CSR practices: an analysis of the impact of societal and environmental commitment on the performance of SMEs in the Cameroonian context

Yves Mballa Atangana 1![]() , Yayé Barouwa 2

, Yayé Barouwa 2![]() , Armel Lewe

Nguepnang 3

, Armel Lewe

Nguepnang 3![]()

1 CAMES

Assistant Professor, Management Sciences, University of Yaoundé 2, Soa, Cameroon

2 Doctor,

Management Sciences, University of Yaoundé 2, Soa, Cameroon

3 Doctoral

Student, Management Sciences, University of Yaoundé 2, Soa, Cameroon

|

|

|

ABSTRACT |

|

|

This article explores the deliberate and/or imposed incorporation of CSR practices by SMEs in the African context, focusing on the influence of these practices on the quest for performance by Cameroonian SMEs. The deployment of CSR practices is part of the utilitarian "social issue management" trend in an approach based on societal and environmental analysis. Based on the specificity of the African environment and on the theoretical division, the coexistence of the formal and informal sector with the predominance of the informal over the formal, our results reveal in priority a societal and environmental commitment in CSR practices, a guarantee of performance in terms of environmental protection, endowment of a social charter and increase of new market shares. The reputation of the SME is reinforced in its ecosystem, allowing it to transform itself and legitimise itself with the various stakeholders. |

|||

|

Received 22 December 2022 Accepted 24 January 2023 Published 07 February 2023 Corresponding Author Yayé Barouwa, yayebarouwa@yahoo.fr

DOI 10.29121/granthaalayah.v11.i1.2023.4985 Funding: This research

received no specific grant from any funding agency in the public, commercial,

or not-for-profit sectors. Copyright: © 2023 The

Author(s). This work is licensed under a Creative Commons

Attribution 4.0 International License. With the

license CC-BY, authors retain the copyright, allowing anyone to download,

reuse, re-print, modify, distribute, and/or copy their contribution. The work

must be properly attributed to its author.

|

|||

|

Keywords: CSR, Environmental Commitment, Societal

Commitment, Performance |

|||

1. INTRODUCTION

In recent

years, corporate social responsibility (CSR) has become a societal debate and a

research topic that has attracted the attention of researchers in economics and

management. Long reserved for large companies, CSR is now a strategic issue for

smaller organisations, especially SMEs Boubakary and Moskolaï

(2017). In this perspective, and in view

of the declining involvement of the state in its economic and social missions,

CSR is far from being considered today as a strategic variable in the

governance of small and medium-sized enterprises (SMEs) but as a reality that

applies to any type of entity Sangue Fotso

(2018). As a result, CSR should not be

considered as a label for this category of companies, as it is about

reconciling the different economic and financial, environmental, and social

issues Companies then hope to benefit from these actions in terms of image and

reputation and especially in terms of performance. For CSR has not come to

change the nature of the capitalist company in order to

make profits, but to help it change its practices, to make them evolve in order

to achieve its objective in the most responsible way possible Jihad and Yaagoubi (2019).

CSR is

seen as an opportunity for each company to improve its governance, strengthen

its societal commitment and limit its environmental impact Manssori and El Hamri

(2022). Faced with this competitive rivalry,

SMEs, in order to remain competitive, must more than

ever integrate the CSR component into their strategic policy in order to meet

the requirements of their partners, as its implementation requires significant

material and immaterial investments Abbassi and Saidi

(2019). Thus, according to Abord and Bachelard (2006), the aim of CSR is not

limited to the economic and financial aspect, but also engages a renewal of the

reflection on the objectives and functioning of the company. In this

perspective, Boubakary and Moskolaï

(2017) refer to the lack of consensus on

the perception of taking CSR practices into account within the SME, which gives

rise to numerous debates in the scientific and business world. Many SMEs, in order

to contribute to socio-environmental progress Agbovoedo et al. (2022), include social objectives to their

profitability objectives and respect the principles and values in their

management mode and that the financial performance of these companies finds its

relevance mainly in the constraining reality of business Abid (2020). However, Cameroon is not on the

fringe of this reality in the African or even global context, since SMEs

represent 90 to 95% of the population of Cameroonian enterprises and employ

49.7% of the active population Feudjo (2006). It should be noted that the development

of concerns related to social responsibility in companies remains marginal.

Thus, Wong and Yameogo

(2011) believe that Africa reflects

realities that escape the traditional focus of Western approaches to social

responsibility and are not the product of the same cultural history.

The

economic fabric of Cameroon presents nearly 80% of small entities with a family

connotation where the role of the manager is intertwined with that of the

company Sangué Fotso

(2011). As a result, the values of the

manager are at the heart of the managerial philosophy promoted within the

company. These entities evolve in a restrictive environment where their source

of financing remains tontine and self-financing, which are also insufficient. In order to maintain their position in their highly

competitive market, these entities operate in defiance of all ethical and

social codes. In this perspective, the strong mobilisation of certain

international organisations on the issue of ethics and respect for the

environment reflects the urgent need for reflection. The popularisation of the "social responsibility"

function is still lagging behind in African SMEs,

particularly in Cameroon. Perhaps they do not measure the stakes or the

inherent gains Djoutsa Wamba and Hikkerova

(2014). Research has focused on

characterising the company's ability to control its social commitment and

achieve satisfactory results. However, the notion of performance inherent in

socially responsible enterprise remains at the heart of the concerns of

researchers in Cameroon.

Indeed, much

research have been carried out to verify the influence of CSR on performance,

but most of them do not address the societal and environmental dimension.

Indeed, research by Ondoua Biwolé

(2012) shows that empirical results in the

field of CSR are inconclusive and highly divergent. From this observation,

research on CSR seems important, in the case of SMEs, to continue

investigations in this area, in order to identify the

type of CSR practiced and the motivations so that a consensus can emerge

regarding the conceptualization of CSR Sangue Fotso

(2018). The latter attempts to apprehend

the perception that SME managers have of CSR in a given

territory and, in an environment, marked by institutional turbulence with 22

SME managers. Its results show that the practice of CSR is dependent on acts of

profit and paternalism and is a tool for employee loyalty. In this respect, social responsibility is

certainly in many ways a fiction. It remains in part a rhetorical platform

devoid of effectiveness.

The

objective of this research is to question the influence of CSR practices on

performance via a societal and environmental analysis of SMEs in the

Cameroonian context. From this problematic, the following main question

emerges: what is the impact of taking

into account CSR practices in their societal and environmental dimension on the

performance of SMEs in the Cameroonian context? To do this, we first

present the framework of the adoption of CSR practices in its perfective vision

of the performance of SMEs. We then elucidate our methodological approach.

Finally, we present and discuss the results obtained.

2. FROM THE ADOPTION OF CSR PRACTICES BY SMES TO PERFORMANCE

Many

authors Quairel and Auberger

(2005), Paradas (2006), Worthington

(2006), Spence (2007) agree that the CSR deployed by SMEs

cannot be treated in the same way as the CSR of large companies. Indeed, SMEs

are generally characterised by a hierarchical distance and even informal

working relationships. This organisational flexibility facilitates adaptation

to changes in the environment, more than it provides access to sources of

information and new ideas Abbassi and Ouriqua

(2018). However, in a controversial debate

at the heart of the apprehension of the concept of SME performance, Ajzen et al. (2016) find it deeply polysemic and

unstable in the SME literature and can be complemented by a whole series of

qualifiers that attempt, more or less, to distinguish different forms of it,

thus conferring on performance a polymorphic character. Thus, in their work,

the authors identify in the literature nine major qualifiers of performance:

social, organisational, operational, environmental, economic, financial,

accounting and stock market, human, commercial and productive and global or

unqualified.

2.1. THEORETICAL ANCHORING OF THE PERCEPTION OF ENVIRONMENTAL COMMITMENT ON THE PERFORMANCE OF THE SME

The

primary responsibility of the company is economic and consists of meeting the

expectations of its shareholders Rajan and Zingales (1998). However, this original conception

has gradually developed and broadened over time. The actions and pressures of

other stakeholders and the institutional framework in which the company

operates are now changing the situation with regard to environmental commitment

and responsibility. We will draw on stakeholder theory and neo-institutional

theory.

2.1.1. STAKEHOLDER THEORY

According

to Renaud (2009), the stakeholder theory (TPP)

places the company at the centre of all relational concerns with its third

parties, who are no longer just providers of capital, but actors interested in

the company's activities and decisions Capron and Quairel-Lanoizelee

(2007). This theory attempts to explain

why the entity must reconcile the contradictory logics of the individuals

affected by the project Freeman (1984), Carroll (1989), Pesqueux (2007), El Abboubi

and Cornet (2012), Ballet et al. (2011), Flanchec and Uzan

(2012). This vision, contrary to the

neoclassical theory of Friedman (1971) which

shows rather that the purpose of the profit-making entity is exclusively linked

to the maximisation of profit, and that social responsibility is only exercised

for the benefit of the contributors of capital, the stakeholder theory remains

much more demanding. According to Renaud (2009), this theory shows that the role of

the manager goes beyond profit maximisation. Indeed, managers seek to achieve a

balance between the different groups of people who have shares in the company Bidi (2021).

2.1.2. NEO-INSTITUTIONAL THEORY

According

to neo-institutional theory, environmental commitment is influenced by various

pressures from the socio-institutional context in which it takes place.

Neo-institutionalism is a school of thought that developed from the 1970s

onwards in the sociological analysis of organisations. Neo-institutional theory

suggests that the motivations of organisations go beyond economic optimisation

to social justifications and a quest for legitimacy Gond

and Mullenbach (2004).

It should

also be noted that among the many approaches that have been used to study CSR

to date, many have sought to determine the influence of CSR on firm performance

Orlitzky et al. (2003), Allouche and Laroche (2005), sometimes arguing that CSR

distracts firms from their true purpose, thus undermining their performance Friedman (1970), and sometimes that it actually

improves firm performance Jackson and Nelson (2004). It is noted that corporate

environmental commitment positively influences corporate performance. This

literature allows us to refine the following hypothesis:

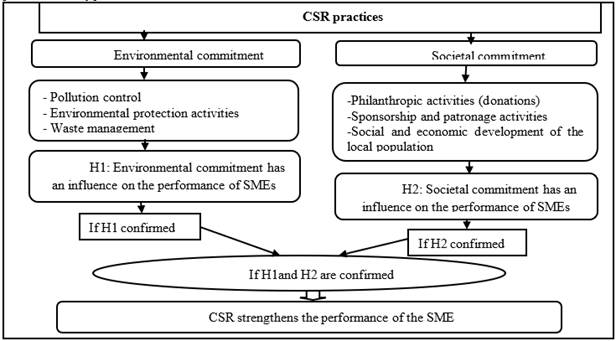

H1: Environmental commitment has a positive and

significant influence on the performance of SMEs.

2.2. THEORETICAL ANCHORING OF THE PERCEPTION OF SOCIETAL COMMITMENT ON THE PERFORMANCE OF THE SME

Purely

financial, quantitative, or one-dimensional conceptualisations of performance

reduce the benefits that can be derived from the societal approach. We note

here that societal engagement does not focus only on financial benefits but

extends to other operational and competitive benefits. Here we will mobilise

the theory of competitive advantage and the theory of resource dependency.

2.2.1. THE THEORY OF COMPETITIVE ADVANTAGE

According

to many authors, companies can use their charitable efforts to improve their

competitive environment Porter and Kramer (2002), Mcalister and Ferrel

(2002). Using philanthropy to improve the

environment helps to reconcile social and economic objectives and improve the

long-term prospects of the company. This is particularly relevant in a

developing economy where the social needs of people must be addressed in order to stabilise the economy and communities. Once

economic stability is achieved, the loyalty and trust of the people served by

philanthropy can translate into future consumers and employees for these

businesses. Not all corporate spending will bring benefits, and not all social

benefits will improve competitiveness, but at some point, there will be a

convergence of interests that will result in social and economic benefits Porter and Kramer (2002). Moreover, CSR appears to bring

substantial gains, both economically and for the company's key stakeholders.

However, these gains are not a factor of competitive advantage Crest (2019). In his study, Barić (2017) raises the importance of the

relationship between organisations and their stakeholders and that the quality

of this relationship represents a key factor on success and differentiation

from competitors.

2.2.2. RESOURCE DEPENDENCY THEORY

This

theory emphasises the dependence of the firm on actors in its environment and

argues that the sustainability of the firm depends on its ability to manage the

demands of different groups. Firms need the consensus of the society in which

they operate and in particular of the groups that

provide them with key resources. Resource dependency theory places CSR within

the traditional economic view of corporate objectives. Firms engage in CSR when

forced to do so in order to meet the pressures and

expectations of resource providers. This study aims to contribute to the

previous literature on a possible relationship between corporate social

performance and financial performance by analysing a sector that has not yet

been explored, namely the food industry and retailers. Knowing that 'engaged consumption seems to be more of a

sustainable consumption trend than a fad', it is clear

that food companies have generally invested in societal issues. This

allows us to formulate the second hypothesis, which is the following:

H2: Societal commitment has a positive

influence on the performance of SMEs.

3. METHODOLOGICAL CHOICES OF THE RESEARCH

This

section explores the fundamentals of this research, from the presentation of

the sample, through the identification of variables based on the study

hypotheses presented above to the choice of the analysis model.

3.1. SAMPLING

In the

context of our study, data were collected through questionnaires administered

to the managers of SMEs selected using the

probabilistic simple random sampling method of the National Institute of

Statistics of Cameroon. To this end, 290 questionnaires were administered in

three cities representative of the Cameroonian economy, namely: Douala (124

enterprises), Yaoundé (107 enterprises) and Bafoussam

(59 enterprises) for a return of 143 usable questionnaires. It should be noted

that the choice of the questionnaire is due to the advantage it offers to

respondents in terms of the availability of the time needed to gather the

information to be provided. Indeed, we have emphasised the heterogeneity of the

sectors in order to favour the richness of the data collected.

3.1.1. OPERATIONALISATION OF EXPLANATORY VARIABLES

For a

thorough analysis, it is first necessary to operationalize the concepts of our

research. Table 1

Table 1

|

Table 1 Identification of the Dimensions of the Explanatory Variables and Operationalization of the Items |

|||

|

Concept |

Dimension |

Indicators |

Number of items |

|

|

Social commitment (The company internally) |

Social climate in companies |

1 |

|

|

|

Gender parity |

1 |

|

|

|

Employee remuneration |

1 |

|

|

|

Working and safety conditions |

1 |

|

|

|

Career process |

1 |

|

|

|

Employee training |

1 |

|

Corporate Social Responsibility |

Societal Commitment (The company with the rest

of society) |

Social and economic

development of the local population |

1 |

|

|

|

Philanthropic activities (donations) |

1 |

|

|

|

Sponsorship and patronage activities |

1 |

|

|

|

Combating pollution |

1 |

|

|

Environmental |

Environmental protection activities |

1 |

|

|

Commitment |

Waste management |

1 |

|

|

|

Environmental risk

prevention and management policy |

1 |

|

|

Economic responsibility |

The enterprise is qualified

here as an institution that produces goods or services to be sold on a market. |

1 |

This

research aims to demonstrate the influence of CSR practices on the performance

of

SMEs. The

study is structured around hypotheses that we seek to test in the field. Figure 1 below present the hypotheses of

this research.

Figure 1

|

Figure 1 Summary of Research Hypotheses |

3.1.2. CONSTRUCTION OF THE VARIABLE TO BE EXPLAINED

Performance

in African SMEs is measured using a number of

indicators such as growth in turnover, market share and growth in net profit Feudjo (2006). In this research, we focus on the

evolution of market share and turnover growth as illustrated in the following

table: Table 2

Table 2

|

Table 2 Highlighting of the Variable to be Explained |

||

|

|

Variables to be explained |

|

|

Variables |

Modality of the couple

(Market share and turnover) |

Perf |

|

Market shares (Pm) |

One-dimensional variable |

~ 1 |

|

Turnover (CA) |

One-dimensional variable |

~ 1 |

We assume

that the socially responsible SME is more successful than its counterpart that

does not display the responsibility dimension in its management function.

3.2. DATA ANALYSIS MODEL: METHOD AND INSTRUMENTS

The

Multiple Correspondence Analysis (MCA) used in the processing of the data

requires that the variables retained be dichotomised to facilitate the

interpretation of the results. Indeed, the logistic regression model, which

offers the possibility of obtaining the probability of an event, allowed us to

measure the influence of the explanatory variables on the performance of the

SMEs in our sample. This estimation of the model from the sample of

observations under study was done by the maximum likelihood principle. This

means that at each step the variable with the worst significance is excluded

from the next model according to the Wald test. This process will be repeated

until a model is obtained where all variables have a significance of 5% or

less. Moreover, the estimation of the coefficients is preceded by the

determination of some parameters of the model, namely the Lambda likelihood

ratio statistic (-2log-likelihood), the associated critical probability (P

(>chi. 2)). As a result, the Lambda likelihood ratio statistics give 63.05

for Corporate social climate, 62.37 for Working conditions and safety, 60.04

for Employee training,

69.482

for Philanthropic activities, 55.07 for Sponsoring activities, 59.23 for

Pollution control, 67.32 for Environmental protection activities and 55.58 for

Economic responsibility with associated critical probabilities of 0.00.

4. PRESENTATION OF RESEARCH RESULTS

CSR

practices are a juxtaposition of traditional values, and the manifest will of

managers in Cameroonian SMEs. With regard to the

objectives of this research, the results of the analysis are grouped into three

points addressed successively.

4.1. APPRECIATION OF ENVIRONMENTAL AND SOCIETAL ISSUES IN SMES

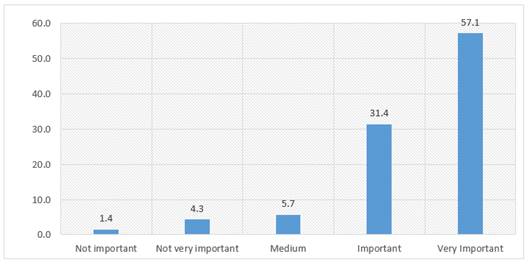

Figure 2 below summarises the descriptive

characteristics of the perception of CSR practices by the managers of the SMEs

that voluntarily participated in the study.

Figure 2

|

Figure 2 Perception of CSR in SMEs |

With

regard to the evaluation of CSR practices relating to environmental issues

within these companies, the results show that out of 70 individuals

interviewed, 57.1% perceive these practices as "very important",

31.4% consider them to be "important", 5.7% give an

"average" opinion, 4.3% declare these practices to be "not very

important" and finally 1.4% of our sample consider them to be "not

very important". The majority of SME managers surveyed consider CSR

practices relating to environmental issues to be very important within SMEs in

the Cameroonian context.

Table 3

|

Table 3 Environmental Commitment |

|||

|

|

Yes |

No |

Commentary |

|

Do you allocate a budget to

environmental issues in your company? |

35,7 % |

64,3 % |

64.3% refusal on the question |

|

Has an environmental

structure been created in the company? |

38,6 % |

61,4 % |

61.4% refusal on the question |

|

Is there a mechanism for

environmental protection? |

58,6 % |

41,4 % |

58.6% positive on the question |

|

Do you have a recycling or

waste treatment facility in your company? |

62,9 % |

37,1 % |

62.9% positive on the question |

|

Are you ISO certified

within your organisation? |

17,1 % |

82,9 % |

82.9% refusal on the question |

|

Have you taken steps to reduce your water consumption? |

38,6 % |

61,4 % |

61.4% refusal on the question |

|

In your organisation, have

you taken measures to reduce your electricity consumption? |

48,6 % |

51,4 % |

51.4% refusal on the question |

|

Within your organisation,

have you taken measures to reduce your polluting emissions (greenhouse gases,

noise, odour) etc.? |

62,9 % |

37,1 % |

62.9% positive on the question |

|

Does your company have a

social, ethical or environmental code or charter? |

17,1 % |

82,9 % |

82.9% positive on the question |

This

section provides us with information on the elements or indicators of the

descriptive statistics on social commitment as illustrated in the following Table 4:

Table 4

|

Table 4 Elements or Indicators of Descriptive Statistics on Societal Engagement |

||||

|

|

Yes |

No |

Sometimes |

Comments |

|

Do you have specific

policies against gender discrimination? |

20,0 % |

80,0 % |

0 % |

80.0% refusal on the question |

|

Have you ever had to

recruit disabled people of any kind into your company? |

38,6 % |

61,4 % |

0 % |

61.4% refusal on the question |

|

Has your company put in

place measures for the forward-looking management of jobs and skills (GPEC)? |

75,7 % |

24,3 % |

0 % |

75.7% positive on the question |

|

Does your company have a

QHSE (Quality, Health, Safety and Environment) policy |

82,9 % |

17,1 % |

0 % |

89.9% positive on the question |

|

Does the company engage in

philanthropic activities (donations) |

28,6 % |

34,3 % |

37,1 % |

37.1% positive on the question |

|

Does the company engage in

patronage, sponsorship (sponsorship of

events) |

21,4 % |

58,6 % |

20,0 % |

58.6% refusal on the question |

|

Does the company participate

in the socioeconomic development of the local population? |

30,0 % |

37,1 % |

42,9 % |

42.9% affirmative on the question |

From

these two tables, we notice that organisational behaviour is an important

prerequisite for the implementation of CSR practices in SMEs Sangue Fotso

(2018). However, it does not show the

priority of social commitment due to the dominant role of the manager which is

linked to his personal values. Yet, the awareness of managers in SMEs on the

issues related to their activities leads them to reconcile social and economic,

environmental, and cultural logics.

4.2. REGRESSION RESULTS

The

tables of the different estimates according to the selected financial

performance variables are presented below. The abbreviations of the different

variables in these tables read as follows: CSE1=Corporate Social Climate,

CTS2=Corporate Safety and Working Conditions, FEm3=Employee Training,

APh4=Philanthropic Activities, ASp5=Sponsoring Activities, LCP6=Light Pollution

Control, APE7=Environmental Protection Activities and REc8=Economic

Responsibility.

Table 5

|

Table 5 Estimation of the Coefficients of the "Market Share" Model |

|||||

|

Variables |

B |

E.S. |

Wald |

Sig. |

Exp(B) |

|

SSC1 |

2,371 |

1,179 |

4,046 |

,044 |

10,712 |

|

CTS2 |

-2,015 |

,801 |

6,330 |

,012 |

,133 |

|

ASp5 |

3,201 |

1,432 |

9,982 |

,003 |

65,111 |

|

FEm3 |

1,920 |

,719 |

7,130 |

,008 |

6,824 |

|

REc8 |

4,241 |

1,264 |

11,249 |

,001 |

69,480 |

|

APh4 |

-1,604 |

,754 |

4,518 |

,034 |

,201 |

|

LCP6 |

2,354 |

,745 |

9,234 |

,034 |

6,675 |

|

APE7 |

3,654 |

,312 |

10,003 |

,007 |

67,345 |

|

Constant |

-3,800 |

1,223 |

9,647 |

,002 |

,022 |

All the

explanatory variables finally retained in the above table are significant at

most at the 5% level. The difference in the signs of the coefficients means

that some (CTS2 and APh4) have a negative influence on the performance

represented here by the company's market shares. However, the other variables

(CSE1, ASp5, FEm3, REc8, LCP6; and APE7) tend to act in the opposite direction.

In addition, all these variables show their capacity to justify the behaviour

of the SMEs studied in their commitment and in the deployment

of CSR practices in the utilitarian current.

The

results of the field survey show that CSR practices on the social, societal,

and environmental levels are taken into account in the

managerial choices of SME managers in Cameroon. The latter perceive the

validity of CSR because it implies that a company must not only be concerned

about its profitability, but also its environmental and social impacts. As a

result, they must be more attentive to the concerns of their stakeholders.

There can be no sustainable happy shareholders without satisfied customers,

motivated and valued employees.

Table 6

|

Table 6 Estimation of the Coefficients of the Turnover Model |

|||||

|

Variables |

B |

E.S. |

Wald |

Sig. |

Exp(B) |

|

SSC1 |

1,77825 |

,920 |

10,739 |

,04928 |

,17 |

|

CTS2 |

-1,51125 |

,625 |

5,851 |

,00392 |

,22 |

|

ASp5 |

-3,18075 |

,986 |

10,408 |

,00116 |

,04 |

|

FEm3 |

1,133 |

,488 |

5,406 |

,020 |

3,11 |

|

REc8 |

2,386 |

,769 |

9,621 |

,002 |

,09 |

|

APE7 |

1,604 |

,754 |

9,518 |

,034 |

,201 |

|

LCP6 |

2,138 |

,744 |

8,251 |

,003 |

,12 |

|

Constant |

1,203 |

,588 |

4,184 |

,03944 |

,30 |

The

behaviour of performance through turnover reveals the same influencing

variables as in the previous table, with the only difference being the

variation in the signs of influence observed at the level of the variables CTS2

and ASp5. In other words, the analysis of the coefficients of the variables

relating to the social climate in companies (CST1), employee training (FEm3),

economic responsibility (REc8), environmental protection activities (APE7) and

the fight against pollution (LCP6) reveals their contribution to the

improvement of the turnover of the SMEs that deploy

CSR practices. On the other hand, working conditions and safety (CTS2) and sponsorship activities (ASp5) act in the

opposite direction. This can be seen in their negative coefficients, which are

of the order of (-1.51125) and (-3.18075), significant at the 5% threshold

(with Prob=.00392 and Prob=00116) with the value 0 for the decrease in

turnover, and the value 1 otherwise, hence the tendency for SMEs to limit

social security expenditure and sponsorship activities which have a negative

influence on their visibility in this highly competitive market.

5. DISCUSSION OF THE RESULTS

Overall,

our results show that the influence of environmental commitment on performance

is positively and significantly correlated with performance. This would be in

line with the work of Porter and Van der Linde

(1995), which led to the idea that pollution is a form of waste and

reflects inefficient procedures. The environment can serve productivity, and

pollution control (sometimes mandatory) encourages companies to find new and

more economical production processes. This hypothesis is also confirmed by the

work of Barić (2017), according to which CSR has a

positive impact on environmental practices.

With regard to societal commitment, we note that the reputation in terms of societal

responsibility remains an asset that generates future income Jouidi et al. (2022). The reputation and trust generated

by the company requires the enhancement of its external image among its

stakeholders. Indeed, the mobilisation of external stakeholders around shared

values, strategic projects and greater openness to the outside world makes it

possible to reduce social risk and create a dynamic of progress Saghroun and Eglem

(2008). Thus, we note that extra-economic

activities (environmental and societal) remain the possible lever for creating

financial value for the Cameroonian SME. Moreover, engaging in a CSR approach

can be a way of obtaining a better local anchoring, which can promote customer

loyalty. Thus, Cameroonian SMEs find their customers directly in this community

of proximity, which allows them to make sales most often on a local or regional

scale. The reputation is thus strengthened in its ecosystem.

6. CONCLUSION

The issue

of socially responsible business, whether it is more specifically related to

societal aspects or environmental issues, has received a lot of attention and

is regularly in the spotlight. By placing social issues at the heart of the SME

vision, stakeholder theory provides the theoretical framework for both the

search for a positive link between societal and environmental engagement on

performance. The disclosure of the company's commitment to responsible business

practices through the installation of environmental and recycling systems and

the provision of a social charter will indeed reduce information asymmetry and

legitimise the company in the eyes of its stakeholders. The objective of this

research is to question the influence of CSR practices on performance through a

societal and environmental analysis of SMEs in the Cameroonian context. In

addition, it attempted to shed light on the relationship between the

environmental and societal commitment of SMEs and their ability to remunerate

residual creditors.

Societal

commitment through the implementation of specific policies against gender

discrimination, the recruitment of people living with disabilities and the

altruism of SME managers to meet the expectations of different stakeholders,

improves the image of these companies in the eyes of the general

public. Moreover, satisfying the legitimate interests of stakeholders

helps to ensure the company's performance and survival objectives in terms of

increasing its market share and turnover. In this respect, it is interesting to

note that despite the craze for the notion of sustainable development, it does

not yet seem to be really reflected in the eyes of Cameroonian SME managers in

the evaluation of the company's performance. Finally, the results also suggest

a more important role for quantitative information, with general information

having less impact on financial performance. The results of the survey show the

extent of the dimensions favoured by SME managers as well as their perception

of CSR, which cannot be understood without taking into

account its economic consequences. Our results highlight that CSR is

biased by the values of the leader, his or her managerial cognition and

personal purpose. These need to be rethought to incorporate the consequences of

possible instrumental and substantive conflicts.

Thus,

from a managerial point of view, the conclusions of this research can serve as

a framework for reflection for business leaders, managers, and researchers.

They will have at their disposal strategic management tools adapted to the

African context. This will enable them to improve the relevance and

effectiveness of their performance measurement system. In

particular, if they want to improve their performance, companies should

become "citizens" by taking

into account all social, societal, and environmental concerns.

Nevertheless, the qualitative nature of the variables selected does not help us to categorically assert the contribution of CSR to performance. Also, we were only able to test probabilities of achievement, contrary to the general trend, according to which the relationship between CSR and performance is usually tested through panel data. On the one hand, the measurement instrument does not seem to cover all theoretical dimensions of the concepts due to the use of closed and semi-open questions. This implies that the approach is not immune to subjectivity. Thus, further research at the international level, taking into account religious, cultural, and socio-cultural factors, may further explain the differences observed within companies in the operationalization of CSR.

CONFLICT OF INTERESTS

None.

ACKNOWLEDGMENTS

None.

REFERENCES

Abbassi, A., and Ouriqua, A. (2018). The Impact Of CSR On The Performance Of Smes In Morocco. Revue Du Contrôle De La Comptabilité Et De l'Audit, 7.

Abbassi, A., and Saidi, C. (2019). Responsible Engagement of Smes: An Analysis Through The Resources and Competencies Approach. International Journal of Management Sciences, 5(2), 210228.

Abid, R. (2020). Responsabilité Sociale Des Entreprises Envers Les Employés Et Performance Financière [Thesis] Presented In View of Obtaining The Degree of Ph. D. In Industrial Relations. Université De Montréal.

Agbovoedo, J. S., Agbede, O. P. C., and Agadame, J. T. (2022). Influence of Corporate Social Responsibility Practices on The Business Performance of Beninese Banks in the Context of COVID19 Health Crisis. International Journal of Accounting, Finance, Auditing, Management and Economics, 3(6-2), 77-94. https://doi.org/10.5281/zenodo.7371433.

Ajzen,

M., Rondeaux, G., Pichault, F., and Taskin, L. (2016). Performance and

Innovation In Smes: A Relationship to be Questioned. Revue Internationale Des

PME, 29(2), 65-94.

https://doi.org/10.7202/1037923ar.

Allouche, J., and Laroche, P. (2005). Responsabilité Sociale Et Performance Financière Des Entreprises : Une Synthèse De La Littérature, Colloque Responsabilité Sociétale Des Entreprises : Réalités, Mythes Ou Mystifications, Nancy, March.

Ballet, J., Dubois, J.L., and Mahieu, F. R. (2011). The Social Sustainability of Sustainable Development: From Omission to Emergence. Developing Worlds, 4(156), 89-110. https://doi.org/10.3917/med.156.0089.

Barić,

A. (2017). Corporate Social Responsibility And Stakeholders : Review of the

Last Decade (2006-2015). Business Systems Research Journal, 8(1), 133-146. https://doi.org/10.1515/bsrj-2017-0011.

Barnett, M. I. (2007). Stakeholder Influence Capacity and Variability of Financial Returns to Corporate Social Responsibility. Academy of Management Review, 32(3), 794-816. https://doi.org/10.5465/amr.2007.25275520.

Barney, J. B. (1991). Firm Resources and Sustained Competitive Advantage. Journal of Management, 17(1), 99-120. https://doi.org/10.1177/014920639101700108.

Bastianutti, J., and Dumez, H. (2012). Why Are Companies Now Recognized as Socially Responsible? Annales Des Mines - Gérer Et Comprendre 3, 109, 44-54. https://doi.org/10.3917/geco.109.0044

Bidi,

G. (2021). Quelle "Température RSE". Dans La Banque

Sénégalaise ? Association Francophone De Comptabilité, 2(11), 59-84. https://doi.org/10.3917/accra.011.0059.

Biwolé Fouda, J. (2014). The Choice of A CSR Strategy. Which Variables to Focus on According To Contexts? Revue Française De Gestion, 40(244), 11-32. https://doi.org/10.3166/rfg.244.11-32.

Boubakary, B., and Moskolaï, D. D. (2016). The Influence

of the Implementation of CSR on Business Strategy: An Empirical Approach Based

on Cameroonian Enterprises. Arab Economic And Business Journal, 11(2), 162-171. https://doi.org/10.1016/j.aebj.2016.04.001.

Boubakary, B., and Moskolaï, D.D. (2017). Determinants Of The Implementation Of Corporate Social Responsibility In Smes In Cameroon. Revue Économie, Gestion Et Société, 9, 1-18.

Capron, M., and Quairel-Lanoizelee, F. (2007). La Responsabilité Sociale D'entreprise. Éditions La Découverte, Collection Repères, Paris.

Charba, A. (2018). The Importance of CSR For The Company : The Main Reasons For A Company's Adherence To CSR Precepts. Revue Marocaine De Gestion Et d'Économie, 4(8), 58-78.

Crest, V. (2019). La Responsabilité Sociale Comme Source D'avantage Concurrentiel [Dissertation] Presented In View Of Obtaining The Degree of Master of Science, Option Strategy. HEC Montréal, School Affiliated To The University Of Montréal, 121.

De Chatillon, A., and Bachelard, O. (2006). Occupational Health and Safety In Smes.

Djoutsa

Wamba, L., and Hikkerova, L. (2014). Corporate Social Responsibility In

Cameroonian Smes: Assessment, Issues And Prospects, Gestion 2000, (6),

November, December, 41-66.

https://doi.org/10.3917/g2000.316.0041.

El

Abboubi, M., and Cornet, A. (2012). The Formalization of HRM In An SME

as a CSR Certification Issue. Human Resource Management Review, 83, 20-30. https://doi.org/10.3917/grhu.083.0020.

Etoundi

Eloundou, G.C. (2014). Ethics and Sustainable Development In Cameroonian

Smes. Developing Worlds, 4(168), 27-41. https://doi.org/10.3917/med.168.0027.

Flanchec, A., and Uzan, O. (2012). Corporate Social Responsibility and Global Governance, Paris. Economica, 145-155.

Freeman,

R. E., and Reed, D. L. (1983). Stockholders and Stakeholders : A New

Perspective on Corporate Governance. In. California Management Review Huizinga

(Ed.), 25(3), 88-106.

https://doi.org/10.2307/41165018.

Gond, J. P., and Mercier, S. (2006). La Théorie Des Parties Prenantes. In Allouche J. (Coord.), Encyclopédie Des Ressources Humaines (2ème Ed). Vuibert. 917-925.

Jackson, I., and Nelson, J. (2004). Values-Driven Performance : Seven Strategies For Delivering Profits With Principles'. Ivey Business Journal 69(2), 1-8.

Jean, F.R. (2006). Gouvernance Et Performance Des Entreprises Camerounaises : Un Univers De Paradoxes, Cahiers Electroniques Du CRECCI IAE, 2006 N° ISRN IAE 33/CRECCI-2006-21-EN, 21.

Jihad, E. L., and Yaagoubi, A. (2019). Impact of The Social Responsibility of Companies Listed on the Casablanca Stock Exchange On Their Financial Performance [Thesis] For The Award of The Doctorate In Economic Sciences And Management, LABEMO.

Jouidi, D., Elmeniy, M., and Elbouyousfi, A. (2022). The Hosting Framework of CSR In Morocco : What Articulation For A Contingent Approach To Specificity? Journal of Economics, Management, Environment and Law, 5(1), 117-135.

Manssori, S., and El Hamri, M. H. (2022). CSR Practices and Good Governance of Companies : An Exploration Of The Case Of Companies In The Souss Massa Region. Alternatives Managériales Economiques, 4(3), 472-491.

Mcalister, and Ferrel. (2002). The Role of Strategic

Philantropy In Marketing Strategy. European Journal of Marketing, 36(5),

689-705. https://doi.org/10.1108/03090560210422952.

Mercier, S. (2004). L'éthique Dans Les Entreprises.

Éditions La Découverte.

https://doi.org/10.3917/dec.merci.2004.01.

Oliver, C. (1991). Strategic Responses To Institutional Processes. Academy of Management Review, 16(1), 145-179. https://doi.org/10.2307/258610.

Ondoua Biwolé, V. (2012). The Cameroonian SME and Sustainable Development. Gestion. Éditions Clé. Cameroonian Smes: Assessment, Challenges and Prospects, 66, 2000, 31(6), 41.

Orlitzky, M., Schmidt, F. L., and Rynes, S. L. (2003). Corporate Social and Financial Performance : A Meta-Analysis. Organization Studies, 24(3), 403-441. https://doi.org/10.1177/0170840603024003910.

Paradas, A. (2006). 'Perception Du Développement Durable Par Les Dirigeants De Petites Entreprises : Résultats D'enquêtes', Actes Du 8ème CIFEPME. Fribourg.

Perez-Batres, L., and Doh, J. (2012). Stakeholder Pressures

As Determinants of CSR Strategic Choice: Why Do Firms Choose Symbolic Versus

Substantive Selfregulatory Codes of Conduct? Van Miller And Pisani, M. Journal

of Business Ethics. Springer, 110(2), 157-172. https://doi.org/10.1007/s10551-012-1419-y.

Pesqueux, Y. (2007). Pour Une Evaluation Critique De La

Théorie Des Parties Prenantes, In. In M. Bonnafous-Boucher and Y. Pesqueux

(Eds.), Décider Avec Les Parties Prenantes, Approches D'une Nouvelle Théorie De

La Société Civile. Éditions La Découverte, 19-40. https://doi.org/10.3917/dec.bonna.2006.01.0019.

Porter, M. E., and Kramer, M. R. (2002). The Competitive Advantage of Corporate Philanthropy. Harvard Business Review, 80(12).

Quairel,

F., and Auberger, M. N. (2005). Management Responsable Et PME : Une

Relecture Du Concept De Responsabilité Sociétale De L'entreprise, La Revue Des

Sciences De Gestion, 40(211-212), 111-126. https://doi.org/10.1051/larsg:2005010.

Rajan, R., and Zingales, L. (1998). Financial Dependence and Growth. American Economic Review, 88, 559-586.

Renaud, A. (2009). Environmental

Performance Assessment Tools : Environmental

Audits And Indicators. La Place De La Dimension

Européenne Dans La Comptabilité Contrôle Audit, Strasbourg, France. Pp.CD ROM.

Ffhalshs-00459153.

Saghroun, J., and Eglem, J. (2008). In Search of Overall Corporate Performance : The Perception of Financial Analysts. Comptabilité Contrôle Audit, 14, 93-118. https://doi.org/10.3917/cca.141.0093.

Sangue

Fotso, R. (2018). Perception of CSR By Cameroonian SME Managers. Revue

Internationale Des PME, 31(1), 129-155. https://doi.org/10.7202/1044691ar.

Sangué Fotso, R. (2011). The Effectiveness of the Control Structure of Cameroonian Firms [Phd Thesis]. University of Franche-Comté.

Schneider, S. C., and Angelmar, R. (1993). Cognition In Organizational Analysis: Who's Minding the Store? Organization Studies, 14(3), 347-374. https://doi.org/10.1177/017084069301400302.

Spence, L. J. (2007). CSR and Small Business in a European Policy Context: The Five C's Of CSR and Small Business Research Agenda. Business And Society Review, 112(4), 533-552. https://doi.org/10.1111/j.1467-8594.2007.00308.x

Wong, A., and Yameogo, U. K.S. (2011). Les Responsabilités Sociétales Des Entreprises En Afrique Francophone, Paris : Les Éditions Charles Léopold Mayer.

Worcester, R. (2009). Reflections on Corporate Reputations. Management Decision, 47, 573589. https://doi.org/10.1108/00251740910959422.

This work is licensed under a: Creative Commons Attribution 4.0 International License

This work is licensed under a: Creative Commons Attribution 4.0 International License

© Granthaalayah 2014-2023. All Rights Reserved.