mental Budgeting and Self-Control on Financial Wellbeing: Mediating Impact of Investment Decision Making. PLOS ONE, 18(11), e0294466. https://doi.org/10.1371/journal.pone.0294466

Belgacem, S. B., Khatoon, G., Bala, H., and Alzuman, A. (2024). The Role of Financial Technology on the Nexus Between Demographic, Socio-Economic, and Psychological Factors, and the Financial Literacy gap. SAGE Open, 14(2). https://doi.org/10.1177/21582440241255678

Cahyono, D., Susbiyani, A., Lestari, E., Fauziyah, F., Qomariah, N., and Guntu, Y.S. (2025). Role of Personal Savings in Financial Tech Impact on Family Planning in Indonesia. 7(1). https://doi.org/10.34306/att.v7i1.494

Darwish, F. S. M. (2025). Financial Literacy and Investment Decision: An Empirical Study from the Palestine Stock Exchange. Frontiers in Behavioral Economics, 4. https://doi.org/10.3389/frbhe.2025.1444022

Ferilli, G. B., Palmieri, E., Miani, S., and Stefanelli, V. (2024). The Impact of Fintech Innovation on Digital Financial Literacy in Europe: Insights from the Banking Industry. Research in International Business and Finance, 69, 102218. https://doi.org/10.1016/j.ribaf.2024.102218

Furinto, A., Tamara, D., Yenni, N., and Rahman, N. J. (2023). Financial and Digital Literacy Effects on Digital Investment Decision Mediated by Perceived Socio-Economic Status. E3S Web of Conferences, 426, 02076. https://doi.org/10.1051/e3sconf/202342602076

Gautam, R. S., Rastogi, S., Rawal, A., Bhimavarapu, V. M., Kanoujiya, J., and Rastogi, S. (2022). Financial Technology and its Impact on Digital Literacy in India: Using Poverty as a Moderating Variable. Journal of Risk and Financial Management, 15(7), 311. https://doi.org/10.3390/jrfm15070311

Gunasekaran, A., Kamble, S., Ghadge, A., and Kumar, V. (2024). Investments in Industry 4.0 technologies and Supply Chain Finance: Approaches, Framework and Strategies. International Journal of Production Research, 62(22), 8049–8055. https://doi.org/10.1080/00207543.2024.2405322

Hassan, N. C., Abdul-Rahman, A., Hamid, S. N. A., and Amin, S. I. M. (2024). What Factors Affecting Investment Decision? The Moderating Role of Fintech Self-Efficacy. PLOS ONE, 19(4), e0299004. https://doi.org/10.1371/journal.pone.0299004

Islam, K. M. A., and Khan, M. S. (2024). The Role of Financial Literacy, Digital Literacy, and Financial Self-Efficacy in Fintech Adoption. Investment Management and Financial Innovations, 21(2), 370–380. https://doi.org/10.21511/imfi.21(2).2024.30

Jariyapan, P., Mattayaphutron, S., Gillani, S. N., and Shafique, O. (2022). Factors Influencing the Behavioural Intention to use Cryptocurrency in Emerging Economies During the COVID-19 Pandemic: Based on Technology Acceptance Model 3, Perceived Risk, and Financial Literacy. Frontiers in Psychology, 12. https://doi.org/10.3389/fpsyg.2021.814087

Khatri, H., Idrees, M. A., and Sultan, F. (2025). Impact of Fintech on Financial Inclusion: The Mediating Role of Digital Financial Literacy. 4(01), 1024–1043. https://doi.org/10.55966/assaj.2025.4.1.068

Kumar, P., Islam, M. A., Pillai, R., and Sharif, T. (2023). Analysing the Behavioural, Psychological, and Demographic Determinants of Financial Decision Making of Household Investors. Heliyon, 9(2), e13085. https://doi.org/10.1016/j.heliyon.2023.e13085

Kumar, P., Pillai, R., Kumar, N., and Tabash, M. I. (2022). The Interplay of Skills, Digital Financial Literacy, Capability, and Autonomy in Financial Decision Making and Well-Being. Borsa Istanbul Review, 23(1), 169–183. https://doi.org/10.1016/j.bir.2022.09.012

Lal, S., Bawalle, A. A., Khan, M. S. R., and Kadoya, Y. (2025). What Determines Digital Financial Literacy? Evidence from a Large-Scale Investor Study in Japan. Risks, 13(8), 149. https://doi.org/10.3390/risks13080149

Luo, Z., Azam, S. M. F., and Wang, L. (2023). Impact of Financial Literacy on Household Stock Profit Level in China. PLOS ONE, 18(12), e0296100. https://doi.org/10.1371/journal.pone.0296100

Mishra, D., Agarwal, N., Sharahiley, S., and Kandpal, V. (2024). Digital Financial Literacy and its Impact on Financial Decision-Making of Women: Evidence from India. Journal of Risk and Financial Management, 17(10), 468. https://doi.org/10.3390/jrfm17100468

Nunnally, J. C. (1975). Psychometric Theory—25 Years Ago and now. Educational Researcher, 4(10), 7–21. https://doi.org/10.3102/0013189X004010007

Olajide, O., Pandey, S., and Pandey, I. (2024). Social Media for Investment Advice and Financial Satisfaction: Does Generation Matter? Journal of Risk and Financial Management, 17(9), 410. https://doi.org/10.3390/jrfm17090410

Rahmiyati, N., and Somodiharjo, K. (2025). The Impact of Financial Literacy, Investment Decision-Making, Risk Tolerance, and Behavioral Biases on Individual Investment Performance. The Es Accounting and Finance, 3(03), 223–237.

Raut, R. K., and Kumar, S. (2023). An Integrated Approach of TAM and TPB with Financial Literacy and Perceived Risk for Influence on Online Trading Intention. Digital Policy, Regulation and Governance, 26(2), 135–152. https://doi.org/10.1108/DPRG- 07-2023-0101

Cahyono, D.C., and Susbiyani, A. (2025). Role of Personal Savings in Financial Tech Impact on Family Planning in Indonesia. (n.d.). Aptisi.

Seraj,

A. H. A., Alzain, E., and Alshebami, A. S. (2022). The Roles

of Financial Literacy and Overconfidence

in Investment Decisions in Saudi Arabia. Frontiers in Psychology, 13, 1005075.

Waliszewski, K., and Warchlewska, A. (2020). Attitudes Towards Artificial Intelligence in the Area of Personal Financial Planning: A Case Study of Selected Countries. Entrepreneurship and Sustainability Issues, 8(2), 399–420.

Xie, Y., and Chen, T. (2024). A Study on the Impact of Digital Financial Literacy on Household Entrepreneurship—Evidence from China. Sustainability, 17(1), 117. https://doi.org/10.3390/su17010117

Yeo, K. H. K., Lim, W. M., and Yii, K. (2023). Financial Planning Behaviour: A Systematic Literature Review and New Theory Development. Journal of Financial Services Marketing. https://doi.org/10.1057/s41264-023-00249-1

Zaimovic, A., Torlakovic, A., Arnaut-Berilo, A., Zaimovic, T., Dedovic, L., and Meskovic, M. N. (2023). Mapping Financial Literacy: A Systematic Literature Review of Determinants and Recent Trends. Sustainability, 15(12), 9358. https://doi.org/10.3390/su15129358

Zhang, Y., and Fan, L. (2024). The Nexus of Financial Education, Literacy and Mobile Fintech: Unraveling Pathways to Financial Well-Being. International Journal of Bank Marketing, 42(7), 1789–1812. https://doi.org/10.1108/IJBM-09-2023-0531

This work is licensed under a: Creative Commons Attribution 4.0 International License

This work is licensed under a: Creative Commons Attribution 4.0 International License

© Granthaalayah 2014-2025. All Rights Reserved.