|

|

|

|

Original Article

Examining the Role of Financial Literacy and Perceived Behavioral Control in Investment Decision-Making: Evidence from Gen Z and Millennials

|

Surbhi 1*, Dr. A.K. Govilla 2 1 Research Scholar, Department

of Economics, Malwanchal University, Indore, India 2 Supervisor, Department of Economics, Malwanchal University, Indore, India |

|

|

|

ABSTRACT |

||

|

Investment decision-making has become increasingly important in contemporary financial environments, particularly among younger and middle-aged individuals who are exposed to expanding investment opportunities, digital financial platforms, and information-rich market environments. In this context, financial literacy and perceived behavioral control have emerged as two important determinants of how individuals evaluate, plan, and execute investment decisions. The present study examined the role of financial literacy and perceived behavioral control in investment decision-making among Gen Z and Millennial respondents. The study also considered the influence of social factors and subjective norms in order to provide a broader behavioral explanation of investment behaviour. Primary data were collected from 480 respondents through a structured questionnaire, and the relationships among the constructs were assessed through structural equation modeling. The findings indicate that financial literacy significantly improves investment decision-making both directly and indirectly through perceived behavioral control. The results further show that perceived behavioral control acts as an important explanatory mechanism, suggesting that financial knowledge alone is not sufficient unless individuals also feel confident in their capacity to make sound investment choices. The generation-wise analysis reveals that these relationships remain meaningful for both Gen Z and Millennials, although the relative influence of confidence and social inputs may vary across age groups. The study contributes to the growing literature on financial behaviour by highlighting that rational investment participation is shaped not only by knowledge but also by perceived capability and behavioural readiness. The findings offer useful implications for policymakers, educators, and financial service providers seeking to improve financial decision-making among emerging and active investor groups. Keywords: Financial Literacy, Perceived

Behavioral Control, Investment Decision-Making, Gen Z, Millennials,

Subjective Norms, Social Factors, Behavioral Finance |

||

INTRODUCTION

In recent years, the financial landscape has undergone

substantial transformation due to the rapid expansion of digital investment

platforms, growing access to financial information, and the increasing

participation of younger individuals in formal investment markets. Investment

is no longer viewed as an activity limited to highly experienced investors or

high-income groups; instead, it has become a more accessible and socially

visible financial behaviour across different demographic categories. Among the

most active and emerging cohorts in this changing environment are Generation Z

and Millennials, who are gradually shaping contemporary investment patterns

through their digital exposure, social connectivity, and evolving financial

aspirations. These generations are more likely to encounter financial products,

market information, and peer-driven investment narratives through online

channels, which makes understanding their investment decision-making process an

important academic and practical concern. Investment decision-making is a

complex process influenced by economic reasoning, psychological readiness,

social environment, and individual capability. Individuals do not make

investment decisions solely on the basis of available income or market

opportunities; rather, such decisions are often guided by knowledge, beliefs,

confidence, and the perceived ability to evaluate risk and return. In this

regard, financial literacy has received considerable scholarly attention as a

foundational determinant of sound financial behaviour. Financial literacy

generally refers to the knowledge, understanding, and skills needed to make

effective financial choices in matters such as saving, borrowing, budgeting,

and investing Atkinson and Messy (2012).

Prior studies have consistently suggested that financially literate individuals

are better equipped to compare alternatives, assess consequences, and make

rational financial decisions Amagir et al. (2020), Suresh (2024). In the context of investment,

financial literacy enables individuals to understand basic financial

instruments, evaluate market information, and reduce the likelihood of

impulsive or uninformed choices.

The present study is also guided by the understanding that

investment behavior is not formed in isolation.

Social surroundings, information channels, and perceived expectations from

important others can influence how individuals think about financial

participation. Social factors such as advice from friends, family discussions,

expert opinions, and digital media content often shape investment awareness and

confidence. Likewise, subjective norms may affect whether individuals perceive

investment as a socially supported or desirable activity. Research has shown

that normative and social influences can affect investment intention,

especially when individuals are uncertain or inexperienced and therefore more

likely to rely on external cues. However, the relative importance of such

influences may differ depending on whether investors rely more heavily on

internal capability or social reinforcement. This makes it important to examine

financial literacy and perceived behavioral control

not as isolated variables, but as part of a broader behavioural framework. The

relevance of this study is strengthened by the continued growth of youth and

middle-aged participation in financial markets, the increasing need for

responsible financial decision-making, and the policy emphasis on improving

financial capability across populations. In many developing and emerging

economies, access to financial services and investment opportunities is

expanding faster than financial understanding. As a result, individuals may

enter investment environments without sufficient literacy or behavioral preparedness. Such conditions can lead to weak

decisions, poor risk assessment, or dependence on unreliable sources of advice.

Existing research has examined the influence of financial literacy on

investment decisions in a variety of contexts, including India, Pakistan, and

other emerging economies Hussain et al. (2022),

Nag and Shah (2022), Arora and Chakraborty (2023). Other studies have explored

behavioural and social determinants, including attitudes, social influence,

risk tolerance, and self-efficacy Che Hassan, et al. (2024), Nepal et

al. (2023), Vaghela

et al. (2023). However,

comparatively fewer studies have focused specifically on the combined role of

financial literacy and perceived behavioral control

in explaining investment decision-making among both Gen Z and Millennials

within a single empirical framework.

The study makes a meaningful contribution in three ways.

First, it extends the literature on financial literacy by demonstrating that

the effect of knowledge on investment decisions should be interpreted alongside

perceived control. Second, it contributes to the behavioral

finance and TPB-based literature by examining how internal capability and

social influences jointly shape decision outcomes. Third, it offers a

generational perspective by focusing on Gen Z and Millennials, two cohorts that

are increasingly influential in the financial marketplace but may differ in

their motivations, confidence, and decision processes. By analyzing

these relationships using primary data collected from 480 respondents, the

study seeks to provide evidence that is both academically relevant and

practically useful.

The remainder of the paper is structured as follows. The

next section reviews the relevant literature on financial literacy, perceived behavioral control, social factors, subjective norms, and

investment decision-making. The subsequent section presents the research

methodology, including sample design, measures, and analytical approach. This

is followed by data analysis and results, including demographic analysis and

generation-wise structural model assessment. The final sections discuss the

findings, draw conclusions, and present practical implications for financial

educators, policymakers, and investment service providers.

Review of Literature

Financial Literacy and Investment

Decision-Making

Financial literacy is widely considered an important

factor in improving investment decision-making because it helps individuals

understand financial concepts, compare alternatives, judge risk and return, and

make more informed choices. A financially literate person is generally more

capable of selecting suitable investment avenues and avoiding impulsive or

poorly informed decisions. Earlier studies have shown that financial literacy

positively influences financial behaviour and investment choices. Atkinson and Messy (2012) explained that financial

literacy is a core requirement for sound financial decisions, while Hussain et al. (2022), Nag

and Shah (2022), Arora and Chakraborty (2023),

and Suresh (2024) also reported that better

financial literacy leads to better investment-related decisions. For Gen Z and

Millennials, this relationship is highly relevant because both groups are

increasingly exposed to market information, online financial platforms, and new

forms of investment participation.

H1: Financial literacy has a significant positive

effect on investment decision-making.

Financial Literacy and Perceived Behavioral Control

Perceived behavioral control

refers to an individual’s belief that he or she is capable of performing a

particular behaviour successfully. In the context of investment, it reflects

the confidence to identify investment opportunities, understand market

situations, and take appropriate financial action. Financial literacy

strengthens this sense of control because knowledge often increases confidence

and reduces uncertainty. Amagir et al. (2020) found that financial

knowledge is linked with financial self-efficacy and behaviour, while Do et al. (2024) showed that financial knowledge significantly improves

perceived behavioral control. This means that when

people know more about financial matters, they are more likely to feel capable

of making investment decisions. This is especially important for younger and

emerging investors, who may have awareness but still lack confidence in actual

market participation.

H2: Financial literacy has a significant positive

effect on perceived behavioral control.

Perceived Behavioral Control and Investment

Decision-Making

Perceived behavioral control

plays a major role in explaining whether individuals turn financial

understanding into real investment action. Even if people have knowledge, they

may not invest unless they feel able to manage risk, evaluate alternatives, and

act with confidence. The Theory of Planned Behavior

suggests that people are more likely to perform a behaviour when they believe

they have control over it. In financial decision-making, this means that

confidence and perceived ability become important drivers of investment

behaviour. Studies such as Do et al. (2024) and Che Hassan, et al. (2024) show that

control-related beliefs significantly influence financial intention and

decision behaviour. Therefore, perceived behavioral

control is expected to directly improve investment decision-making in the

present study.

H3: Perceived behavioral

control has a significant positive effect on investment decision-making.

Social Factors, Subjective Norms, and

Investment Decision-Making

Investment decisions are not shaped by personal knowledge

alone. They are also influenced by social surroundings such as family, friends,

expert opinions, media content, and digital communities. Social factors can

shape how individuals think about investment opportunities and can also affect

their confidence and willingness to participate. Subjective norms refer to the

perceived approval or pressure from important others regarding whether a

behaviour should be performed. Earlier studies have shown that social influence

and subjective norms can affect financial and investment intentions,

particularly among young investors and socially connected groups. Tabassum

et al. (2021) suggest that social

and normative pressures often influence financial behaviour, especially when

individuals depend on external guidance. Thus, social influences are important

in understanding investment decisions among Gen Z and Millennials.

H4: Social factors have a significant positive effect

on investment decision-making.

H5: Social factors have a significant positive effect

on perceived behavioral control.

H6: Social factors have a significant positive effect

on subjective norms.

H7: Subjective norms have a significant positive effect

on investment decision-making.

Mediating Role of Perceived Behavioral Control

The literature also suggests that financial literacy may

not influence investment decisions only in a direct way. It may also improve

investment decision-making indirectly by increasing perceived behavioral control. In other words, people who are

financially literate may develop stronger confidence in their own ability, and

that confidence may further improve their decisions. This mediation logic is

supported by studies that connect knowledge, self-efficacy, control beliefs,

and financial behaviour. Do et al. (2024) and Rangga et al.

indicate that behavioral control is an important

explanatory link between financial understanding and action. Therefore,

perceived behavioral control is expected to mediate

the relationship between financial literacy and investment decision-making in

this study.

H8: Perceived behavioral

control significantly mediates the relationship between financial literacy and

investment decision-making.

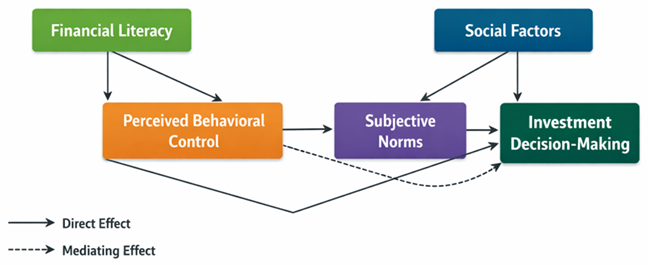

Conceptual Model of the Study

The conceptual model of the study proposes that financial literacy and social factors act as exogenous variables, while perceived behavioral control and subjective norms act as intervening variables, and investment decision-making acts as the final endogenous variable. The model assumes that financial literacy directly affects investment decision-making and also improves it indirectly through perceived behavioral control. At the same time, social factors are expected to influence investment decision-making both directly and indirectly through perceived behavioral control and subjective norms.

Figure 1

|

Figure 1 Conceptual Model of Investment Decision-Making |

Research Methodology

Research Design

The present study adopted a quantitative and descriptive

research design to examine the role of financial literacy and perceived behavioral control in investment decision-making among Gen

Z and Millennial respondents. The study was based on a structured survey

approach because the objective was to measure the relationships among

predefined constructs and test the proposed hypotheses in an empirical manner.

The design was suitable for analyzing how financial

literacy, social factors, perceived behavioral control,

and subjective norms influence investment decision-making.

Population and Sample

The target population of the study comprised individuals

belonging to Generation Z and Millennials. For the purpose of analysis, Gen Z

respondents were classified in the age group of 14–29 years, while Millennials

were classified in the age group of 30–45 years. A total of 480 valid responses

were included in the final analysis. The sample consisted of respondents from

different gender, income, and occupational categories, which helped ensure

diversity in the dataset and improved the suitability of the sample for

examining generational investment behaviour.

Data Collection and Instrument

The study was based on primary data collected through a

structured questionnaire. The questionnaire was designed to measure the major

constructs of the study, namely Financial Literacy (FL), Social Factors (SF),

Perceived Behavioral Control (PBC), Subjective Norms

(SN), and Investment Decision-Making (IDM). All items were measured using

close-ended statements. Most of the construct items were recorded on a

five-point Likert scale, ranging from lower agreement to higher agreement, while

the subjective norm items were measured on a three-point scale. The instrument

was prepared in a simple and understandable format so that respondents from

both generations could provide clear responses.

Variables of the Study

The study included Financial Literacy and Social Factors

as exogenous variables. Perceived Behavioral Control

and Subjective Norms were treated as mediating variables, while Investment

Decision-Making was considered the endogenous variable. Financial literacy

represented the respondents’ level of financial awareness and understanding.

Social factors reflected the influence of media, peers, family, and other

external information sources. Perceived behavioral

control measured the respondents’ confidence in their ability to take

investment-related actions. Subjective norms represented the role of perceived

social approval, while investment decision-making captured the extent to which

respondents made rational and structured investment choices.

Data Analysis Technique

The collected data were coded and analyzed

with the help of SPSS and SmartPLS 4. SPSS was used

for demographic analysis and descriptive statistics, while SmartPLS

4 was used for structural model assessment and hypothesis testing. The analysis

included demographic profiling of respondents, descriptive statistics of

construct items, and structural model analysis for testing direct and indirect

relationships among the variables. In addition, a generation-wise subgroup

analysis was conducted to compare the structural relationships separately for

Gen Z and Millennial respondents. This helped provide deeper insight into the

behavioural differences and similarities between the two cohorts.

Hypothesis Testing

The hypotheses of the study were tested through path

analysis and mediation analysis using SmartPLS 4. The

significance of the proposed relationships was examined through path

coefficients, t-statistics, and p-values. Relationships with significant

p-values were accepted, while statistically insignificant relationships were

rejected. The mediating role of perceived behavioral

control and subjective norms was also assessed to determine whether these

variables transmitted the effects of financial literacy and social factors on

investment decision-making.

Ethical Considerations

The study was conducted on the basis of voluntary

participation. Respondents were approached only for academic purposes, and the

information collected from them was kept confidential. The responses were used

strictly for research analysis, and no personal identity of any respondent was

disclosed in the study.

Data Analysis and Results

Demographic Profile

Table 1

|

Table 1 Demographic Profile of Respondents (N = 480) |

|||

|

Variable |

Category |

Frequency |

Percent |

|

Gender |

Male |

233 |

48.5 |

|

Female |

247 |

51.5 |

|

|

Age Group |

14–29 years (Gen

Z) |

270 |

56.3 |

|

30–45 years

(Millennials) |

210 |

43.8 |

|

|

Income |

Low Income |

186 |

38.8 |

|

Middle

Income |

156 |

32.5 |

|

|

High Income |

138 |

28.7 |

|

|

Occupation |

Student |

114 |

23.8 |

|

Private Job |

129 |

26.9 |

|

|

Self-Employed |

129 |

26.9 |

|

|

Unemployed |

108 |

22.5 |

|

|

Source: Primary

data compiled by the researcher. |

|||

The study is based

on 480 respondents. Female respondents (51.5%) are slightly higher than male

respondents (48.5%). In terms of age, 56.3% belong to Gen Z and 43.8% belong to

the Millennial group. Regarding income, 38.8% fall in the low-income category,

32.5% in the middle-income category, and 28.7% in the high-income category. The

occupational profile shows a balanced spread, with 23.8% students, 26.9%

private employees, 26.9% self-employed respondents, and 22.5% unemployed

respondents. This demographic composition indicates that the sample is

adequately diverse and suitable for studying investment decision-making among

Gen Z and Millennials.

Table 2

|

Table 2 Descriptive

Statistics |

|||||

|

N |

Minimum |

Maximum |

Mean |

Std. Deviation |

|

|

FL1 |

480 |

1.00 |

5.00 |

3.5000 |

.78344 |

|

FL2 |

480 |

1.00 |

5.00 |

3.4833 |

.77523 |

|

FL3 |

480 |

1.00 |

5.00 |

3.4938 |

.78075 |

|

FL4 |

480 |

1.00 |

5.00 |

3.4687 |

.80646 |

|

SF1 |

480 |

1.00 |

5.00 |

3.3021 |

.79034 |

|

SF2 |

480 |

1.00 |

5.00 |

3.3417 |

.78340 |

|

SF3 |

480 |

1.00 |

5.00 |

3.3083 |

.78126 |

|

SF4 |

480 |

1.00 |

5.00 |

3.3063 |

.81987 |

|

PBC1 |

480 |

1.00 |

5.00 |

2.7750 |

.79363 |

|

PBC2 |

480 |

1.00 |

5.00 |

2.7750 |

.75867 |

|

PBC3 |

480 |

1.00 |

5.00 |

2.7688 |

.82918 |

|

SN1 |

480 |

1.00 |

3.00 |

1.4479 |

.54962 |

|

SN2 |

480 |

1.00 |

3.00 |

1.4479 |

.56461 |

|

SN3 |

480 |

1.00 |

3.00 |

1.4750 |

.57741 |

|

IDM1 |

480 |

2.00 |

5.00 |

3.8792 |

.82875 |

|

IDM2 |

480 |

2.00 |

5.00 |

3.8688 |

.82590 |

|

IDM3 |

480 |

2.00 |

5.00 |

3.8854 |

.82333 |

|

IDM4 |

480 |

1.00 |

5.00 |

3.8625 |

.82615 |

|

IDM5 |

480 |

1.00 |

5.00 |

3.9000 |

.83404 |

|

Valid N (listwise) |

480 |

||||

|

Source: SPSS

output based on primary data. |

|||||

Table 2 indicates that the

items measuring Financial Literacy have mean values ranging from 3.4687 to

3.5000, suggesting that respondents generally possess a moderate level of

financial awareness and investment-related understanding. Among these items,

FL1 records the highest mean value of 3.5000, indicating that respondents tend

to believe that they have a reasonably good understanding of investment. The

standard deviations for these items remain below 1.00, which implies a moderate

but acceptable spread of responses. The Social Factors items show mean values

between 3.3021 and 3.3417. These values indicate that respondents moderately

rely on internet sources, media information, family, friends, and experts while

making investment decisions. Among the Social Factors items, SF2 reports the

highest mean, suggesting that internet and media-based financial information

have a relatively strong influence on respondents’ investment thinking. The

findings reflect the growing importance of digital information channels in financial

decision-making among younger and middle-aged investors. The Perceived Behavioral Control items record noticeably lower mean

scores, ranging from 2.7688 to 2.7750. This suggests that although respondents

may have some financial awareness, they are comparatively less confident about

their practical ability to identify profitable investments or act quickly in

stock-market settings. In other words, knowledge and confidence do not appear

to move at the same intensity, which strengthens the importance of including

Perceived Behavioral Control as a mediating construct

in the model. The Subjective Norms items register the lowest mean values,

between 1.4479 and 1.4750, on a three-point response range. These values

suggest that respondents are relatively less driven by social pressure or

social approval when thinking about stock market participation. However, since

the standard deviations remain low, the responses are fairly consistent. In

contrast, the Investment Decision-Making items produce high mean values ranging

from 3.8625 to 3.9000, indicating that respondents tend to compare investment

options, seek advice, set goals, and consider both risk and return in a

systematic manner. This pattern suggests that the sample demonstrates a

relatively rational and deliberate orientation toward investment behavior.

Generation-wise Structural Model Analysis

In order to obtain a deeper understanding of whether the

proposed conceptual model behaves similarly across the two generational

cohorts, the structural relationships were assessed separately for Gen Z and

Millennial respondents. This subgroup analysis is important because the study

is specifically concerned with understanding investment decision-making among

these two generations, which differ in terms of digital exposure, financial

experience, social environment, and life-stage responsibilities. The generation-wise

structural model assessment makes it possible to determine whether the pattern

of direct and indirect effects remains stable across cohorts or whether one

generation displays a meaningfully different investment decision process. Such

analysis adds analytical depth to the study and strengthens the interpretation

of the broader findings.

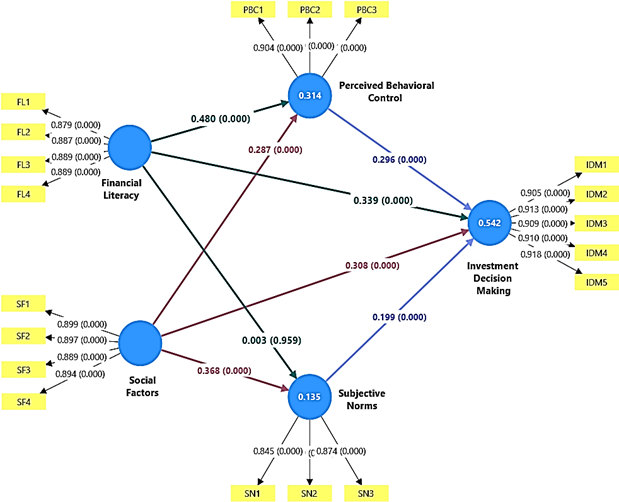

Structural Model Results for Gen Z

The Gen Z structural model results show a pattern that is largely consistent with the overall sample, while also highlighting the strong relevance of confidence-related mechanisms for younger respondents. Financial Literacy significantly influences both Investment Decision-Making and Perceived Behavioral Control among Gen Z, indicating that knowledge improves both decision quality and the perceived ability to act in financial contexts. However, Financial Literacy does not significantly affect Subjective Norms, which means that financial knowledge among this cohort does not directly translate into feelings of social approval regarding investment. Perceived Behavioral Control significantly affects Investment Decision-Making, confirming that confidence and action capability are particularly important for younger investors who may still be building practical financial experience. Social Factors significantly influence Investment Decision-Making, Perceived Behavioral Control, and Subjective Norms, suggesting that Gen Z respondents are strongly shaped by information environments, peer networks, and social reinforcement. Subjective Norms also significantly affect Investment Decision-Making, indicating that perceived approval from others contributes meaningfully to investment behaviour in this group. Overall, the Gen Z findings show that investment decisions are shaped by a combined influence of financial understanding, social exposure, confidence, and normative signals, though the route from financial literacy to social norms remains non-significant.

|

Figure 2

|

|

Figure 2 Structural Model of Investment Decision Making for Generation Z (Source: Smart PLS 4 software) |

Table 3

|

Table 3 Path Analysis and

Hypothesis Testing GEN Z |

|||||

|

Relationship |

Original Sample (O) |

STDEV |

T Statistics |

P Value |

Decision |

|

Financial Literacy → Investment Decision-Making |

0.339 |

0.048 |

7.124 |

0.000 |

H1a Supported |

|

Financial Literacy → Perceived Behavioral Control |

0.480 |

0.044 |

10.826 |

0.000 |

H2a Supported |

|

Financial Literacy → Subjective Norms |

0.003 |

0.061 |

0.051 |

0.959 |

H3a Not Supported |

|

Perceived Behavioral

Control → Investment Decision-Making |

0.296 |

0.049 |

6.086 |

0.000 |

H4a Supported |

|

Social Factors → Investment Decision-Making |

0.308 |

0.044 |

7.038 |

0.000 |

H5a Supported |

|

Social Factors → Perceived Behavioral Control |

0.287 |

0.048 |

5.972 |

0.000 |

H6a Supported |

|

Social Factors → Subjective Norms |

0.368 |

0.052 |

7.003 |

0.000 |

H7a Supported |

|

Subjective Norms → Investment

Decision-Making |

0.199 |

0.045 |

4.452 |

0.000 |

H8a Supported |

|

Source: SmartPLS

subgroup analysis for Gen Z. |

|||||

The Gen Z results in Table 3 reveal a pattern

largely similar to the overall model. Financial Literacy significantly affects

Investment Decision-Making (β = 0.339, p = 0.000) and Perceived Behavioral Control (β = 0.480, p = 0.000), thereby

supporting H1a and H2a. However, it does not significantly influence Subjective

Norms (β = 0.003, p = 0.959), leading to rejection of H3a. This indicates

that financial knowledge among Gen Z strengthens decision quality and

confidence, but not social-normative pressure. Perceived Behavioral

Control positively affects Investment Decision-Making (β = 0.296, p =

0.000), which supports H4a. Social Factors also significantly affect Investment

Decision-Making, Perceived Behavioral Control, and

Subjective Norms, supporting H5a, H6a, and H7a. Subjective Norms further

contribute positively to Investment Decision-Making (β = 0.199, p =

0.000), supporting H8a. Taken together, these results suggest that Gen Z

investment decisions are shaped by a combination of knowledge, social inputs,

confidence, and normative influence, although knowledge itself does not

directly produce normative pressure.

Table 4

|

Table 4 Mediating |

|||||

|

Relationship |

Original Sample (O) |

STDEV |

T Statistics |

P Value |

Decision |

|

Social Factors → Perceived Behavioral

Control → Investment Decision-Making |

0.085 |

0.021 |

4.125 |

0.000 |

H11a Supported |

|

Financial Literacy → Subjective Norms

→ Investment Decision-Making |

0.001 |

0.012 |

0.050 |

0.960 |

H10a Not Supported |

|

Financial Literacy → Perceived Behavioral Control → Investment Decision-Making |

0.142 |

0.027 |

5.232 |

0.000 |

H9a Supported |

|

Social Factors → Subjective Norms →

Investment Decision-Making |

0.073 |

0.019 |

3.816 |

0.000 |

H12a Supported |

|

Source: SmartPLS subgroup mediation output for Gen

Z. |

|||||

The mediation results for Gen Z indicate that Perceived Behavioral Control mediates the relationship between

Financial Literacy and Investment Decision-Making (β = 0.142, p = 0.000),

supporting H9a. Similarly, Social Factors significantly influence Investment

Decision-Making through Perceived Behavioral Control

(β = 0.085, p = 0.000), supporting H11a, and through Subjective Norms

(β = 0.073, p = 0.000), supporting H12a.

However, Subjective Norms do not mediate the relationship

between Financial Literacy and Investment Decision-Making for Gen Z (β =

0.001, p = 0.960), resulting in rejection of H10a. This means that for Gen Z,

financial knowledge improves investment outcomes primarily through enhanced

personal capability rather than through social expectation channels.

Table 5

|

Table 5 Coefficient of Determination (R²) |

||

|

Construct |

R² |

Adjusted R² |

|

Investment Decision-Making (IDM) |

0.542 |

0.538 |

|

Perceived Behavioral

Control (PBC) |

0.314 |

0.310 |

|

Subjective Norms (SN) |

0.135 |

0.133 |

|

Source: SmartPLS

subgroup analysis for Gen Z. |

||

The R² values for Gen Z show that the model explains 54.2

percent of the variance in Investment Decision-Making, 31.4 percent of the

variance in Perceived Behavioral Control, and 13.5

percent of the variance in Subjective Norms. Compared with the overall model,

the explanatory power for Investment Decision-Making is slightly higher in the

Gen Z subgroup, suggesting that the proposed framework is particularly suitable

for explaining the investment behavior of this

generation.

Discussion

The present study adopted a quantitative, descriptive, and

cross-sectional research design to examine the role of financial literacy and

perceived behavioral control in investment

decision-making among Gen Z and Millennial respondents. A survey-based approach

was considered suitable because the study aimed to empirically test the

relationships among behavioral and financial

constructs through measurable responses collected from a relatively large

number of participants. The focus on financial literacy and investment

behaviour is supported by earlier studies which have shown that financial

knowledge, self-efficacy, control, and behavioral

influences play an important role in shaping financial choices and investment

actions Amagir et al. (2020), Herawati

et al. (2018), Nepal et

al. (2023), Vaghela

et al. (2023). The target population

of the study consisted of individuals from Generation Z (14–29 years) and

Millennials (30–45 years), as these two cohorts represent active and emerging

participants in modern financial environments.

Previous studies have also emphasized that younger

generations are increasingly influenced by financial literacy, behavioral finance factors, and changing investment

attitudes in both traditional and digital contexts Moreno-Herrero

et al. (2018), Sajeev

et al. (2021), Widhiastuti et al. (2024). The study was based

on primary data, and a total of 480 valid responses were included in the final

analysis. The respondents belonged to different categories of gender, income,

and occupation, making the sample sufficiently diverse for analyzing

generational investment behaviour. Data were collected through a structured

questionnaire prepared in a simple and clear format to ensure that respondents

could understand the statements easily and respond accurately. The

questionnaire measured the main constructs of the study, namely Financial

Literacy (FL), Social Factors (SF), Perceived Behavioral

Control (PBC), Subjective Norms (SN), and Investment Decision-Making (IDM).

Most of the items were measured on a five-point Likert scale, while the items

related to subjective norms were measured on a three-point scale. The inclusion

of these constructs was grounded in prior literature which suggests that

financial literacy, social influences, and control-related beliefs are major

determinants of financial and investment behaviour Naiwen et al. (2021), Tabassum

et al. (2021), Che Hassan, et al. (2024), Do et al. (2024). In the conceptual

framework, financial literacy and social factors were treated as exogenous

variables, perceived behavioral control and

subjective norms were treated as mediating variables, and investment

decision-making was taken as the endogenous variable. Financial literacy

represented respondents’ understanding of financial concepts and investment

matters, while social factors represented the influence of peers, family,

media, and other external information channels.

Perceived behavioral control

referred to the level of confidence and perceived capability of respondents to

make and execute investment decisions, an idea supported by earlier research

highlighting the role of control, self-efficacy, and behavioral

readiness in financial action. Subjective norms reflected the social approval

or pressure perceived by respondents regarding investment behaviour, while

investment decision-making referred to the extent to which respondents compared

alternatives, evaluated risk and return, sought advice, and made rational

financial choices. After data collection, the responses were coded and analyzed using SPSS and SmartPLS

4. SPSS was used for demographic analysis and descriptive statistics, including

frequency, percentage, mean, minimum, maximum, and standard deviation values. SmartPLS 4 was used for structural model analysis, path

analysis, mediation analysis, and generation-wise subgroup analysis in order to

test the proposed relationships more comprehensively. The use of such model-testing

procedures is consistent with earlier studies examining financial literacy and

investment-related behavioural relationships. The hypotheses were tested

through path coefficients, t-statistics, p-values, and coefficient of

determination (R²) to assess both direct and indirect effects among the study

variables. In addition, separate structural analysis was conducted for Gen Z

and Millennial respondents to identify whether the relationships among the

constructs differed across the two generations.

The mediation role of perceived behavioral

control and subjective norms was also examined, particularly because prior

research indicates that financial knowledge often influences behavioural

intention and decision-making through control beliefs and internal confidence

rather than only through direct pathways. The study was conducted strictly for

academic purposes, participation was voluntary, and the confidentiality of the

respondents was maintained throughout the research process. Overall, the chosen

methodology was considered appropriate because it combined a structured survey

design, clearly defined constructs, adequate sample size, and suitable

statistical tools to examine the behavioural and financial determinants of

investment decision-making among Gen Z and Millennials in a comprehensive

manner.

Conclusion and Implications

The study concludes that financial literacy and perceived behavioral control are important determinants of investment

decision-making among Gen Z and Millennials. The findings show that respondents

with better financial knowledge are more likely to make rational and informed

investment decisions. However, knowledge alone is not sufficient unless

individuals also feel confident in their ability to understand market

conditions and take appropriate investment actions. In this context, perceived behavioral control plays a significant role by

strengthening the effect of financial literacy on investment decision-making.

The study also finds that social factors and subjective norms contribute to

investment behaviour, especially among younger respondents, but their influence

is weaker than the role of financial literacy and personal control. Overall,

the study establishes that investment decisions are shaped by a combination of

financial understanding, confidence, and social influence, with perceived behavioral control acting as an important link between

knowledge and action.

Implications of the Study

·

For policymakers: Financial awareness programs

should focus not only on knowledge but also on building confidence for

practical investment decisions.

·

For educational institutions: Colleges and

universities should introduce financial literacy and investment education in a

more practical form.

·

For financial service providers: Investment

platforms should be made simple, clear, and user-friendly for Gen Z and

Millennial investors.

·

For young investors: Better financial knowledge

can improve decision quality, but confidence and control are equally important.

·

For researchers: The study provides scope for

further research on behavioral and generational

factors affecting investment decisions.

ACKNOWLEDGMENTS

None.

REFERENCES

Achtziger, A.,

Hubert, M., Kenning, P., Raab, G., and Reisch, L. (2015). Debt Out Of Control: The Links

Between Self-Control, Compulsive Buying, And Real Debts. Journal of Economic

Psychology, 49, 141–149. https://doi.org/10.1016/j.joep.2015.04.003

Alkaraan, F.,

Elmarzouky, M., Hussainey, K., and Venkatesh, V. G. (2023). Sustainable Strategic Investment

Decision-Making Practices In UK Companies: The Influence Of Governance

Mechanisms On Synergy Between Industry 4.0 And Circular Economy. Technological

Forecasting and Social Change, 187, 122187. https://doi.org/10.1016/j.techfore.2022.122187

Amagir, A., Groot,

W., van den Brink, H. M., and Wilschut, A. (2020). Financial Literacy Of High School Students

In The Netherlands: Knowledge, Attitudes, Self-Efficacy, And Behavior.

International Review of Economics Education, 34, 100185. https://doi.org/10.1016/j.iree.2020.100185

Che Hassan, N.,

Abdul-Rahman, A., Ab. Hamid, S. N., and Mohd Amin, S. I. (2024). What Factors Affecting Investment

Decision? The Moderating Role Of Fintech Self-Efficacy. PLOS ONE, 19(4),

e0299004. https://doi.org/10.1371/journal.pone.0299004

Do, H. L., Vu, T. M.

P., Vu, N. M., Nguyen, D. T., and Tran, T. V. (2024). The Mediating Role Of Perceived

Behavioral Control On The Relationship Between Financial Knowledge And Saving

Intention: A Study Of Vietnamese University Students. Human Behavior,

Development and Society, 25(1). https://doi.org/10.62370/hbds.v25i1.270883

Harahap,

N. (2020).

Penelitian Kualitatif.

Herawati, N. T., Candiasa, I. M.,

Yadnyana, I. K., and Suharsono, N. (2018). Factors That Influence Financial Behavior

Among Accounting Students In Bali. International Journal of Business

Administration, 9(3), 30. https://doi.org/10.5430/ijba.v9n3p30

Moreno-Herrero, D.,

Salas-Velasco, M., and Sánchez-Campillo, J. (2018). Factors That Influence The Level Of

Financial Literacy Among Young People: The Role Of Parental Engagement And

Students’ Experiences With Money Matters. Children and Youth Services Review,

95, 334–351. https://doi.org/10.1016/j.childyouth.2018.10.042

Naiwen, L., Wenju,

Z., Mohsin, M., Rehman, M. Z. U., Naseem, S., and Afzal, A. (2021). The Role Of Financial Literacy And

Risk Tolerance: An Analysis Of Gender Differences In The Textile Sector Of

Pakistan. Industria Textila, 72(3), 300–308. https://doi.org/10.35530/IT.072.03.202023

Nasution,

A. F. (2023).

Metode Penelitian Kualitatif.

Nepal, R., Rajopadhyay, P.,

Rajopadhyay, U., and Bhattarai, U. (2023). Interplay Of Investor Cognition, Financial

Literacy, And Neuroplasticity In Investment Decision Making: A Study Of

Nepalese Investors. Journal of Business and Social Sciences Research, 8(2),

51–76. https://doi.org/10.3126/jbssr.v8i2.62133

Sajeev,

K. C., Afjal, M., Spulbar, C., Birau,

R., and Florescu, I. (2021). Evaluating The Linkage Between

Behavioural Finance And Investment Decisions Amongst Indian Gen Z Investors Using Structural

Equation Modeling. Revista de Stiinte

Politice, 72, 41–59.

Strömbäck, C.,

Lind, T., Skagerlund, K., Västfjäll, D., and Tinghög, G. (2017). Does Self-Control Predict Financial

Behavior And Financial Well-Being? Journal of Behavioral and Experimental

Finance, 14, 30–38. https://doi.org/10.1016/j.jbef.2017.04.002

Sulistyowati, A., Rianto, M. R.,

Handayani, M., and Bukhari, E. (2022). Pengaruh Financial Literacy, Return Dan

Resiko Terhadap Keputusan Investasi Generasi Milenial Islam Di Bekasi. Jurnal

Ilmiah Ekonomi Islam, 8(2), 2253. https://doi.org/10.29040/jiei.v8i2.5956

Tabassum,

S., Soomro, I. A., Ahmed, S., Alwi, S. K. K., and Siddiqui, I. H. (2021). Behavioral

Factors Affecting

Investment Decision-Making Behavior

In A Moderating Role Of

Financial Literacy: A Case Study Of Local Investors

Of Pakistan Stock Market. International Journal of Management, 12(2), 321–354.

Twumasi, M. A.,

Jiang, Y., Wang, P., Ding, Z., Frempong, L. N., and Acheampong, M. O. (2022). Does Financial Literacy Inevitably

Lead To Access To Finance Services? Evidence From Rural Ghana. Ciência Rural,

52(3), e20210112. https://doi.org/10.1590/0103-8478cr20210112

Vaghela, P. S.,

Kapadia, J. M., Patel, H. R., and Patil, A. G. (2023). Effect Of Financial Literacy And

Attitude On Financial Behavior Among University Students. Indian Journal of

Finance, 17(8), 43–57. https://doi.org/10.17010/ijf/2023/v17i8/173010

Widhiastuti, R. N., Harianti, A., Suryowati, B., and Suzuda, F. (2024). Penyuluhan Literasi Keuangan Untuk Mencapai Financial Freedom Bagi Gen-Z. Swadimas: Jurnal Pengabdian Kepada Masyarakat, 2(1), 8–12. https://doi.org/10.56486/swadimas.vol2no1.390

|

|

This work is licensed under a: Creative Commons Attribution 4.0 International License

This work is licensed under a: Creative Commons Attribution 4.0 International License

© IJETMR 2014-2026. All Rights Reserved.