|

|

|

|

Case Study

Assessing the Impact of Pradhan Mantri Jan Dhan Yojana (PMJDY) on Rural Digital Adoption: A Secondary Data Analysis

|

Mallikarjun

K. Chougala 1, Dr. Arun Babu Angadi 2 1 Assistant Professor, JSPM

University, Pune, Maharashtra, India 2 Assistant Professor, Karnataka Janapada

University, Gotagodi, Shiggaon, Haveri, Karnataka, India |

|

|

|

ABSTRACT |

||

|

Pradhan Mantri Jan Dhan Yojana (PMJDY) is the flagship financial inclusion programme of the Government of India and the foundation of the Jan Dhan–Aadhaar–Mobile (JAM) trinity. Over the last decade, PMJDY has expanded basic savings bank accounts to more than 55 crore beneficiaries, with around two-thirds of accounts located in rural and semi-urban areas. This paper assesses whether the rapid scaling-up of PMJDY has been associated with deeper digital adoption in rural India. Using exclusively secondary data from official sources such as the Ministry of Finance, Reserve Bank of India, Parliament documents, and the National Payments Corporation of India, supplemented by recent survey evidence and academic literature, the study constructs a consolidated data set for the period 2015–2025. Descriptive statistics and trend analysis are used to track the evolution of PMJDY accounts, deposits, RuPay card issuance and rural account shares alongside digital payment indicators such as the RBI Digital Payments Index and aggregate digital transaction volume. A simple correlation analysis for 2020–2025 indicates a very strong positive association between the growth in PMJDY accounts and the RBI-DPI, suggesting that expansion of basic accounts has moved broadly in tandem with the deepening of digital payments infrastructure and usage. However, evidence from rural UPI and AePS usage and from recent survey-based studies shows that gaps in digital literacy, connectivity and trust still constrain active digital use, especially among older and less educated rural account holders. The paper concludes that PMJDY has been a necessary but not sufficient condition for rural digital adoption; complementary investments in digital and financial literacy, cybersecurity safeguards and last-mile infrastructure remain critical for converting access into sustained usage. Keywords: PMJDY, Financial inclusion, Digital

payments, Rural India |

||

INTRODUCTION

Financial

inclusion has emerged as a core pillar of India’s inclusive growth strategy

over the past decade, with digital technology playing an increasingly central

role in extending formal financial services to underserved populations.

Launched in August 2014, Pradhan Mantri Jan Dhan Yojana (PMJDY) sought to

provide at least one basic savings bank account for every household, along with

access to remittances, credit, insurance and pension services at affordable

cost. On inauguration day alone, about 1.8 crore bank accounts were opened, a

feat recognised by the Guinness World Records, and by March 2015 the number of

PMJDY accounts had reached around 14.7 crore. Over time, the scheme has grown

into one of the world’s largest financial inclusion programmes, with more than

50 crore accounts by August 2023 and over 55 crore by

mid-2025, supported by a strong focus on rural and semi-urban geographies and

women beneficiaries.

Parallel to this

expansion in account ownership, India has witnessed a remarkable rise in

digital payments. The Reserve Bank of India’s Digital Payments Index (RBI-DPI),

which uses March 2018 as a base value of 100, rose to 395.57 by March 2023,

445.50 by March 2024 and 493.22 by March 2025, reflecting a more than fourfold

increase in digital payment activity since 2018. Over the same period, total

retail digital transactions expanded from about 2,338 crore

in 2018–19 to more than 16,000 crore transactions in 2023–24, driven

predominantly by the Unified Payments Interface (UPI), Aadhaar-enabled Payment

Systems (AePS) and card-based payments. These developments have positioned

India as a global leader in real-time digital payments and have redefined the

way households and micro-entrepreneurs transact.

Rural India has

been at the heart of both PMJDY and the broader digital payments revolution.

Approximately two-thirds of PMJDY accounts are located in rural and semi-urban

areas, and a substantial proportion of women beneficiaries reside in villages

and small towns. Business Correspondent (BC) networks, micro-ATMs, RuPay debit

cards and mobile-based platforms such as UPI and BHIM have created new

possibilities for accessing cash and conducting digital transactions in

locations that previously lacked brick-and-mortar banking outlets. Yet,

multiple studies and field reports highlight that access to an account does not

necessarily translate into regular, active digital usage. Account dormancy, low

transaction frequencies, patchy connectivity, and persistent gaps in digital

and financial literacy, especially among older and low-income rural households,

continue to constrain the transformative potential of digital finance.

Against this

backdrop, the question of whether PMJDY has primarily opened bank accounts or

whether it has also been a significant enabler of rural digital adoption

assumes policy relevance. While government documents emphasise the role of the

JAM trinity in facilitating Direct Benefit Transfers (DBT) and digital

payments, the empirical linkage between PMJDY expansion and measurable digital

adoption indicators remains under-explored. This paper addresses that gap by

systematically analysing secondary data on PMJDY account growth, deposits and

RuPay card issuance, alongside national and rural-focused metrics of digital

payments, with a particular focus on the period 2015–2025.

Research Problem

Most evaluations

of PMJDY emphasise its success in rapidly expanding basic bank account

ownership, particularly among rural and low-income households. However, far

less attention has been paid to whether these accounts are effectively

leveraged as gateways into the digital financial ecosystem. National-level

statistics on UPI, AePS and card usage show strong growth, but they rarely

disaggregate outcomes by type of account or explicitly link patterns of digital

adoption to PMJDY beneficiaries. At the same time, policy documents and

parliamentary discussions highlight concerns about account dormancy,

cybersecurity risks and uneven digital literacy among Jan Dhan account holders,

especially in rural areas.

The core research

problem addressed in this paper is therefore to assess the extent to which the

expansion of PMJDY has been associated with indicators of rural digital

adoption. Rather than attempting to establish strict causality, the study seeks

to map co-movements between PMJDY account metrics and digital payment

indicators, and to triangulate them with evidence from survey-based and

qualitative studies on rural digital usage. In doing so, it aims to move beyond

a binary view of access versus non-access and to shed light on how far PMJDY

has contributed to meaningful, digitally enabled financial inclusion.

Objectives

The specific

objectives of the study are as follows:

·

To trace

the growth of PMJDY accounts, deposits, RuPay debit cards and rural account

shares between 2015 and 2025 using secondary data.

·

To

analyse the evolution of key digital payment indicators in India—particularly

the RBI Digital Payments Index and aggregate digital transaction volumes—over

the same period.

·

To

examine secondary evidence on digital payment adoption in rural India,

including UPI and AePS usage, and relate these patterns to the PMJDY ecosystem.

·

To

synthesise insights from recent empirical and conceptual studies, including the

work of Dr. Shailesh Kediya and co-authors, on digital platforms, AI-driven

financial services and user behaviour, and draw implications for PMJDY-linked

digital adoption.

Literature Review

The literature on

PMJDY can broadly be grouped into three strands: evaluations of financial

inclusion outcomes, analyses of digital payment systems and rural inclusion,

and studies on technology-enabled financial services.

The first strand

focuses on the extent to which PMJDY has improved access to formal financial

services and altered household behaviour. Gupta

(2023) documents the historical evolution of PMJDY

and concludes that the scheme has been particularly effective in rural areas

because of the deeper penetration of public sector banks and Business

Correspondent networks. Gupta

and Gupta (2026) undertake a micro-level analysis in

Firozabad district and find that PMJDY has increased savings, reduced reliance

on informal moneylenders and facilitated timely receipt of subsidies through

Direct Benefit Transfer, especially for women beneficiaries. Several

commentaries from the Ministry of Finance and policy think tanks highlight that

PMJDY accounts have grown more than threefold since 2015 and that a large

majority of accounts are operative, but these documents typically do not delve

deeply into patterns of digital usage.

A related set of

studies investigates digital payments and financial inclusion in rural India. Vasudev

(2025) and other recent contributions examine how

platforms such as UPI, AePS and mobile wallets are reshaping transactional

behaviour in villages, emphasising the importance of Aadhaar-based

authentication, smartphone penetration and merchant onboarding. Studies

published in journals such as the International Journal of Professional Studies

and IRJMETS report that digital payments have improved account usage, smoothed

delivery of welfare schemes and enabled rural households to reduce travel costs

and time associated with cash-based transactions, although they also underscore

persistent constraints linked to connectivity, digital literacy and cyber risk.

Survey-based work on UPI adoption by rural users finds that perceived

usefulness, ease of use, trust and facilitating conditions significantly

influence behavioural intention to adopt digital payments, but adoption remains

uneven across remote and better-connected villages.

The third strand,

particularly relevant for this paper, explores the intersection of digital

technology, AI and financial services. Kediya and co-authors have contributed

to this emerging body of work in multiple ways. In a study published in the

Journal for ReAttach Therapy and Developmental Diversities, Kediya

et al. (2023) examine how AI and chatbot-based services

shape user psychology in banking and financial services, arguing that

well-designed conversational interfaces can enhance perceived service quality,

reduce friction and extend financial access to underserved segments. In another

paper presented at an international conference on communication, security and

artificial intelligence, Kediya

et al. (2023) propose a blockchain and proxy

re-encryption-based financial data sharing solution, highlighting how secure

data exchange architectures can build trust in digital financial ecosystems.

More recently, Kediya

et al. (2024) compare the performance and customer

satisfaction effects of chatbots in customer service, showing that AI-enabled

conversational tools can significantly improve response times and user

satisfaction when appropriately implemented. Singh et

al. (2023) extend the Technology Acceptance Model (TAM)

to study students’ acceptance of digital platforms across Indian states,

finding that perceived usefulness and perceived ease of use strongly predict

behavioural intention and actual usage.

Together, these

contributions reinforce three themes: first, that the availability of a

transaction account is only the starting point for financial inclusion; second,

that digital payments and AI-enabled service channels are increasingly central

to deepening usage; and third, that user perceptions of usefulness, ease of

use, trust and security critically shape adoption behaviour. However, few of

these studies explicitly connect PMJDY account metrics with national indices of

digital payment penetration or with rural-specific adoption indicators, which

motivates the present study.

Gap Analysis

Existing

scholarship provides rich insights into the functioning of PMJDY and the

broader digital payments ecosystem, but several gaps remain. First, most

PMJDY-focused studies either rely on cross-sectional surveys in specific

districts or summarise headline account and deposit figures; they rarely

integrate these metrics with longitudinal indicators of digital payment

penetration such as the RBI-DPI or aggregate digital transaction volumes.

Second, rural digital adoption studies often treat bank account ownership as a

control variable rather than explicitly distinguishing between PMJDY and

non-PMJDY accounts, even though the former are directly tied to government

initiatives and DBT flows. Third, while the literature on AI, chatbots and

digital platforms—including the work of Kediya and co-authors—highlights the

behavioural factors that drive technology acceptance, these insights have not

yet been systematically applied to the design and evaluation of PMJDY-linked

digital services for rural users.

Finally, there is

a paucity of secondary data-based studies that bring together official

administrative statistics, survey evidence and conceptual literature to

quantitatively and qualitatively assess how the PMJDY ecosystem interacts with

the evolving digital payments landscape. This paper addresses these gaps by

constructing a consolidated time-series data set for PMJDY and digital payment

indicators for 2015–2025, and by synthesising rural adoption evidence and

technology acceptance insights within a unified analytical framework.

Research Methodology

The study adopts a

descriptive and correlational research design based entirely on secondary data.

The primary quantitative variables include: (i) the number of PMJDY accounts

and associated deposit balances at selected time points, (ii) the share of PMJDY

accounts located in rural and semi-urban areas and the share held by women,

(iii) the number of RuPay debit cards issued to PMJDY account holders, (iv) the

RBI Digital Payments Index (RBI-DPI) for March of each year from 2018 to 2025,

and (v) aggregate digital transaction volumes in India between 2018–19 and

2023–24. PMJDY figures are drawn from Ministry of Finance press releases, the

“Nine Years of PMJDY” status document, and parliamentary replies on PMJDY

account statistics. RBI-DPI values and digital transaction volumes are taken

from RBI press releases and derivative reports, while rural digital adoption

indicators are sourced from EY–CII’s 2024 report on financial inclusion through

technology and literacy and from peer-reviewed studies on UPI adoption in rural

India.

Data were collated

into a structured spreadsheet and cross-checked across multiple sources

wherever possible. For PMJDY accounts and deposits, the analysis uses March-end

figures for 2015 and 2021–2025, supplemented by technical reports which

document that PMJDY accounts reached about 38.07 crore by March 2020. For the

RBI-DPI, the study uses March values from 2018 to 2025, treating March 2018 as

the base year (index value = 100). A simple compound annual growth rate (CAGR)

was calculated for PMJDY account growth between 2015 and 2025, and Pearson’s

correlation coefficient was computed for the relationship between PMJDY

accounts and the RBI-DPI over the overlapping period 2020–2025. The resulting

data sets were visualised using line and bar charts to facilitate

interpretation.

In addition to

quantitative analysis, the study conducts a narrative synthesis of qualitative

and survey-based evidence on rural digital payment adoption, drawing on studies

of UPI usage in rural India, AePS transactions through Business Correspondents

and technology acceptance research focusing on digital platforms and AI-enabled

financial services. This mixed secondary-data approach enables the paper to

triangulate statistical trends with user-level insights and to identify

structural and behavioural constraints that may decouple account ownership from

active digital usage. No primary data collection was undertaken, and the

analysis is limited by the granularity and frequency of data published in the

public domain.

Data Presentation and Analysis

Table 1

|

Table 1 Presents the Evolution

of PMJDY Accounts and Deposit Balances at Selected March year-ends Between

2015 and 2025 |

||

|

Year

(March) |

PMJDY

accounts (crore) |

Deposits

(₹ crore) |

|

2015 |

14.72 |

15,670 |

|

2020 |

38.07 |

|

|

2021 |

42.2 |

1,45,551 |

|

2022 |

45.06 |

1,66,459 |

|

2023 |

48.65 |

1,98,844 |

|

2024 |

51.95 |

2,32,502 |

|

2025 |

55.18 |

2,60,387 |

Between March 2015

and March 2025, the number of PMJDY accounts increased from approximately 14.72

crore to 55.18 crore. This implies a compound annual growth rate of roughly

14.1 percent over the decade. Over the same period, reported deposits in PMJDY accounts

rose from about ₹15,670 crore in March 2015 to more than ₹2.60 lakh

crore by March 2025, indicating that many accounts have transitioned from

dormant status to active savings and transaction use. Furthermore,

parliamentary data show a steady increase in the share of women account holders

and sustained dominance of rural and semi-urban locations, where roughly

two-thirds of PMJDY accounts are concentrated.

|

Table 2 |

|

Table 2 Summarises the Co-Movement

of PMJDY Accounts and the RBI Digital Payments Index (RBI-DPI) for the Period

2020–2025 |

||

|

Year

(March) |

PMJDY

accounts (crore) |

RBI-DPI

(index) |

|

2020 |

38.07 |

207.84 |

|

2021 |

42.2 |

270.59 |

|

2022 |

45.06 |

349.3 |

|

2023 |

48.65 |

395.57 |

|

2024 |

51.95 |

445.5 |

|

2025 |

55.18 |

493.22 |

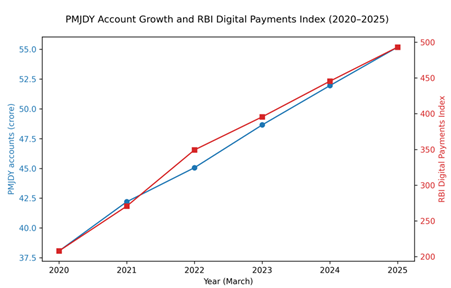

A simple

correlation analysis using these annual March observations yields a Pearson

correlation coefficient of 0.995 between PMJDY account counts and the RBI-DPI

for 2020–2025. While correlation does not imply causation, the near-perfect

positive association suggests that the period of rapid PMJDY expansion has

overlapped closely with the deepening of digital payments infrastructure and

usage captured by the RBI-DPI. This pattern is consistent with the view that a

broad-based base of transaction accounts, combined with the JAM architecture,

has facilitated the scaling up of digital payments, even though other factors

such as smartphone penetration, merchant acceptance infrastructure and policy

nudges also play significant roles.

|

Table 3 |

|

Table 3 Shows the Change

in Aggregate Digital Transaction Volumes in India between 2018–19 and 2023–24 |

|

|

Financial

year |

Digital

transactions (crore) |

|

2018-19 |

2,338 |

|

2023-24 |

16,443 |

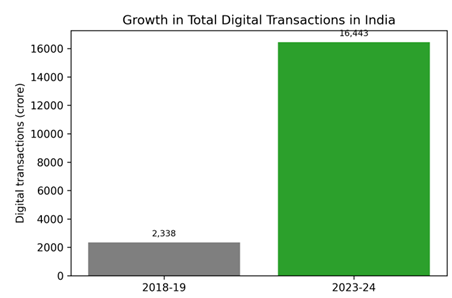

Official data

indicate that total digital transactions in India increased from about 2,338 crore in 2018–19 to approximately 16,443 crore

in 2023–24. This more than sevenfold increase reflects both the rapid adoption

of UPI and the expansion of card, AePS and other digital channels. The period

of steepest growth coincides with sustained increases in PMJDY account balances

and the maturation of the JAM ecosystem, suggesting reinforcing dynamics

between account-based financial inclusion and digital transaction behaviour.

|

Figure 1

|

|

Figure 1 Plots the Joint

Evolution of PMJDY Accounts and the RBI-DPI for the Period 2020–2025 |

|

Figure 2

|

|

Figure 2 Illustrates the

Increase in Aggregate Digital Transaction Volumes Between 2018–19 and 2023–24 |

Beyond national

aggregates, survey and administrative data provide insights into rural digital

adoption. EY and the Confederation of Indian Industry (CII) report that by

2024, the Unified Payments Interface (UPI) had become the most preferred mode

of transaction for nearly 38 percent of respondents in rural and semi-urban

India, even though around 86 percent of account holders in these areas still

expressed a preference for visiting bank branches. Studies on UPI usage in

rural regions find that adoption is higher in semi-rural areas with better

connectivity and market linkages, while remote villages continue to rely

heavily on cash due to network issues and low digital literacy. Administrative

data on AePS transactions show sustained volumes of cash withdrawals and

balance enquiries through BC-operated micro-ATMs in rural areas, underscoring

the importance of biometric, Aadhaar-linked channels for low-literacy users.

Taken together, these patterns suggest that PMJDY has created a broad base of

rural account holders who can, in principle, use digital payment channels, but

that the actual mix of digital and cash usage varies widely across contexts.

Discussion

The empirical

analysis indicates that PMJDY has achieved sustained growth in account

ownership and deposit balances over the last decade, with particularly strong

gains between 2015 and 2025. The CAGR of roughly 14 percent in account numbers

and the manifold increase in balances reflect both continued enrolment and

greater utilisation of accounts for savings and transactions. The high and

persistent share of rural and semi-urban accounts and the over-representation

of women among beneficiaries point to a deliberate targeting of historically

excluded segments. At the same time, the near-linear rise in the RBI-DPI and

the sharp increase in digital transaction volumes suggest that India’s payments

infrastructure and user base have undergone a structural transformation during

the same period.

The very strong

positive correlation between PMJDY account counts and the RBI-DPI over

2020–2025 should be interpreted with caution, but it is nonetheless

informative. It implies that the years in which PMJDY accounts and balances

grew most rapidly were also the years in which digital payment penetration and

performance deepened the most. From a conceptual standpoint, this is consistent

with the idea that transaction accounts, combined with unique digital identity

and mobile phones, form the foundational rails on which digital payment

ecosystems run. PMJDY accounts have served as the primary receptacle for DBT

flows, which in turn may encourage beneficiaries to engage with digital

channels—either directly through UPI and RuPay cards or indirectly through AePS

and BC-assisted transactions.

However, the

rural-focused literature and survey evidence also underscore important

frictions. Many rural PMJDY beneficiaries, particularly older women and

low-literacy users, prefer assisted modes of transaction and cash withdrawals

over independent use of UPI or merchant QR payments. Concerns about fraud, data

privacy and biometric misuse, as discussed in recent work on cybersecurity

risks in PMJDY digital transactions, can dampen willingness to adopt fully

digital usage patterns. The Technology Acceptance Model-based study by Singh et

al. and the AI and chatbot research by Kediya and co-authors highlight the

importance of perceived usefulness, ease of use, trust and service quality in

shaping attitudes towards digital platforms. These findings suggest that

strengthening user-centric design, grievance redressal and cybersecurity, and

embedding financial and digital literacy into PMJDY outreach, are critical for

translating account ownership into meaningful digital inclusion.

Findings

·

PMJDY

accounts expanded from about 14.72 crore in March 2015 to 55.18 crore in March

2025, with a compound annual growth rate of roughly 14.1 percent and a

parallel, multi-fold increase in deposits.

·

Throughout

the period, roughly two-thirds of PMJDY accounts were located in rural and

semi-urban areas and a majority were held by women, confirming the scheme’s

strong rural and gender focus.

·

The RBI

Digital Payments Index rose steadily from 207.84 in March 2020 to 493.22 in

March 2025, and correlation analysis shows a very strong positive association

between PMJDY account growth and the RBI-DPI over this period.

·

Aggregate

digital transaction volumes in India increased more than sevenfold between

2018–19 and 2023–24, driven largely by UPI and supported by RuPay cards and

AePS, indicating rapid mainstreaming of digital payments.

·

Secondary

evidence on rural UPI and AePS usage reveals that while digital adoption has

deepened in many rural and semi-urban areas, significant disparities persist

across villages and user segments due to connectivity constraints, literacy

gaps and trust deficits.

·

Insights

from the work of Dr. Shailesh Kediya and co-authors on AI, chatbots and digital

platform adoption underline that user perceptions of usefulness, ease of use,

security and service quality are crucial determinants of digital financial

adoption, with direct relevance for the design of PMJDY-linked digital

services.

Conclusion

This paper has

assessed the impact of Pradhan Mantri Jan Dhan Yojana on rural digital adoption

using a secondary data-based approach that links PMJDY account and deposit

trends with national indices of digital payment penetration and rural digital

usage evidence. The analysis shows that PMJDY has been instrumental in rapidly

expanding the base of transaction accounts among rural and low-income

households and that this expansion has occurred alongside, and in close

association with, the deepening of India’s digital payments ecosystem. Yet, the

persistence of account dormancy in some segments, the continued reliance on

cash and assisted channels, and reported concerns around cybersecurity and data

privacy indicate that access alone is insufficient for achieving full digital

inclusion.

From a policy

perspective, the findings support a two-pronged strategy. On the one hand,

PMJDY and related schemes should continue to focus on saturating account

coverage, maintaining low-cost access and ensuring that DBT flows are reliably

delivered through formal channels. On the other hand, there is a need to

systematically integrate digital and financial literacy initiatives,

user-centric design of digital interfaces (including AI-driven conversational

tools), and robust cybersecurity safeguards into the PMJDY ecosystem,

particularly in rural and remote areas. Future research could build on this

study by exploiting more granular transaction-level data, conducting

mixed-methods fieldwork to capture user experiences in specific districts, and

applying behavioural frameworks such as TAM and related models to better

understand the determinants of sustained digital usage among PMJDY

beneficiaries. Such work would further illuminate how PMJDY can continue to

evolve from a bank account opening scheme into a cornerstone of inclusive,

secure and trusted digital finance for rural India.

ACKNOWLEDGMENTS

None.

REFERENCES

Das,

A. (2021).

Regulating Basic Savings Bank Deposit Accounts: Do We

Need to Care for these Marginalized Depositors? IIT

Bombay Technical Report.

EY, and Confederation of Indian Industry. (2024). Financial Inclusion Through Technology and Literacy in India: Strategies for Sustainable Growth. EY-CII.

Gupta, K. (2023). Pradhan Mantri Jan Dhan Yojana: History and Present Impact. South Asian Journal of Social Studies and Economics, 19(2), 21–27. https://doi.org/10.9734/sajsse/2023/v19i2674

Gupta,

S., and Gupta, P. (2026). Socio-Economic Impact of Pradhan Mantri Jan Dhan Yojana:

A Micro-Level Analysis in Firozabad. Advances in Consumer Research, 3(2),

1618–1634.

Kediya, S., Dhote, S., Singh, D. K., Bidve, V. S., Pathan, S., and Suchak, A. (2023). Are AI and Chatbots Services Affecting the Psychology of users in Banking Services and Financial Sector. Journal for ReAttach Therapy and Developmental Diversities, 6(9s2), 191–197.

Kediya, S., Chib, S., Chouhan, N., Sharma, A., Vinchurkar, S., and Parekh, K. (2023). Blockchain and Proxy Re-Encryption Technology-Based Financial Data Sharing Solution. In Proceedings of the International Conference on Communication, Security and Artificial Intelligence. https://doi.org/10.1109/ICCSAI59793.2023.10421524

Kediya, S., Mohanty, V., Gurjar, A., Chouhan, N., Sharma, R., and Golar, P. (2024). Chatbots in Customer Service: A Comparative Analysis of Performance and Customer Satisfaction. In Proceedings of the 2nd DMIHER International Conference on Artificial Intelligence in Healthcare. https://doi.org/10.1109/IDICAIEI61867.2024.10842848

Kumari, B., and Singh, A. (2025). Cybersecurity Risks and Data Privacy Concerns in PMJDY Digital Transactions. Electrical and Electronic Engineering and Technology, 15(2), 4725–4745. https://doi.org/10.52783/eel.v15i2.3323

Ministry

of Finance. (2020).

Pradhan Mantri Jan-Dhan Yojana (PMJDY): National

Mission for Financial Inclusion Completes Six Years of Successful

Implementation. Press Information Bureau, Government of India.

Ministry

of Finance. (2021).

Pradhan Mantri Jan-Dhan Yojana (PMJDY): National

Mission for Financial Inclusion Completes Seven Years of Successful

Implementation. Press Information Bureau, Government of India.

Ministry

of Finance. (2023).

Nine Years of Pradhan Mantri Jan-Dhan Yojana (PMJDY). Department of Financial

Services, Government of India.

Ministry

of Finance. (2024).

Pradhan Mantri Jan Dhan Yojana (PMJDY) (Press Release, August 13, 2024). Press

Information Bureau, Government of India.

Ministry

of Finance. (2025).

Eleven Years of PM Jan Dhan Yojana: Banking the

Unbanked. Press Information Bureau, Government of India.

Reserve

Bank of India. (2024). RBI-Digital Payments Index for March 2024 (Press release).

Reserve

Bank of India. (2025). RBI-Digital Payments Index for March 2025 (Press release).

Sharma,

S. V., et al. (2025).

Digital Payments and Financial Inclusion in Rural India. International Journal

of Professional Studies, 5(4), 45–60.

Singh,

D. K., Kediya, S., Band, G., and Shukla, S. (2023). An Insight into Students' Acceptance of

Various Digital Platforms Using TAM Model Across the Indian States During the

Pandemic. Academy of Marketing Studies Journal, 27(5), 1–16.

Vasudev, S. (2025). Digital Payments and Financial Inclusion in Rural India. International Journal of Professional Studies, 5(4), 1–20.

|

|

This work is licensed under a: Creative Commons Attribution 4.0 International License

This work is licensed under a: Creative Commons Attribution 4.0 International License

© IJETMR 2014-2026. All Rights Reserved.