ANALYSIS OF BANK SOUNDNESS LEVEL USING RGEC METHODBEFORE AND AFTER THE IMPLEMENTATION OF PSAK 71Dian Indri Purnamasari 1 1, 2 Universitas Pembangunan Nasional “Veteran” Yogyakarta, Indonesia |

|

||

|

|

|||

|

Received 4 September2021 Accepted 18 September2021 Published 30 September2021 Corresponding Author Dian

Indri Purnamasari, indri80.mtc@gmail.com DOI 10.29121/granthaalayah.v9.i9.2021.4242 Funding:

This

research received no specific grant from any funding agency in the public,

commercial, or not-for-profit sectors. Copyright:

© 2021

The Author(s). This is an open access article distributed under the terms of

the Creative Commons Attribution License, which permits unrestricted use, distribution,

and reproduction in any medium, provided the original author and source are

credited.

|

ABSTRACT |

|

|

|

The

changing economic conditions require dynamic regulations on economic system

in order to keep the pace of economic growth. By the dynamic nature we mean

making constant changes in economic aspects in efforts to adapt to the

current conditions. An example could be the bank regulation which is an

important institution in distributing funds to concerned parties. The present

study aims to determine the differences in bank soundness level before and

after the implementation of PSAK 71 in Indonesian commercial banks. We

adopted assessments of Risk Profile, Earnings, Good Corporate Governance and

Capital. The study used 21 samples collected using a purposive sampling

approach. To analyze our data we used descriptive statistics, normality test,

and paired t-test. The results indicate that differences were found between

all ratios before and after the implementation of PSAK 71, except NPL ratio. |

|

||

|

Keywords: RGEC

Method, Bank, PSAK, Financial Ratio 1. INTRODUCTION Background Banks are financial

institutions that play an important role in the economy of a country.

According to AP Faure (2013), banks are

intermediaries for all parties involved in the economy; financial

institutions and the public. Therefore, they have significant role and great

impact on the economic growth of a country. With such a great role, banks

must always be monitored for their performance in order to have a positive

impact on the economy of a country. Banks that play an important role in the

economy of a country must be able to gain their customer trust. Customer

trust in the banks can be gained through their operating efficiency and

financial soundness. Soundness of banks is indicated by their capability to

conduct normal banking operations and to fulfill their entire obligation

properly in a manner that is in accordance with applicable banking

regulations (Triandaru and Budisantoso, 2006:5). In order to determine the

soundness of banks using the same approach, Bank Indonesia issued PBI

No.13/1/PBI/2011 concerning a system for assessing the soundness of

individual banks. The regulation stipulates assessment method for risk

profile, good corporate governance, earnings, and capital, or better known as

the RGEC method. In practice, the RGEC

method assesses the soundness of a bank from its operational and financial

performance. According to Dwinanda and

Wiagustini (2015), the RGEC method

focuses more on assessing the quality of management performance of a bank.

The management performance is reflected in the |

|

||

information released to the public in the form of, for example, a financial report. The financial report included bank’s performance in a certain period. The financial report of banks or companies shall comply with the rules of accounting applicable in Indonesia and should be easy to understand and analyze. In Indonesia, the rule of accounting is called Financial Accounting Standards (Standar Akuntansi Keuangan [SAK]). The SAK bases itself on the International Financial Accounting Standard (IFRS).

As the IFRS continues to develop and improve its standards, the SAK will adapt accordingly. An example would be the enactment of PSAK 71 to replace PSAK 50, 55, and 56 concerning the guide to the recognition and measurement of financial instruments. According to the General Chair of IAPI, Tarkosunaryo, issuers mostly affected by the implementation of PSAK 71 are banks and those with substantial investments in the financial sector. An example of the amended standard is that the PSAK 71 requires companies to create a backup line of credit since the beginning of the period while PSAK 55 requires a backup line of credit to be created if the risk of default is high.

The urgency of this research lies in the implementation of PSAK 71 which earlier PSAK that has made some changes in bank accounting records. Furthermore, some changes in the implementation of PSAK may affect how banks make accounting records and present information in their financial reports. Based on the above-mentioned points, we formulated the research question as follows: Are there differences in bank soundness level in terms risk profile, good corporate governance, rentability, and capital before and after the implementation of PSAK 71? The research aims to discover the empirical evidence of differences in bank soundness level in terms risk profile, good corporate governance, rentability, and capital before and after the implementation of PSAK 71.

2. LITERATURE REVIEW AND THEORETICAL DEVELOPMENT

According to Kasmir (2012), Banks are financial institutions whose main activity is to collect public funds and channel them back to the community through the services they provide. As the definition suggests, banks constitute the important pillar for the economy of a country because they are the financial intermediaries. The sources of fund for banks are: first, the bank itself; second, the fund it collects; and third, public deposits. While there are several different kinds of banks in Indonesia, most people are familiar only with the public and private banks.

According to Budisantoso and Nuritomo (2016), banks served several roles in the economy of a country, such as asset acquisition, transaction, liquidity, and efficiency. Those roles are in line with the main activities of the bank fund management. Bank can be described as a trusted financial institution. It gains the trust from the parties related to the banking activities. Being a trusted institution makes it possible for the bank to conduct its activities in the economy of a country.

3. BANK SOUNDNESS LEVEL

Bank Soundness Level is the result of the assessment of Bank's condition performed on Bank's risks and performance. According to Santoso and Nuritomo (2014), bank soundness is the capability of a bank to perform its banking operations properly and to fullfil its banking obligations in compliance with the applicable rules. The regulation of Bank Indonesia No 13 of 2011 in article 6 states that banks are required to conduct assessment of Bank Soundness Level individually using a risk-based approach that covers risk profile, good corporate governance, earnings, and capital (subsequently abbreviated to RGEC method).

RGEC method is an independent assessment of bank soundness that replaces CAMEL method for similar assessment. The RGEC method can be used to assess inherent risk and the quality of risk management in bank’s operation using risk profile, corporate governance using good corporate governance assessment, rentability using earnings assessment, and capital using capital assessment.

4. PSAK 71

Statement of Financial Accounting Standards (PSAK 71) is a guideline on measurement and recognition of financial instruments. This standard replaces PSAK 55 which was previously applicable. This standard replacement is in compliance with the IFRS 9 that deals with similar subject. According to Henky Suryaputra (2019), the implementation of PSAK 71 that requires larger reserve accumulation has made bank profits to decrease. An important point in the PSAK 71 concerns the financial asset impairment reserves. It was stated earlier in the PSAK 55 that banks are required to reserve for losses due to uncollected loans when there are signs of bad credit. However, with the implementation of PSAK 71, banks are required to reserve for losses prior to final loan approval. Referring to the roadmap of the Financial Services Authority (OJK), the PSAK 71-Financial Instruments was implemented in the Indonesia’s banking system on 1 January 2020.

H: Differences were found in risk profile, good corporate governance, earnings, and capital before and after the implementation of PSAK 71 in the banks.

5. RESEARCH METHODS

5.1. TYPE OF RESEARCH

This study employed a quantitative research method conducted by analyzing and describing quantifiable data. We used secondary data in the form of information presented in the financial reports of the banks that have implemented PSAK 71 to determine their soundness level using RGEC method. Horizontal analysis was conducted to find differences between financial reports issued before and after the implementation of PSAK 71. The dependent variable in this study is the bank soundness level. The hypothesis testing was performed using descriptive statistics, normality test, and paired t-test. Purposive sampling is used to choose the correspondent banks to participate in the survey. The criteria for sample selection include: 1) Public and private banks that operate in Indonesia; 2) Banks that have implemented the PSAK in their financial and annual reporting; 3) Banks that publish their financial statements and annual reports; and 4) Banks listed on the Indonesia Stock exchange in 2021.

5.2. VARIABLES AND MEASURES

The assessment of bank soundness level refers to the Circular Letter of Bank Indonesia No. 13/24/DPNP dated 25 October 2021. The assessment was performed using RGEC method which includes risk profile, good corporate governance, earnings and capital. Each factor of RGEC will generate scores that reflect the bank’s conditions. Those scores were then summed up to generate the final score or the composite rating to determine bank’s soundness level. In conformity with the Circular Letter of Bank Indonesia No. 13/24/DPNP, the composite rating helps identify the soundness level as follow:

1) Composite 1 is rated as “excellent”

2) Composite 2 is rated as “very good”

3) Composite 3 is rated as “good”

4) Composite 4 is rated as “fair”

5) Composite 5 is rated as “poor”

6. RESULTS AND DISCUSSION

The research studied the financial statements, annual reports, and quarterly reports of banks selected using purposive sampling method. It is conducted to obtain the banks’ financial data which include Loan to Deposit Ratio (LDR), Net Performing Loan (NPL), Net Interest Margin (NIM), Return on Assets (ROA), Capital Adequacy Ratio (CAR), and independent assessment of Good Corporate Governance (GCG). The number of banks used as research objects is 21, resulting from the sampling based on predetermined criteria.

The reports used in this research were published in the years before and after the implementation of PSAK 71 in the banks’ financial reporting. In this research, the years before and after the implementation of PSAK 71 were 2019 and 2020, respectively. This has been compliant with the regulation of Bank Indonesia to begin the implementation on 1 January 2021. RCEG method is a self-assessment, meaning that the assessments of risk profile, good corporate governance, earnings, and capital were conducted by the banks. The banks published the results of the assessment in their financial statements, annual reports, or quarterly reports.

Risk Profile

This study focuses on two risks that can be identified using a quantitative approach and the data provided by the banks on their credit risks and liquidity risks. Credit risks can be assesed by calculating the non-performing loans (NPL) ratio and the liquidity ratio can be assessed by calculating the Loan to Deposit Ratio (LDR).

|

Table 1 Paired T-Test Results of the NPL and LDR |

||

|

Ratio |

Significance |

Description |

|

NPL |

0,832 |

Differences were not

found |

|

LDR |

0,000 |

Differences were found

|

|

Source: Processed data (2021) |

||

Table 1 presents the results of paired t-test conducted to assess the NPL and LDR. The NPL ratio is at a significant level of 0.832 which means that no significant differences were found between NPL ratios before and after the implementation of PSAK 71. Meanwhile, the LDR ratio is at a significant level of 0.00 which means that significant differences were found between LDR ratios before and after the implementation of PSAK 71.

The analysis of assessment components of bank soundness level using RGEC method generated different results. Twenty-one commercial banks in this study have normally distributed financial ratios and therefore merit discrimination testing using a single type of test. Risk profile is assessed using two ratios of NPL and LDR. The NPL ratios before and after the implementation of PSAK 71 have no significant differences. This is in line with the results of a study by Jovie Wijaya (2018) entitled “A Comparative Analysis of Financial Performance using RGEC Method Before and After IPO”. This study revealed that no significant differences were found in the assessments using RGEC method, despite an occurrence in between the two studied periods.

The widening gap between the lowest and the highest NPL ratios tells us that after the implementation of PSAK 71 some banks managed to anticipate their credit risks while others failed to do so. The NPL ratios indicate the bank is having a hard time dealing with future credit disbursement. The LRD ratios have significant differences between those in the years before and after the implementation of PSAK 71. From the analysis of descriptive statistics, we can see that LDR ratios are positively affected by the implementation of PSAK 71. The decrease in LDR percentage indicates that the bank’s liquidity has improved. The decreasing LDR percentage means that the bank’s credit is hampered.

Good Corporate Governance (GCG) assessment is intended to measure the quality of good corporate governance implementation. The assessment covers three domains: leadership structure, governance processes, and governance outcomes. GCG assessment was conducted independently by the banks with certain aspects kept secret from the general public. In the annual reports of the banks, the GCG assessments are presented in rating scale (1-5).

|

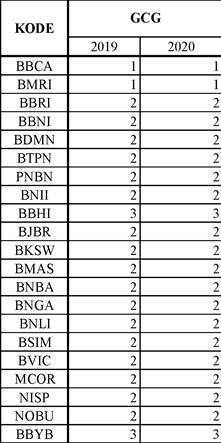

Table 2 Data on Good Corporate Governance of Commercial Banks in Indonesia |

|

|

|

Source: Processed data (2021) |

Table 2 shows us the data on self-assessment of every bank participated in this study. No changes were found in the GCG assessments from 2019 to 2020. Good Corporate Governance did not affected by the implementation of PSAK 71, because the former does not related directly to the corporate finance. The assessment of Good Corporate Governance will be affected if differences were found in the corporate governance, company management, and company problems.

Moreover, no differences were found in the assessments of Good Corporate Governance before and after the implementation of PSAK 71. This may have been because no aspect in PSAK 71 implementation that causes significant changes in the corporate governance. The regulatory changes did not lead to the reshuffling of a company’s board of directors. This is in line with a previous study that did not involve such GCG assessment.

Earnings

Rentability assessment is performed by calculating the Return on Assets and Net Interest Margin. Return on Assets (ROA) compares the profit before tax and the average total assets of banks to determine how much profit a bank is able to generate from its assets. Meanwhile, the Net Interest Margin (NIM) compares the bank's net interest with the average productive assets.

The assessment of rentability or earnings is conducted by calculating two ratios; ROA and NIM. The calculation of the two produces matching results. The discrimination test of both ROA and NIM indicates significant differences. The value of ROA is lower than that in one year earlier. This indicates a negative impact as a consequence of PSAK 71 implementation. This may have been because ROA is meant to assess banks’ capability to generate profit when, in fact, PSAK 71 affects banks’ profitability as they have to reserve more funds for the existing credits.

|

Table 3 The Results of Paired T-Test for ROA and NIM |

||

|

Ratio |

Significance |

Description |

|

ROA |

0,000 |

Differences were found |

|

NIM |

0,040 |

Differences were found |

|

Source : Processed

Data (2021) |

||

The results of paired t-test for ROA and NIM, shown in Table 3, indicated that ROA has a significance level of 0.00. This means that significant differences were found between the ROAs before and after the implementation of PSAK 71. Meanwhile, the value of NIM has a significance level of 0.040 which means that significant differences were found between the NIM values before and after the implementation of PSAK 71.

As for the NIM in 2020, the value is higher than that in 2019. Thus, the NIM value has been more positively affected than before. This means that the banks earn more interest income in 2020. Unlike the ROA that can be quickly recognized because it is related to the capital and credit, the NIM is related to the number of credit applications submitted to the banks.

Capital

Capital assessment can be performed using Capital Adequacy Ratio (CAR). This ratio indicates a bank’s ability to provide fund to anticipate the risk of financial loss. The Indonesia’s Capital Adequacy Ratio was measured at a minimum threshold of 8%. If the ratio was measured less than that, a bank is considered a poorly capitalized bank.

|

Table 4 The Result of Paired T Test

for CAR |

||

|

Ratio |

Significance |

Description |

|

CAR |

0,040 |

Differences were found |

|

Source: Processed Data

(2021) |

||

Table 4 presents the result of a paired t-test for the Capital Adequacy Ratio. The latter has a significance level of 0.40 which means that significant differences were found between the values of CAR before and after the implementation of PSAK 71.

Capital assessment can be conducted using Capital Adequacy Ratio. The data used in this research is normally distributed and significance differences were found between the values of CAR before and after PSAK 71 implementation. Those differences, from a perspective of descriptive analysis, constitute a positive change. This finding runs contrary to that of a study by Suroso (2017), entitled “The Implementation of PSAK 71 and its Impact on Banks’ Minimum Capital Adequacy Requirement.” He found that PSAK 71 implementation has a negative impact on the impairment loss reserve or CAR. The study was conducted before Bank Indonesia requires all commercial banks to adopt PSAK 71 in their financial reports in 2020. This is because the banks can maintain a stable capital adequacy ratio and anticipate the implementation of PSAK 71.

7. CONCLUSION

The results of the study mentioned earlier lead us to the conclusion that based on the discrimination test using a paired t-test, all ratios calculated using RGEC method have differences, with the exception of non-performing loan (NPL) ratio. The values of NPL ratio have a wider range compared to those in the years before the implementation of PSAK 71. Significant differences in Loan to Deposit (LDR) ratio, Net Interest Margin (NIM), and Capital Adequacy Ratio (CAR) bring positive impact. On the contrary, differences in the Return on Assets (ROA) bring a negative impact. The assessment of Good Corporate Governance in this study has been completely unaffected because PSAK 71 has nothing to do with the corporate governance of banks. This can be seen from the fact that the rank of 21 banks participated in this study has not changed at all.

One of limitations that we found in this study is that no consideration was given to other influencing factors such as the spread of COVID-19 pandemic in Indonesia in the years during which the financial reports were studied. When conducting a data search, we found that COVID-19 pandemic could be a justification for the banks for their performance. In addition, we found outlier data that needs to be excluded, especially those with extreme values. This, in turn, affects the number of data we used in this study.

REFERENCES

Anggraini, R., Yuliani, & Rasyid, H. U. (2017). Analisis Tingkat Kesehatan Bank Syariah Sebelum dan Sesudah Spin Off. Jurnal Bisnis dan Manajemen. Retrieved from https://doi.org/10.25139/ekt.v1i1.88

Armanto, W. (2018). Perbandingan Perlakuan Akuntansi Kredit Menurut PSAK 55, PSAK 71, dan Basel pada Bank Umum. Jurnal Online Insan Akuntan. Retrieved from http://www.ejournal-binainsani.ac.id/index.php/JOIA/article/view/1029

Dwinanda, & Wiagustini. (2015). Analisis Penilaian Tingkat Kesehatan Bank Pada PT. Bank Pembangunan Daerah Bali Berdasarkan Metode RGEC. E- Jurnal Manajemen Universitas Udayana, Vol. 4 No.1. Retrieved from https://ojs.unud.ac.id/index.php/Manajemen/article/view/10151

Faure, A. (2013). Banking: An Introduction. London: Quoin Institute.

Ghozali, I. (2009). Aplikasi Analisis Multivariate dengan Program SPSS. Semarang: UNDIP.

Herman, D. (2011). Manajemen Perbankan. Jakarta: Bumi Aksara.

Kasmir. (2012). Bank dan Lembaga Kuangan Lainnya. Jakarta: PT. Raja Grafindo Persada.

Kementerian Kesehatan RI. (2018). Laporan Riskedas 2018. Jakarta: Kemkes.

OJK. (2021). Roadmap Persiapan Penerapan PSAK 71. Jakarta: OJK.

Pandia, F. (2012). Manajemen Dana dan Kesehatan Bank. Jakarta: Penerbit Rineka Cipta.

Santoso, T. B., & Nuritomo. (2014). Bank dan Lemaga Keuangan. Jakarta: Salemba Empat.

Suroso. (2017). Penerapan PSAK 71 dan Dampaknya Terhadap Kewajiban Penyediaan Modal Minimum Bank. Jurnal Bina Akuntansi. Retrieved from https://doi.org/10.52859/jba.v4i2.31

Syafina, D. C. (2019). Bagaimana PSAK 71 Memengaruhi Perbankan? Retrieved from https://tirto.id/bagaimana-psak-71-memengaruhi-perbankan-ehPf

Totok, B., & Triandaru. (2006). Bank dan Lembaga Keuangan Lain. Jakarta: Salemba Empat. Retrieved from http://pustaka.usahid.ac.id/index.php?p=show_detail&id=8344

Totok, B., & Triandaru. (2014). Bank dan Lembaga Keuangan Lain Edisi Tiga. Jakarta: Salemba Empat.

Wijaya, J. (2018). Analisis Perbandingan Kinerja Keuangan Dengan Menggunakan Metode RGEC Sebelum dan Sesudah Go Public. Jurnal Raden Intan Lampung. Retrieved from http://repository.radenintan.ac.id/4818/

This work is licensed under a: Creative Commons Attribution 4.0 International License

This work is licensed under a: Creative Commons Attribution 4.0 International License

© Granthaalayah 2014-2021. All Rights Reserved.