|

|

|

|

THE EFFECT OF LEVERAGE, FIRM SIZE, AND SALES GROWTH ON INCOME SMOOTHING AND ITS IMPLICATION TO THE FIRM VALUE (STUDY ON STATE-OWNED COMPANIES LISTED IN INDONESIA STOCK EXCHANGE 2016-2019)Sri Mulyati 1 1, 2 Mercu Buana University, Indonesia. |

|

||

|

|

|||

|

Received 08 August 2021 Accepted 12 September 2021 Published 22 September 2021 Corresponding Author Sri

Mulyati, srimulyatilia@gmail.com DOI 10.29121/ijetmr.v8.i9.2021.1015 Funding:

This

research received no specific grant from any funding agency in the public,

commercial, or not-for-profit sectors. Copyright:

© 2021

The Author(s). This is an open access article distributed under the terms of

the Creative Commons Attribution License, which permits unrestricted use, distribution,

and reproduction in any medium, provided the original author and source are

credited.

|

ABSTRACT |

|

|

|

The

purpose of this research was to determine the effect of leverage, firm size

and sales growth on income smoothing and its implication to the firm value.

The population used on this research was 24 state-owned companies listed on Indonesia

Stock Exchange. The samples were determined using purposive sampling method

and there were 19 companies which selected as the samples. The analytical

method used on this research was statistic descriptive and panel data

regression and use Eviews 9 for data processing. The result of this research

showed that leverage which measured by debt-to-equity ratio has negative and

insignificant effect on income smoothing while firm size and sales growth

have negative and significant effect on income smoothing and income smoothing

itself was found to have positive and significant effect on the firm value. |

|

||

|

Keywords: Income Smoothing, Firm Value, Debt to Equity Ratio, Firm Size, Sales

Growth 1. INTRODUTION Earning profits and

maximize the value of the company is one of many reasons why a company being

established. The value of a company is reflected on the stock price and

financial performance which usually can be seen on financial statements.

Financial reports are usually used by stakeholders to determine the level of

success that is achieved by a company. Beside financial reports, stock prices

can also be used as the measurement of the companies’ prosperity. Normally, the investors

tend to like a company that has stable profit on each year. They assume, that

the more stable profit or income company get then the more stable the returns

will be received by them as well. The information that is being very noticed

by investors before deciding to invest is the company's profit. The awareness

of the importance of earnings information is often being used as an excuse by

the management to take inappropriate actions (dysfunctional behavior) such as

changing the actual profit amount and one of kind of this inappropriate

behavior known as income smoothing. On 2019, PT Garuda

Indonesia was suspected manipulating the 2018 financial statement. The case

began when the company's financial statement showed a net profit of US$

809.84 thousand in 2018 or equivalent to Rp. 11.49 billion which was ultimately

found to be misrepresentation |

|

||

information. This discrepancy was found because the company managed to earn a profit of US$ 809.84 thousand, in contrast to the conditions in 2017 where they suffered a loss of US$ 216.58 million. The company's performance was surprising because in the third quarter of 2018 the company still suffered a loss of US$ 114.08 million. Further, it was found that PT Garuda Indonesia was included the profits from PT Mahata Aero Technology in the 2018 financial statement where it should not have been included. Thus, the result that must be declared by PT Garuda Indonesia was a loss of US$ 244.96 million.

Other phenomenon of state-owned company which also attract attention due to suspected to manipulating financial statement is also happened to PT PLN (Persero) which managed to record a net profit of Rp. 11.56 trillion in the 2018 financial statement. The profit increased by 162.30% or almost three times the profit in 2017 which was Rp. 4.42 trillion. An interesting fact of the financial statement of PT PLN (Persero) is that on the third quarter of 2018, PLN still suffered a loss of Rp. 18.48 trillion due to foreign exchange of Rp. 17.32 trillion. Beside PT PLN (Persero), PT Pertamina (Persero) also experienced a similar situation where the company announced a net profit for 2018 of US$ 2.53 billion or around Rp. 35.99 trillion. Although this achievement is slightly lower than 2017 which was US$ 2.54 billion, the fact that in the third quarter of 2018 the company still recorded a profit of Rp. 5 trillion get the spotlight from various parties. From these three cases, it can be summarized that the key to increasing profits was because they treat or recognized receivables as income.

Based on these cases, it can be concluded that earnings have influence on the quality of the company's performance. The quality of the company's performance is believed to lead the company’s value. Below is an overview of state-owned companies’ value listed on Indonesia Stock Exchange during 2016-2019.

|

|

|

Figure 1 The Average of State-Owned Company Value |

The Figure 1 shows a decline in the value of state-owned companies from 2016 to 2019. This phenomenon occurs with reasons and several factors that are suspected to influence income smoothing and have implications as well on the firm value are leverage, firm size, and sales growth.

2. LITERATURE REVIEW

2.1. INCOME SMOOTHING

Income smoothing is an action that is deliberately taken by managers with the intention to give the view that company has a stable profit rate and the systematic risk that will be carried out by investors is minim Rodrigues and Florencio (2020). The effect of the income smoothing makes the information about company’s actual earnings is incorrect and the decisions that will be taken by the users are not correct as well. Income smoothing can be detected by Index Eckel and the formula is as follows:

![]()

2.2. AGENCY THEORY

Agency theory is a theory related to the contracts between shareholders (principals) and managers (agents) with assumption that each party is solely motivated by his own interests Dion (2016). Difference of interests between principal and the agent often lead to a conflict known as the agency problem Bae et al. (2018). This frequent conflict is occurred due to the condition of asymmetry information. Managers as agents are suspected to have more information about the actual state of the company. Therefore, they become motivated to use the information for their own benefit.

2.3. SIGNALING THEORY

Signaling theory explains that a good company must be able to give signals to the market with the aim of showing the company's potential to the investors. According to Bae et al. (2018), high quality companies will be more motivated to send signals compared to the low ones. As in general, investors will respond the signal by evaluating the quality of the company's performance where if the results are in accordance with what is conveyed then it will be directly impact to the value of the company.

2.4. FIRM VALUE

Firm value is an investor's perception of the company's well-being which is often associated to the stock prices or refers to the price that are willingly paid by the buyer if the company sold Jiang and Fu (2019). Firm value can be measured by several methods and one of them is Price to Book Value (PBV) ratio. The formula is as follows:

![]()

2.5. STAKEHOLDER THEORY

Stakeholder theory explains that the sustainability of an organization depends on the support from many parties that connected with the organization itself. Stakeholder theory generally identifies that company’s value is the main reason of a company's success and building a synergetic relationship with the stakeholder, not only between the shareholders and the managers but also with all related parties, is one of the methods that can be choose to create a value. Theodoulidis et al. (2017).

2.6. LEVERAGE

Leverage is a ratio that can be used to measure company's assets that are financed by the debt Anindya and Yuyetta (2020). On this research, the leverage is proxied by debt-to-equity ratio (DER) and the formula is as follows:

![]()

2.7. FIRM SIZE

Iswajuni et al. (2018) said that the size of a company can be measured by total assets or total net sales. Big companies tend to have more advantages compared to the small companies. One of the advantages that big company have is the bargaining power on financial contracts. By having bargaining power, a company will get more profit easier that the one who doesn’t. In this research, the size of the company will be measured by the total assets (Ln Total Assets).

![]()

2.8. SALES GROWTH

Sales growth reflects the company's success as seen on the total sales. Companies which have relatively stable sales rate are more reliable in fulfilling their obligations to the shareholders or creditors. The formula of the sales growth is:

![]()

|

|

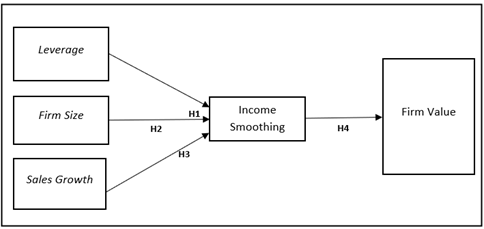

Hypothesis:

H1: Leverage has positive impact on income smoothing

H2: Firm Size has positive impact on income smoothing

H3: Sales Growth has positive impact on income smoothing

H4: Income smoothing has positive impact on the firm value

3. MATERIALS AND METHODS

3.1. POPULATION AND SAMPLE

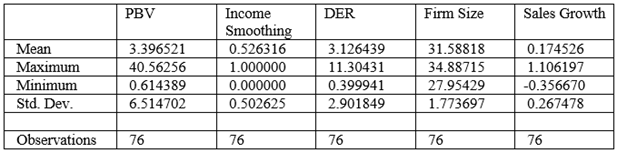

The population used on this research was 24 state-owned companies listed on Indonesia Stock Exchange. The samples were determined using purposive sampling method and there were 19 companies which selected as the samples. The period of this research is from 2016 to 2019 and the total number of observations is 76.

3.2. DATA TYPE AND SOURCE

Data used in this research is taken from secondary data sources. The data was obtained from Indonesia Stock Exchange website.

3.3. DATA ANALYSIS METHOD

The analytical method used on this research was statistic descriptive and panel data regression and use Eviews 9 for data processing. There are several techniques offered to estimate the parameters of the panel data model, such as common effects, fixed effects, and random effects. The methods used to test the most suitability panel data model is Chow test, Hausman test, and the Lagrange multiplier test.

4. RESULTS AND DISCUSSIONS

4.1. DESCRIPTIVE STATISTIC

4.2. PANEL DATA REGRESSION RESULT

4.2.1. REGRESSION EQUATION MODEL 1

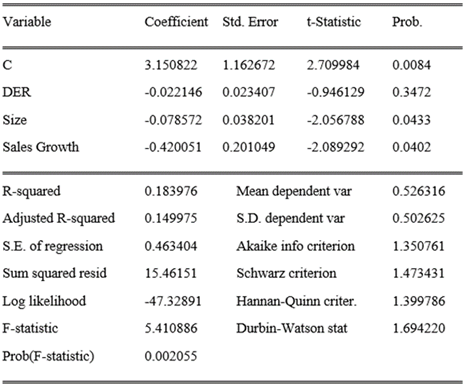

The first model is to examine the effect of the debt-to-equity ratio, firm size, and sales growth on income smoothing. The most suitable model chosen to represent the result is the Common Effect Model (CEM) and here is the result:

1) Regression

Result and Interpretation

PL= 3,150822 – 0,022146 DER – 0,078572 Size – 0,420051 Sales Growth.

Above equation is explained as below:

· The value of 3.150822 indicates that if the debt-to-equity ratio, firm size and sales growth of the sample companies are in the 0 position, then the income smoothing is 3.150822.

· The value of the debt-to-equity ratio -0.022146 indicates that DER has a negative effect on income smoothing. This means that every 1% increase of debt-to-equity ratio will decrease the income smoothing practices by 0.022146% with the assumption that other coefficients are considered constant.

· The value of firm size -0.078572 indicates that firm size has a negative effect on income smoothing. This means that every 1% increase of company size will decrease the income smoothing practices by 0.078572% with the assumption that other coefficients are considered constant.

· The value of sales growth -0.420051 indicates that sales growth has a negative effect on income smoothing. This means that every 1% increase on sales growth will decrease the income smoothing practices by 0.420051% with the assumption that other coefficients are considered constant.

2) Hypothesis

Test

· Coefficient Determination (R2)

The value of Adjusted R-squared 0.149975 or 14.99% means that the variation of income smoothing can be explained by the debt-to-equity ratio, firm size, and sales growth at the rate of 14.99% while the remaining 85.01% is explained by factors outside the model.

· F-Test

The result for F-statistical probability is 0.002055 which is smaller than the significance level of 0.05. Meaning, debt to equity ratio, firm size and sales growth simultaneously have significant effect on income smoothing.

· Partial Significance Test (T-Test)

By α = 5%, df (n-k) = 72, the value of the the T table is 1.993464. The result for each variable can be explained as follows:

1) The t-statistic value for DER 0.946129 is lower than T table 1.993464 and the probability 0.3472 is greater than 0.05. Meaning, debt to equity ratio has no insignificant effect on the income smoothing.

2) The t-statistic value for firm size 2.056788 is greater than T table 1.993464 and the probability 0.0433 is lower than 0.05 which means firm size has significant effect on income smoothing

3) The t-statistic value for sales growth 2.089292 is greater than T table 1.993464 and the probability 0.0402 is lower than 0.05 which means sales growth has significant effect on income smoothing.

4.2.2. REGRESSION EQUATION MODEL 2

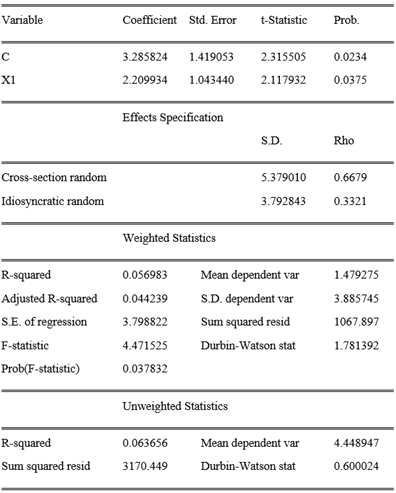

The second model is to test the effect of income smoothing on the firm value. The most suitable model chosen to represent the result is the Random Effect Model (REM). Here is the result:

1) Regression

Result and Interpretation

PBV= 3,285824 + 2.209934 PL

Above equation is explained as below:

· The value 3.285824 indicates that if the income smoothing is on 0 position, then the firm value is 3.150822.

· The value of the income smoothing 2.209934 indicates that income smoothing has a positive effect on the firm value. Meaning that every 1% increase on income smoothing will increase the firm value for 2.209934 with the assumption that the other coefficients are constant.

2) Hypothesis

Test

· Coefficient Determination (R2)

The value of Adjusted R-squared 0.044239 shows that the variation on firm value can be explained by income smoothing at the rate of 4.42% while the remaining 95.58% is explained by other factors outside the model.

· F-Test

The result for F-statistical probability is 0.037832 which is smaller than the significance level of 0.05. To conclude, income smoothing has significant effect on firm value.

· Partial Significance Test (T-Test)

By α = 5%, df (nk) = 74, the value of the t table is 1.992543 and the t-statistic value is 2.117932 which means that the value of the t-statistic is greater than the t-table and the probability value 0.0375 is lower than 0.05 which means income smoothing has significant effect on firm value.

4.3. DISCUSSION

4.3.1. THE EFFECT OF LEVERAGE ON INCOME SMOOTHING

Debt to equity ratio has negative and insignificant effect on income smoothing. It can be interpreted as a condition where company with higher debt will less motivated to manipulate the actual profit rather than the opposite ones.

The samples in this study are state-owned companies listed on Indonesia Stock Exchange. One of functions of the state-owned companies is to allocate their operational income to the state. If these companies manipulate financial statements just to show the good results when the truth is not, then it can lead to bad impact to the company's operational activities in the future. The results of this study are in line with the results of research conducted by Shabilla and Nugroho (2020) and Tasman and Mulia (2019).

4.3.2. THE EFFECT OF FIRM SIZE ON INCOME SMOOTHING

Firm size has negative and significant effect on income smoothing. State-owned companies that categorized as big companies tend to have more stable financial condition than the small ones. Therefore, the possibility of these kind companies does the income smoothing is lower. As for the companies categorized with small size will be more motivated to perform income smoothing with the intention to show their good performance to the stakeholders.

A good and stable financial condition is one of the factors that attract investors to invest their funds. Due to of these conditions, the small companies will try their best to show good financial performance to gain the trust from the stakeholders, especially the potential investors. The results of this study are in line with the research done by Holinata and Yanti (2020) and Mohammadi and Arman (2016).

4.3.3. THE EFFECT OF SALES GROWTH ON INCOME SMOOTHING

Sales growth has negative and significant effect on income smoothing. Meaning, company with lower sales growth will be more motivated to do the income smoothing and vice versa. High sales growth is believed to be one of many factors that can lead to the higher profit and in this case the higher profit a stated-owned company can get then the bigger contribution they will make to the state. These kind companies will get more credit from the investors and creditors.

Companies with the high fluctuation sales movements are considered incapable to maintain their sales trend and it gives impression that they can experience a significant increase or decrease on their profit which can later affect the companies' ability to fulfill their obligations to the shareholders and creditors. The purpose of income smoothing made by companies with low sales growth is to give a signal to the stakeholders that they still will be able to maintain their profit even though their sales level tends to decrease. This result is in line with the research conducted by Wina and Etna (2020) also Basir and Muslih (2019).

4.3.4. THE EFFECT OF INCOME SMOOTHING ON FIRM VALUE

Income smoothing has positive and significant effect on the firm value. High profit rate is believed to be one of the factors that can increase the value of the company. Beside the high profit earnings, companies with the stable profits are also considered to have same quality as companies with the high profit rates. The assumption is that companies with stable profit rates are believed to have capability to manage their financial condition and will always be able to fulfill their obligations to the stakeholders.

Investors tend to like to invest their funds to the companies whom capable providing commensurate profits and returns of their investments. The more investment received by a company then the more valuable a company will be. To achieve this goal, they become motivated to perform income smoothing in hope to increase the value of their company. This result is in line with the research conducted by Suprianto and Setiawan (2018) also Phornlaphatrachakorn and Na-Kalasindhu (2020).

5. CONCLUSIONS AND RECOMMENDATIONS

5.1. CONCLUSIONS

In summary, the results of this study are as follows:

1) Debt to equity ratio has negative and insignificant effect on income smoothing.

2) Firm size has negative and significant effect on income smoothing.

3) Sales growth has negative and significant effect on income smoothing.

4) Income smoothing has positive and significant effect on firm value.

5.2. RECOMMENDATIONS

The limitations of this study are the period

observation only 4 years and the samples used are state-owned companies with

many industries. Thus, the next researchers can extend the observation period

and use samples of state-owned companies in the same industry so that the

results will be more focus on one industrial sector.

REFERENCES

Anindya, Wina and Yuyetta, Etna Nur Afri, (2020) Pengaruh Leverage, Sales Growth, Ukuran Perusahaan dan Profitabilitas Terhadap Manajemen Laba, Diponogoro Journal of Accounting, Vol 9 Nomor 3, pp. 1 - 14.

Bae, Seong Mi, Masud, Md. Abdul Kaium, and Kim, Jong Dae, (2018) A Cross-Country Investigation of Corporate Governance and Corporate Sustainability Disclosure: A Signaling Theory Perspective, Journal Sustainability. Retrieved from https://doi.org/10.3390/su10082611

Dion, Michel, (2016) Agency Theory and Financial Crime: The Paradox of The Opportunistic Executive, Journal of Financial Crime, Emerald insight,. Retrieved from https://doi.org/10.1108/JFC-03-2015-0012

Holinata, Wilbert Jonathan and Yanti, (2020) Factors Affecting Income Smoothing, Proceedings of the 2nd Tarumanagara International Conference on the Applications of Social Sciences and Humanities. Retrieved from https://doi.org/10.2991/assehr.k.201209.046

Iswajuni, Arina Manasikana and Soetedjo, (2018) The Effect of Enterprise Risk Management (ERM) on Firm Value in Manufacturing Companies Listed on Indonesian Stock Exchange year 2010-2013, Asian Journal of Accounting Research Emerald Insight. Retrieved from https://doi.org/10.1108/AJAR-06-2018-0006

Jiang, Chun and Fu, Qiang, (2019) A Win-Win Outcome Between Corporate Eviromental Performance and Corporate Value: From the Perspective of Stakeholders, Sustainability, Vol. 11 No. 921. Retrieved from https://doi.org/10.3390/su11030921

Mohammadi, M.Y. and Arman, M.H., (2016) The Survey of Accounting Variables Effect on Income Smoothing in Stock Exchange Companies, Journal of Fundamental and Applied Sciences, Vol 8 No 2. Retrieved from https://doi.org/10.4314/jfas.v8i2s.29

Phornlaphatrachakorn, K., and Na-Kalasindhu, K, (2020) Strategic management accounting and firm performance: Evidence from finance businesses in Thailand, Journal of Asian Finance, Economics, and Business, Vol 7 No 8, pp. 309-321. Retrieved from https://doi.org/10.13106/jafeb.2020.vol7.no8.309

Rodrigues, Ramon and Florencio, Joséte, (2020) Income Smoothing Practice and Conservatism in Brazilian Credit Unions, Revista Pensamento Contemporaneo em Administracao. Retrieved from https://doi.org/10.12712/rpca.v14i1.38886

Shabilla, Annisa and Nugroho, Wawan Sadtyo, (2020) Pengaruh Financial Leverage, Ukuran Perusahaan, Profitabilitas, dan Struktur Kepemilikan Terhadap Praktik Perataan Laba, Business and Economics Conference in Utilization of Modern Technology.

Suprianto, E, and Setiawan, D, (2018) Impact of family control on the relationship between earning management and future performance in Indonesia, Business and Economic Horizon Vol 14 No 2, pp. 342-354. Retrieved from https://doi.org/10.15208/beh.2018.25

Sutama, Dedi Rossidi dan Lisa, Erna, (2018) Pengaruh Leverage dan Profitabilitas Terhadap Nilai Perusahaan (Studi pada Perusahaan Sektor Manufaktur Food and Beverage yang terdaftar di Bursa Efek Indonesia), Jurnal Sains Manajemen & Akuntansi, Vol X No 1. Retrieved from http://ojs.stan-im.ac.id/index.php/JSMA/article/view/26

Tasman, Abel and Mulia, Yudi Suci, (2019) Analisis Praktek Income Smoothing dan Faktor Penentunya Pada Perusahaan Indek LQ45 di Indonesia, E-Journal UNP, Vol 7 No 2. Retrieved from https://doi.org/10.24036/wra.v7i2.106951

Theodoulidis, Babis, Diaz, David, Crotto, Federica and Rancati, Elisa Rancati, (2017) Exploring Corporate Social Responsibility and Financial Performance through Stakeholder Theory in The Tourism Industries, Elsevier. Retrieved from https://doi.org/10.1016/j.tourman.2017.03.018

|

|

This work is licensed under a: Creative Commons Attribution 4.0 International License

This work is licensed under a: Creative Commons Attribution 4.0 International License

© IJETMR 2014-2021. All Rights Reserved.