|

|

|

|

ANALYSIS DETERMINANT OF DIVIDEND PAYOUT RATIO AND ITS IMPACT TO THE FIRM VALUE (Empirical Study On Food and Beverage Industry Issuer 2016-2019)M. Noor Salim 1 1 Mercu Buana University, Indonesia2 ibis Styles Hotel Jatibening, Indonesia |

|

||

|

|

|||

|

Received 01 August 2021 Accepted 16 August 2021 Published 30 September 2021 Corresponding Author M.

Noor Salim, m_noorsalim@gmail.com DOI 10.29121/ijetmr.v8.i9.2021.1017 Funding:

This

research received no specific grant from any funding agency in the public,

commercial, or not-for-profit sectors. Copyright:

© 2021

The Author(s). This is an open access article distributed under the terms of

the Creative Commons Attribution License, which permits unrestricted use, distribution,

and reproduction in any medium, provided the original author and source are

credited.

|

ABSTRACT |

|

|

|

The

purpose of this research is to Analyze Determinant of Dividend Payout Ratio

and Its Impact to The Firm Value (Empirical Study on Food And Beverage

Industry Issuer 2016-2019). The samples in the form of secondary data as many

as 16 companies collected from financial statements listed on the Indonesia

Stock Exchange (IDX). In this study, nine research hypotheses were

formulated. The analysis design used is quantitative data with panel data

regression method which is processed with Eviews 9 with a random effect

model. Hypothesis testing using F test, T test, and Sobel test (Path

Analysis). The results showed in direct financial performance as proxied by

the current ratio, debt equity ratio and return on assets had a positive

affect on firm value, and partially current ratio, debt equity ratio and

return on assets had a positive affect on dividend payout ratio. Directly,

current ratio, debt equity ratio and return on assets have a positive affect

on firm value. Indirectly, the dividend payout ratio is able to strengthen

the relationship between the current ratio, debt equity ratio and return on

assets to firm value. |

|

||

|

Keywords: Liquidity, Solvency, Profitability, Dividend Payout Ratio, Firm Value 1. INTRODUTION Firm value can be said

is a picture of investors about the level of success of a company, where the

value of the company often reflected in the company's stock price. The

positive relationship between the stock price of a company and firm value

shows of the increase in stock price and followed by the increase in the firm

value and otherwise. However, if firm value is higher, public's can be trust

and prospect to the company in the future will also increase. An investor often

dealing with the risks and uncertainties that difficult to predict. For to

the minimize of this, investors need different information all that deals

with the company, all the internal factor which is a company financial

performance and other external factors such as other information, for example

economic and political condition of a country or region. Information about

the performance of a company can usually be obtained through the financial

report company including information about profit and dividend produced every

piece of the company shares issued. Based on that information then investors

will have an overview of the company. Each company has a policy that has been

determined, dividend payment but all the shareholders of course want the

payment of dividends that is certain and stable. |

|

||

Stable dividends will reduce the uncertainty of the results of investment that they do. The low uncertainty of the investment will increase public trust in the company, the value of the company and the price stocks will also be increased. However, to achieve this, the company requires sales volume and profit for a nominal stable in order to produce dividends are high. The greater the volume of sales and profit is nominal it is expected that the greater to the determinant of the dividend of the company to the shareholders.

This is done in order to avoid losses and the most important thing is that the return or rate of return of shares in accordance with the expectations of investors. The company's financial performance often becomes a measurement tool of investors to take investment decisions. Every investor has the emphasis is different to the items of the financial statements. Benchmark the company's performance can be measured and determined based on the financial ratios of the company. Company's financial ratios can be found in the company's financial statements in the form of accounting information that can be used one as a base of information to take an investment decision. Investors who do fundamental analysis of the information about the financial performance of the company's internal with this information ( Kurrohman et al.(2014)). Financial ratios are mostly used as reference in view the performance of a company is the ratio of liquidity, solvency, and profitability.

|

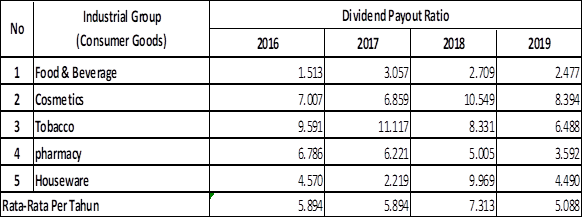

Development

of the Average Dividend Payout Ratio Industry Groups which are listed in

Indonesia stock Exchange year 2016 -2019 (in percent) |

|

|

From tabel that known level development of the average Dividend Payout Ratio (DPR) each of the industrial sector in Indonesia stock Exchange (BEI) in the year 2016-2019 experiencing fluctuations and do not indicate the presence of the application of a stable dividend policy in the sector of the food and beverage industry especially in the food and beverage industry which became the object of research. Dividend policy is one of the important decisions for the company, because the policy is related to the decision of the company in determining the magnitude of the net profit will be distributed as dividends and how much profit to be reinvested into the company in the form of retained earnings (retairned earnings). In addition, the dividend policy to be an important part of the strategy of long-term financing of the company in responding to the dynamics of the business environment. This can show the problem of determinants of the dividend policy.

|

|

|

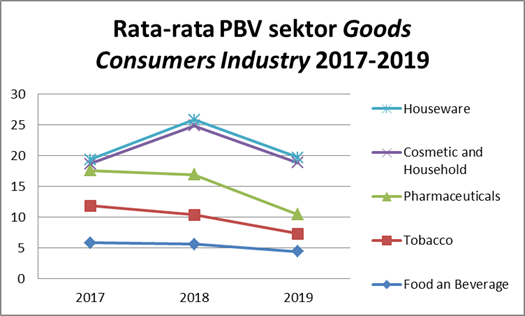

Average PBV in

goods company industry listed on BEI 2016-2019 Source : Central Bureau Of Statistics 2020 |

The value of average in sector of goods consumers industry in each sub-sector has increased and decreased normal. However on the sub-sector of houseware and cosmetics and household increases the value of PBS drastically during the year 2018 and also again on the decline during the year 2019. While other can we know the sub-sector of the pharmaceutical, tobacco industry, and also food and drinks, the value of PBV decreased every year. However, in between all sectors of industrial parts, offered food and beverage is the sector of industry that has a value of PBV is the most stable. This is because the value of PBV in the food and beverage industry decrease is not significant. With it, the author can conclude that the food and beverage industry, namely industrial sectors that have a level of stability which is good compared with the industry on the other sub-sector industry.

So therefore, with the phenomenon of the determinants of dividend payments that fluctuate every year. This will have an impact on investor interest in investing in the company and also the number of firms industry Food and Beverage Industry is likely to decline during the years 2016 to 2019, and also the value of the company Food and Beverage Industry sector tends to decrease during the year 2016 up to 2019 but it is precisely volume sale of the company Food and Beverage industry is likely to increase in the period 2016 to 2019 that have an effect on the liquidity, solvency and profitability.

2. LITERATURE REVIEW

2.1. Agency Theory

The agency theory perspective is the basis used to understand the issue of dividend payout ratio determinants and firm value. Agency theory results in an asymmetric relationship between the principal (investor) and manager (agent), to avoid this asymmetry relationship, it is necessary to clarify the dividend payout ratio in dividend policy which aims to assist investors in making stock investment decisions because it is related to the quantity of return generated. The relationship between agency theory and firm value is because in the agency relationship there is a conflict of interest between the agent and the principal. So financial performance which includes liquidity, solvency and profitability is needed by investors to see the quality of a company before making an investment.

2.2. Signaling Theory

Signaling theory explain about a boost company so that the company provide information about the condition of financial statements better for parties from both external and internal company. Such encouragement appears due to the presence of asymetry of information between external parties and the management of the company. Asymetry of information caused by the company find out more information about the company's prospects, risks that may arise and how the condition of the actual company, compared with external parties or potential investors (Suryono, 2019).

2.3. Firm Value

According from Birgham (1977) in (Metha and Gunawan (2011)), all companies have a primary goal in improving the value of the company, this effort was carried out to enhance the prosperity of the politics of shareholders. The value of the company is an important aspect of a company, this is because as the rising value of the company, prosperity and also the well-being of the shareholders will be increased as well.

![]()

2.4. Financial Ratio

Financial ratio defined as a ratio calculation using the reports from financial companies to measure and assess the financial condition and performance of a company (Hery (2016)). With this ratio, investors can determine the level of health and condition of the company at this time. In this study financial ratio used is liquidity, solvency, and profitability.

Liquidity ratio using for determine the liquidity of a company and the ability in pay short-term debt see with current assets of the company against the debt current. As for the liquidity ratio that researchers use in this study are current ratio (CR). The Current ratio is the ratio used to measure a company's ability to meet short term liabilities that will be due soon on all current assets that are owned by the company (Hery (2016)). This ratio is assumed by the study as the ratio of the right to represent the liquidity ratio. So, formula calculation of current ratio:

![]()

Solvency ratio is the ratio that used for measure a company's ability to manage debt to profit, and also to pay back the debt. Researchers using the debt to equity ratio (DER) to measure the solvency ratio in this study. DER is a ratio that measures a company's ability to repay the debt capital owned. Analysis (2011) stated that if the company's assets are obtained from the debt will have an impact on the increase of investment risk. If the company is unable to pay off its obligations according to the time that has been determined. Thus, this ratio will have an impact on the value of a company. So, formula calculation of debt to equity ratio:

![]()

The last is profitability ratio that researchers use in this study is Return on Assets (ROA). ROA is used to see the magnitude of the return of investment has been invested by the investor. So that it is relevant to the purpose of the investment made by investors in the Capital Market (Fahmi(2013)). So, formula calculation of return on assets:

![]()

2.5. Dividend Payout Ratio

The main purpose of the investment made by the investor to the company certain is to get the return. On the other hand, with the investment of the investors, the company also expects to continue to survive and develop their business. Return expected investors can be in the form of capital gains or dividend income (Ulfa and Yuniati (2016)). Stock Return proxies by the Dividend payout ratio, where the value of the house of representatives is obtained by dividing the value of the annual dividend with an annual dividend or by dividing the value of the earnings of a building stock with dividend shares/sheet (Ulfa and Yuniati (2016)). Level of dividend payout ratio can also be affected by the company's financial performance. Then, the dividend policy will affect the value of the company. So, the variable dividend policy is also often referred to as a signal to investors in assessing the condition of the company. So, formula calculation of dividend payout ratio:

![]()

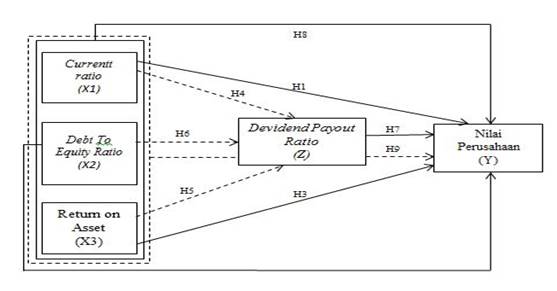

Hypothesis :

H1 : Current Ratio (CR) has positive impact on the firm value.

H2 : Debt To Equity Ratio (DER) has positive impact on the firm value.

H3 : Return On Assets (ROA) has positive impact on the firm value.

H4 : Current Ratio (CR) has positive impact on the dividend payout ratio

H5 : Debt To Equity Ratio (DER) has positive impact on the dividend payout ratio.

H6 : Return On Assets (ROA) has positive impact on the dividend payout ratio.

H7 : Dividend Payout Ratio (DPR) has positive impact on the firm value.

H8 : Current Ratio, Debt To Equity Ratio, Return On Assets simultaneously has positive impact on the firm value.

H9 : Current Ratio, Debt To Equity Ratio, Return On Assets simultaneously has positive impact through dividend payout ratio on the firm value.

3. MATERIALS AND METHODS

3.1. Population and Sample

The population in this research was 30 companies that listed in the annual financial statements of the company food and beverage industry in Indonesia stock Exchange. Samples were taken by purposive sampling technique and then obtained the 16 companies that deserve to be used as research sample. The research period is from 2016 to 2019 with a total observation research is 64.

3.2. Data Type and Source

Data used in this research is taken from secondary data sources. The financial statements obtained from the website of the Indonesia Stock Exchange website.

3.3. Data Analysis Method

The analytical method used on this research was quantitative and descriptive statistics with regression of panel data, data proceed using Eviews 9 analysis of the data with the data type of the cross-section data and time-series. There are several techniques used in the data panel, such as the Ordinary Least Square Pooled (Common Effect Model), the Fixed Effect Model (FEM), Random Effect Model (REM). The method used model of panel data that are most appropriate fot this research is Chow test, Hausman test, and Lagrange Multiplier test.

4. RESULTS AND DISCUSSION

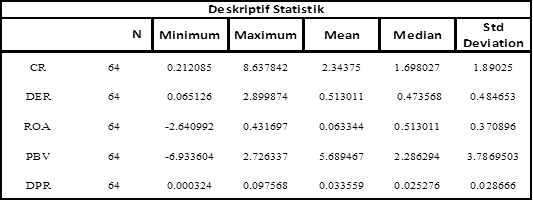

4.1. Descriptive

Statistic

|

Descriptive Statistics |

|

|

|

Source: The

results of the data processed with Eviews 9 |

4.2. Panel Data Regression

Result

The first model in

estimating panel data regression. On the model of the estimation of panel data,

there are three techniques that can be used, such as Ordinary Least Square

(OLS), Fixed Effects Model and Random Effect Model. From chow test and hausman

the most suitable model chosen is Random Effect.

4.2.1.

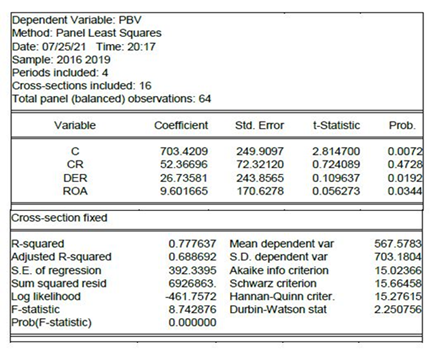

Regression Equation Model 1

After testing the

regression model of panel data has determined that random effect model the most

suitable model chosen for use in this research. Here is the results of a panel data random effect

model.

|

Regression Equation Model 1 |

|

|

|

|

A. Regression

Results

PBV = 703.4209 + 52.36696*CR + 26.73581*DER + 9.601665*ROA

B. Hypothesis

Test Results

·

Coefficient of Determination (R2)

Adjusted R-squared value of 0.777637 or 77.7637% means that the firm value variable can be explained by independent variables, namely Current Ratio, Debt Equity Ratio, and Return on Assets while the remaining 22.236% is explained by other factors outside the research model.

·

F-Test

The result for the probability F-statistic is 0.000 which is smaller than the 0.05 significance level. That is, the Current Ratio, Debt Equity Ratio, and Return on Assets simultaneously have a significant effect on firm value.

·

Partial Significance Test (T-Test)

With = 5%, df (n-k) = 59, then the value of T table is 2.00099. The results for each variable can be explained as follows:

1)

The t-statistic CR value (0.724089)

< t table 2.00099 and the probability value is 0.4728 > 0.05, meaning

that there is no direct partial effect between the CR variables on the PBV

variable.

2)

DER t-statistic value (0.109637) < t

table (2.00099) and the probability value is 0.0192 < 0.05, meaning that it

has a positive influence between the DER variable on the PBV variable partially

directly

3)

The value of t-statistic ROA (0.056273)

< t table (2.00099) and the probability value is 0.0344 <0.05, meaning

that it has a positive influence between the ROA variables on the PBV variable

partially directly

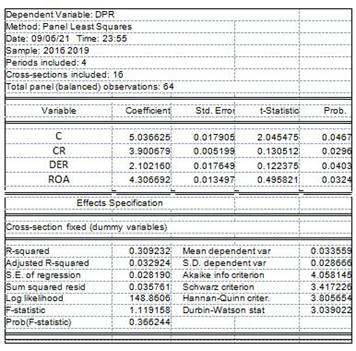

4.2.2.

Regression Equation Model 2

|

Regression Equation Model 2 |

|

|

A. Regression

Results

DPR = 5.036625 + 3.900679*CR + 2.102160*DER + 4.306692*ROA

B. Hypothesis

Test Results

·

Coefficient of Determination (R2)

Adjusted R-squared value of 0.309232 or 30.9232 % means that the mediating variable Dividend Payout ratio can be explained by independent variables, namely Current Ratio, Debt Equity Ratio, and Return on Assets while the remaining 69,0768 % is explained by other factors outside the research model.

·

F-Test

The result for the probability F-statistic is 0.366244 which is biger than the 0.05 significance level. That is, the increase in DPR is not always influenced by the company's performance simultaneously, namely the variables CR, DER, ROA.

·

Partial Significance Test (T-Test)

With = 5%, df (n-k) = 59, then the value of T table is 2.00099. The results for each variable can be explained as follows:

1)

The t-statistic CR value (0.130512)

< t table 2.00099 and the probability value is 0.0296 < 0.05, meaning

that there is a positive significant influence between the CR variable and the

DPR variable partially.

2)

The t-statistic value of DER (0.122375)

< t table (2.00099) and the probability value of 0.0403 < 0.05 means that

there is a positive significant between the DER variable on the DPR variable

partially.

3)

The ROA t-statistic value (0.495821)

> t table (2.00099) and the probability value is 0.0324 <0.05, meaning

that there is a positive significant between the ROA variable on the DPR

variable partially.

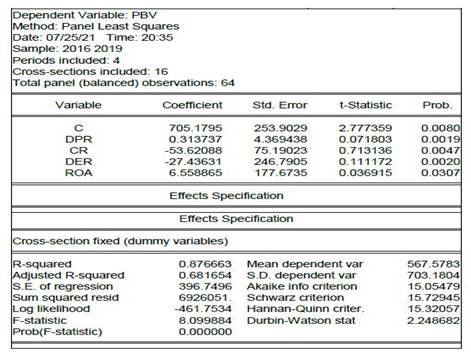

4.2.3.

Regression Equation Model 3

|

Regression Equation Model 3 |

|

|

A. Regression

Results

Y = 705.1795+ 0.313737*DPR

The t-statistic value of Dividend Payout Ratio on Price Book Value (0.9431) < t table 2.00099 and the probability value is 0.0019 <0.05, meaning that there is a significant influence between the Current Balance variable and stock return as a mediating variable.

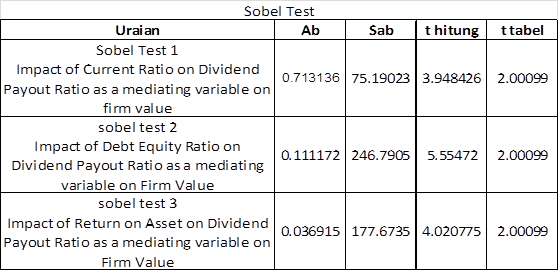

Analysis Sobel Test

According (Ghozali (2018) in the (Akhmadi et al. (2020)) sobel test has testing the strength of the indirect effect of X to Y through Z. The influence of mediation indicated by the multiplication coefficient (ab) need to be tested with the test Sobel as follows:

![]()

With count t, as follows :

![]()

With

hypotheses as follows:

Ho :

β = 0 ; No impact of Liquidity, Solvency, Profitability on Dividend Payout

Ratio as a mediating variable to the firm value.

Ha :

β ≠ 0 ; Has impact of Liquidity, Solvency, Profitability on Dividend

Payout Ratio as a mediating variable to the firm value.

Sobel test in this research using application from danielsoper.com that show the impact of the indirect Current Ratio on Firm Value mediated the Dividend Payout Ratio, the value of t count is 3.948426 < 2.00099 t table. The influence of indirect Debt Equity Ratio on Firm Value mediated the Dividend Payout Ratio, the value of t count is 5.5547195 > 2.00099 t table. No direct influence of Return On Assets on Firm Value mediated the Dividend Payout Ratio, the value of t count is 4.0207749 > 2.00099 t table.

5. DISCUSSION

1)

Partially, Current Ratio has a negative

effect on firm value, according to previous research from Salim and Susilowati (2020a) showing CR and asset growth

have a significant negative effect on firm value. While solvency and

profitability have a positive effect, according to research conducted by Anggraeni and Musaroh (2018), which shows that DER has a

significant positive effect on firm value, and Salim and Firdaus (2020) also state that ROA has a

significant positive effect on not significant effect on firm value.

2)

There is a significant positive effect

on the Dividend Payout Ratio on the Current Ratio, Debt Equity Ratio, and

Return On Assets have a direct partial effect, according to research conducted

by Gunawan and Adi (2018) showing that liquidity partially

has a positive effect on policy dividends, and Akhmadi and Robiyanto (2020) said that DER had a

significant effect on dividend policy, and Budagaga (2017) stated

that there was a significant positive ROA relationship between dividend

payments and firm value.

3)

Directly Dividend Payout Ratio has a

positive effect on firm value. This is in line with research conducted by Anton and Gabriel (2016). Dividend payout ratio has a

positive effect on firm value. Indirectly, the current ratio, debt equity

ratio, and return on assets can strengthen the relationship between the

influence of firm value through the mediating variable, namely the dividend

payout ratio. This proves that financial performance can describe the company's

profit level to get a return that is used as a dividend policy which is

expected to be distributed to shareholders, for that a good return will

certainly strengthen the company's value in the eyes of investors and

management.

6. CONCLUSION

In summary, the results of this study are as follows:

1)

Current Ratio has a negative effect on

firm value.

2)

Debt Equity Ratio has a positive and

significant effect on firm value.

3)

Return on Assets has a positive and significant

effect on firm value.

4)

Current Ratio has a positive and

significant effect on the dividend payout ratio.

5)

Debt Equity Ratio has a positive and

significant effect on the dividend payout ratio.

6)

Return on Assets has a positive and significant

effect on the dividend payout ratio.

7)

Dividend payout ratio has a positive

and significant effect on firm value.

8)

Current Ratio, debt to equity ratio and

return on assets have a positive and significant effect on firm value

simultaneously.

9)

Current Ratio, debt to equity ratio and

return on Current Ratio have a positive and significant effect simultaneously

through the Dividend Payout Ratio on firm value.

7. RECOMENDATION

This research is further expected to add to the variable external factors because the empirical findings it produces the value of R-square 0.876663 which means the independent variables used in this study can be explained 87.6% means that the dependent variable has a significant positive effect against an intervening variable, If add or use other factors that affect the determinants of dividend payout ratio and firm value not only on internal factors, but also added external factors, namely interest rates, inflation, exchange rate and economic growth, the possibility of the rest of 12.4% can explain the variation of the increase in R-square so that it can produce results that more research comprehensive.

REFERENCES

Akhmadi, Akhmadi, and Robiyanto Robiyanto (2020). "The Interaction Between Debt Policy, Dividend Policy , Firm Growth , and Firm Value." Journal of Asian Finance, Economics and Business 7(11):699-705. Retrieved from https://doi.org/10.13106/jafeb.2020.vol7.no11.699

Alenazi, Huda, and Bernard Barbour (2019). "The Relationship between Dividend Policy and Firm Value within Qatari Banks." Qscience Connect 2019(1):1-22. Retrieved from https://doi.org/10.5339/connect.2019.5

Analisa, Yangs (2011). "Pengaruh Ukuran Perusahaan, Leverage, Profitabilitas Dan Kebijakan Dividen Terhadap Nilai Perusahaan (Studi Pada Perusahaan Manufaktur Yang Terdaftar Di Bursa Efek Indonesia Tahun 2006-2008)." Universitas Diponegoro. Retrieved from http://eprints.undip.ac.id/29436/

Anggraeni, Rusandina, and Musaroh (2018). "Analisis Determinan Nilai Perusahaan Studi Pada Perusahaan Manufaktur Yang Terdaftar Di Bursa Efek Indonesia." Jurnal Manajemen Bisnis Indonesia 3:327-36. Retrieved from http://dx.doi.org/10.21831/jim.v15i2.34760

Anton, Sorin Gabriel (2016). "The Impact Of Dividend Policy On Firm Value . A Panel Data Analysis Of Romanian Listed Firms." Journal of Public Administration, Finance and Law (10):107-12. Retrieved from https://www.ceeol.com/search/article-detail?id=743810

Aprillianto, Bayu, Novi Wulandari, and Taufik Kurrohman (2014). "Perilaku Investor Saham Individual Dalam Pengambilan Keputusan Investasi: Studi Hermeneutika-Kritis." E-Journal Ekonomi Bisnis Dan Akuntansi 1 (1):16-31. Retrieved from https://doi.org/10.19184/ejeba.v1i1.567

Arieska, Metha, and Barbara Gunawan (2011). "Pengaruh Aliran Kas Bebas Dan Keputusan Pendanaan Terhadap Nilai Pemegang Saham Dengan Set Keputusan Investasi Dan Dividen Sebagai Variabel Mediasi." Jurnal Akuntansi Keuangan 13(1):13-23. Retrieved from https://doi.org/10.9744/jak.13.1.13-23

Astakoni, I. Made Purba, I. Wayan Wardita, and Ni Putu Nursiani (2020). "Ukuran Perusahaan Dan Profitabilitas Sebagai Determinan Nilai Perusahaan Manufaktur Dengan Struktur Modal Sebagai Variabel Mediasi." KRISNA: Kumpulan Riset Akuntansi 12(1):35-49. [9] Basuki, Agus Tri, and Nano Prawoto. 2016. Analisis Regresi Dalam Penelitian Ekonomi Dan Bisnis: Dilengkapi Aplikasi SPSS Dan Eviews. Jakarta: Rajawali Pers Retrieved from https://doi.org/10.22225/kr.12.1.1851.1-6

Budagaga, Akram (2017). "Dividend Payment and Its Impact on the Value of Firms Listed on Istanbul Stock Exchange: A Residual Income Approach." 7(2):370-76. Retrieved from https://www.researchgate.net/profile/Akram-Budagaga-2/publication/343350075_DIVIDEND_PAYMENT_AND_ITS_IMPACT_ON_THE_VALUE_OF_FIRMS_LISTED_ON_ISTANBUL_STOCK_EXCHANGE_A_RESIDUAL_INCOME_APPROACH/links/5f246a84458515b729f8ab3d/DIVIDEND-PAYMENT-AND-ITS-IMPACT-ON-THE-VALUE-OF-FIRMS-LISTED-ON-ISTANBUL-STOCK-EXCHANGE-A-RESIDUAL-INCOME-APPROACH.pdf

Fahmi, Irham (2013). Analisis Laporan Keuangan. Bandung: Alfabeta.

Ghozali, Imam (2018). Aplikasi Analisis Multivariate Dengan Program IBM SPSS 25. Semarang: Badan Penerbit Universitas Diponegoro. Retrieved from http://repo.unikadelasalle.ac.id/index.php?p=show_detail&id=13099

Ghozali, Imam, and Dwi Ratmono (2013). Analisis Multivariat Dan Ekonometrika Teori, Konsep Dan Aplikasi Dengan Eviews 8. Semarang: Universitas Diponegoro.

Gujarati, D.N., (2012), Dasar-dasar Ekonometrika, Terjemahan Mangunsong, R.C., Salemba Empat, buku 2, Edisi 5, Jakarta

Gunawan, I. Made Adi (2018). "The Effect Of Capital Structure, Dividend Policy, Company Size, Profitability And Liquidity On Company Value (Study At Manufacturing Companies Listed On Indonesia Stock Exchange 2014-2016)." International Journal of Economics, Commerce and Management, United Kingdom VI(6).

Hery (2016). Financial Ratio for Business. Jakarta: PT. Grasindo.

Husain, Saleh (2016). "Industri Makanan dan Minuman RI Tumbuh 8,16%" http://www.kemenperin.go.id/artikel/12163/Industri-Makanan-dan-Minuman-RI-Tumbuh-8 ,16 (diakses tanggal 25 Mei 2021).

Kountur, Roony (2005). Metode Penelitian. Jakarta: PPM. [18] Alenazi, Huda, and Bernard Barbour. 2019. "The Relationship between Dividend Policy and Firm Value within Qatari Banks." Qscience Connect 2019(1):1-22. Retrieved from https://doi.org/10.5339/connect.2019.5

Moeljadi (2014). "Factors Effecting Firm Value." South East Asia Journal of Contemporary Business, Economics and Law 5 No 2:6-15. [20] Alenazi, Huda, and Bernard Barbour. 2019. "The Relationship between Dividend Policy and Firm Value within Qatari Banks." Qscience Connect 2019(1):1-22.

Mulyana, Bambang, and Rahmatika Rini (2017). "Pengaruh Solvabilitas; Profitabilitas; Ukuran Perusahaan Serta Dampaknya Pada Return Saham Perusahaan Sub Sektor Otomotif Dan Komponennya Yang Terdaftar Di Bursa Efek Indonesia Periode Tahun 2010-2016." Jurnal Ilmiah Manajemen & Bisnis 3(1):17-30.

Salim, M. Noor, and Zaky Firdaus (2020). "Determinants of Firm Value and Its Impact on Stock Prices (Study in Consumer Good Public Companies in Idx 2014-2018)." Dinasti International Journal of Education Management and Social Science 2(1):41-54. Retrieved from https://doi.org/10.31933/dijemss.v2i1.506

Salim, M. Noor, and Rina Susilowati (2020a). "The Effect of Internal Factors on Capital Structure and Its Impact on Firm Value: Empirical Evidence From the Food and Baverages Industry Listed on Indonesian Stock Exchange 2013-2017." International Journal of Engineering Technologies and Management Research 6(7):173-91. Retrieved from https://doi.org/10.29121/ijetmr.v6.i7.2019.434

Salim, M. Noor, and Rina Susilowati (2020b). "The Effect of Internal Factors on Capital Structure and Its Impact on Firm Value: Empirical Evidence From the Food and Baverages Industry Listed on Indonesian Stock Exchange 2013-2017." International Journal of Engineering Technologies and Management Research 6(7):173-91. Retrieved from https://doi.org/10.29121/ijetmr.v6.i7.2019.434

Ulfa, Luluk Mariyah, and Tri Yuniati (2016). "Jurnal Ilmu Dan Riset Manajemen : Volume 5, Nomor 5, Mei 2016 ISSN : 2461-0593 Pengaruh Kinerja Keuangan, Asset Growth Dan Firm Size Terhadap Dividend Payout Ratio." Jurnal Ilmu Dan Riset Manajemen 5(5):1-16.

|

|

This work is licensed under a: Creative Commons Attribution 4.0 International License

This work is licensed under a: Creative Commons Attribution 4.0 International License

© IJETMR 2014-2021. All Rights Reserved.