|

|

|

|

An Efficient Compromised Imputation Method for Estimating Population Mean

Sandeep Mishra 1 ![]()

![]()

1 Association of Indian Universities, New Delhi, India

|

|

|

ABSTRACT |

|

|

This paper

suggests a modified new ratio-product-exponential imputation procedure to

deal with missing data in order to estimate a finite

population mean in a simple random sample without replacement. The bias and

mean squared error of our proposed estimator are obtained to the first degree

of approximation. We derive conditions for the parameters under which the

proposed estimator has smaller mean squared error than the sample mean,

ratio, and product estimators. We carry out an empirical study which shows

that the proposed estimator outperforms the traditional estimators using real

data. |

|||

|

Received 16 July 2022 Accepted 19 August 2022 Published 05 September 2022 Corresponding Author Sandeep

Mishra, smisra1983@yahoo.co.in DOI10.29121/ijetmr.v9.i9.2022.1216 Funding: This research

received no specific grant from any funding agency in the public, commercial,

or not-for-profit sectors. Copyright: © 2022 The

Author(s). This work is licensed under a Creative Commons

Attribution 4.0 International License. With the

license CC-BY, authors retain the copyright, allowing anyone to download,

reuse, re-print, modify, distribute, and/or copy their contribution. The work

must be properly attributed to its author.

|

|||

|

Keywords: Missing Data,

Mean Square Error, Imputation, Bias, Ratio Estimator |

|||

1. INTRODUCTION

Imputation means

replacing a missing value with another value based on a reasonable estimate.

Information on the related auxiliary variable is generally used to recreate the

missing values for completing datasets. Incomplete data is usually categorized

into three different response mechanisms: Missing Completely at Random (MCAR);

Missing at Random (MAR); and Missing Not at Random (MNAR or NMAR) Little and Rubin (2002). Missing completely at random (MCAR): Missing

data are randomly distributed across the variable and unrelated to other

variables. Missing at random (MAR): Missing data are not randomly distributed

but they are accounted for by other observed variables. Missing not at random

(MNAR): Missing data systematically differ from the observed values. From the

above-mentioned classifications of missing data, we, in the present study, have

assumed MCAR.

Auxiliary

information is important for survey practitioner as it is utilized to improve

the performance of the methods. It may be utilized at the design stage or the

estimation stage of the survey to get the more efficient estimator. At

estimation stage ratio, product and regression methods are traditionally used. Bhal

and Tuteja (1991) introduced

exponential ratio and product estimator for estimation of population mean. Many

modifications have been proposed using these methods till date. For handling

missing data on the study variable several extensions and developments were

proposed in the literature. Singh (2003) suggested

product estimation for imputation. Shakti Prasad (2018) adapts exponential

product type estimator given by Bahal and Tuteja (1991) and

proposed exponential estimators for imputation. Kadilar and Cingi (2008) investigated some ratio-type imputation

methods and proposed three new estimators to overcome the problem of the

missing data. Diana and Perri (2010)

proposed three regression type estimators which were

more efficient than the Kadilar and Cingi (2008). The

present article suggests a general ratio product exponential type method of

imputation and accordingly proposed three estimators using the different amount

of available auxiliary information as utilized by Ahmad

et al. (2006), Kadilar and Cingi (2008), and Diana and Perri (2010). The proposed methods are

than compared by traditional procedure of imputation. The proposed estimators

come out to be more efficient than the usual ratio, product, regression, and

exponential method for handling missing observations to estimate the population

mean.

Given a finite population ![]() ,

the objective is to estimate the

population mean

,

the objective is to estimate the

population mean ![]() . A

simple random sample wor,

. A

simple random sample wor, ![]() ,

of size

,

of size ![]() is drawn from the population

is drawn from the population ![]() .

Let the responding units be

.

Let the responding units be ![]() from the

from the ![]() sampled units. Let us denote

sampled units. Let us denote ![]() as the set of responding units and

as the set of responding units and ![]() the set of non-responding units, i.e.,

the set of non-responding units, i.e., ![]() is observed for

is observed for ![]() but for units in

but for units in ![]() the values are not available and hence imputed

values are derived by some method. In this paper we shall use the following

notations:

the values are not available and hence imputed

values are derived by some method. In this paper we shall use the following

notations:

![]() : Population

Size;

: Population

Size; ![]() Sample size;

Sample size; ![]() : Number of

responding units;

: Number of

responding units; ![]() : Population

means of study variate

: Population

means of study variate ![]() and auxiliary variate

and auxiliary variate ![]() respectively;

respectively; ![]() : Standard Deviation of study variate

: Standard Deviation of study variate ![]() and auxiliary variate

and auxiliary variate ![]() respectively;

respectively; ![]() : Coefficient

of variation of study variate

: Coefficient

of variation of study variate ![]() and auxiliary variate

and auxiliary variate ![]() respectively;

respectively; ![]() : Correlation

coefficient between

: Correlation

coefficient between ![]() and

and ![]() ;

; ![]() .

.

2. Some

existing methods of imputation

1)

The mean method of imputation suggests replacing the

missing observations with the mean of the observations available on response

units i.e.

Then the estimator of the population mean ![]() is given by

is given by

![]() and its MSE is given by

and its MSE is given by

![]() (1.1)

(1.1)

2)

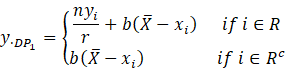

The ratio method of imputation uses information on one auxiliary

variable ![]() and calculates the missing values by

and calculates the missing values by

![]()

Where ![]()

This gives the resulting estimator by

![]()

The MSE of ![]() is given by

is given by

![]() (1.2)

(1.2)

It is noted that, in the presence of missing data, the

availability of information on auxiliary variable ![]() in the data set supports

suggesting efficient estimators.

in the data set supports

suggesting efficient estimators.

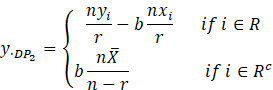

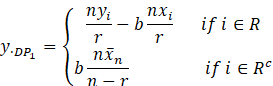

3) Diana

and Perri (2010) proposed three estimators as by using different regression-type

method of imputation such that the imputed data is given by

For these

methods the resulting estimators are

![]()

![]()

![]()

![]() (1.2)

(1.2)

![]() (1.3)

(1.3)

![]() (1.4)

(1.4)

They proved

that the suggested estimators are more efficient than the Kadilar and Cingi (2008) estimators. ![]() is always more efficient

than both

is always more efficient

than both ![]() and

and ![]() , whereas

, whereas ![]() perform better than

perform better than ![]() if the condition

if the condition

![]()

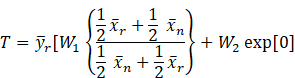

3. The proposed Estimator

With the above

imputation method, the resulting estimator of the population mean ![]() is obtained as

is obtained as

(2.1)

(2.1)

![]() and

and ![]() are constant chosen

suitably so that their choice minimizes the mean square error of the resultant

estimator and

are constant chosen

suitably so that their choice minimizes the mean square error of the resultant

estimator and ![]() is a real constant. Our

goal in this paper is to discuss the suggested estimators for different values

of

is a real constant. Our

goal in this paper is to discuss the suggested estimators for different values

of ![]() and have a comparative

study of the suggested estimator for these values of

and have a comparative

study of the suggested estimator for these values of ![]() in order

to get the minimum MSE.

in order

to get the minimum MSE.

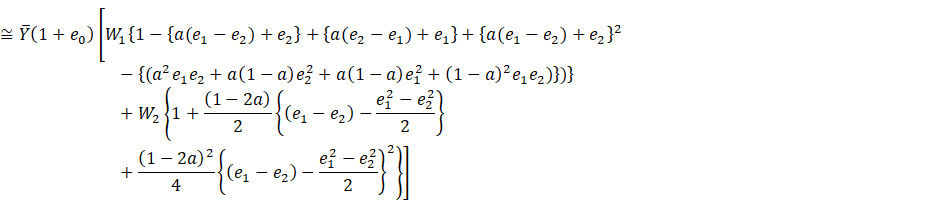

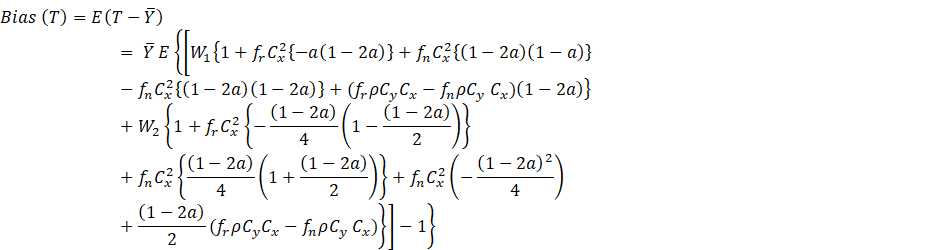

4. First

Degree Approximation to the Bias

To derive the Bias and MSE expressions of the proposed estimator ![]() upto

upto ![]() , we define

, we define

![]()

Thus, we have ![]()

The expectation of these ![]() are

are ![]()

And under simple random sampling without replacement,

![]()

![]()

where ![]() ,

, ![]()

![]() .

. ![]()

Now representing (2.1) in terms of ![]() , we have

, we have

![]()

We assume that the sample is large enough to make ![]() and

and ![]() so small that contributions from powers of

degree higher than two are negligible. By retaining powers up to

so small that contributions from powers of

degree higher than two are negligible. By retaining powers up to ![]() and

and ![]() , we get

, we get

(2.2)

(2.2)

Theorem 2.1. The

conditional bias up to the first order of approximation of the estimator ![]() is given by the estimator

is given as

is given by the estimator

is given as

![]()

Where ![]() and

and ![]()

Proof: From (2.2) we have

(2.3)

(2.3)

Taking expectation on both side we obtain the bias of ![]() to order

to order ![]() as

as

(2.4)

(2.4)

Letting ![]() ,

, ![]() in eq. (A.1)

in eq. (A.1)

![]()

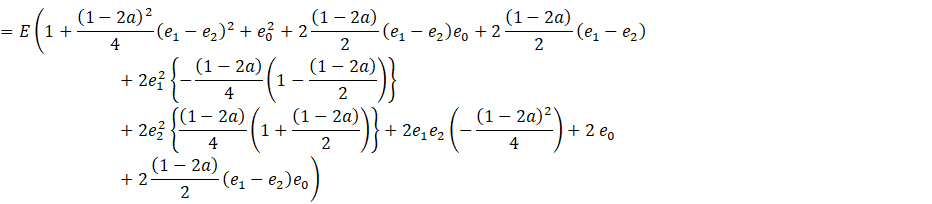

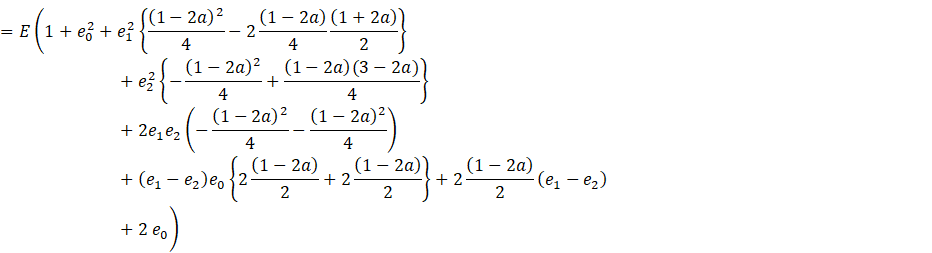

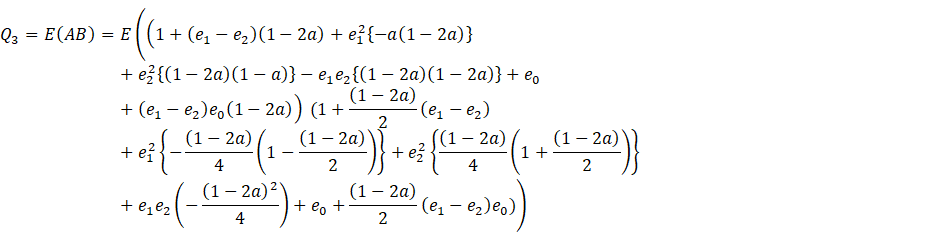

5. Mean

Squared Error of T

We calculate the mean squared error of ![]() up to order

up to order ![]() by

squaring (2.2) and retaining terms up to squares in

by

squaring (2.2) and retaining terms up to squares in ![]() and

and ![]() , and then

taking the expectation. This yields the first-degree approximation of the MSE

, and then

taking the expectation. This yields the first-degree approximation of the MSE

Theorem 2.2. The minimum mean square

error of the proposed estimator ![]() is given by

is given by

![]()

The optimum values of ![]() and

and ![]() are:

are:

![]()

Where

![]()

![]()

, ![]()

![]()

![]()

And the minimum MSE of the proposed estimator

is given by

![]()

Proof:

(A.2)

(A.2)

Let coefficient

of ![]() and

and ![]() in eq. (A.2) are

in eq. (A.2) are ![]() and

and ![]() respectively then

respectively then ![]() is

is

![]()

![]()

![]() (2.5)

(2.5)

Now, let

![]()

![]()

![]()

![]()

![]()

![]()

![]()

From

previous theorem

![]() ,

,

Placing these values of ![]() in (A.2) we get

in (A.2) we get

![]()

![]()

Differentiating MSE with respect to ![]() and

and ![]() ,

and equating to zero, we get

,

and equating to zero, we get

![]()

![]()

On

solving these equations, we get

![]()

And

after placing the values of ![]() and

and ![]() from () to the expression

of MSE (?) the minimum MSE expression is

from () to the expression

of MSE (?) the minimum MSE expression is

![]()

6. Expressions of MSE for different choices of ![]()

Here we consider the

different forms of the proposed estimator for various values of ![]() .

.

Case 1. ![]()

![]()

![]()

![]()

![]()

![]()

![]() ,

, ![]()

![]()

![]()

![]()

![]()

Which is better

than the mean estimator ![]() in terms of efficiency as

in terms of efficiency as

![]()

And if ![]() , The proposed estimator

at

, The proposed estimator

at ![]() is equivalent to the mean

estimator

is equivalent to the mean

estimator![]()

Case 2. ![]()

![]()

![]()

![]()

![]()

, ![]()

![]()

![]()

![]()

![]()

For ![]()

![]()

![]()

![]()

![]()

For ![]()

![]()

![]()

![]()

Case 3. ![]()

![]()

A linear

combination of product estimator and product type exponential estimator,

![]() ,

, ![]()

![]()

![]()

![]()

![]()

, ![]()

![]()

![]()

and further

For ![]() it reduces to product

estimator

it reduces to product

estimator

![]()

![]()

![]()

and for ![]() it reduces to product type exponential estimator

it reduces to product type exponential estimator

![]()

![]()

![]()

![]()

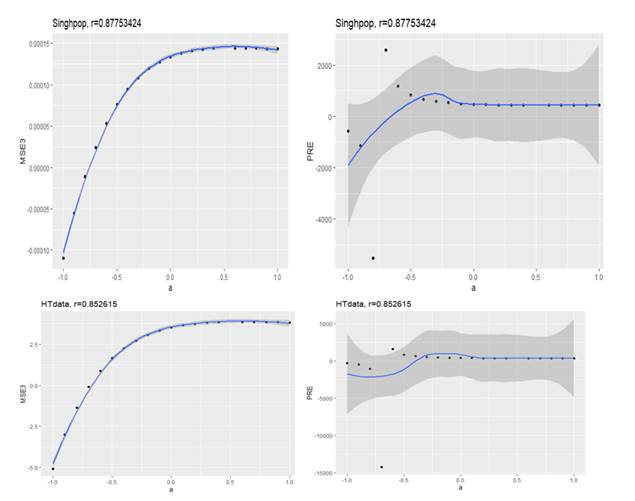

For the purpose of

comparison of the proposed estimator we conducted the empirical study and

computed the Percentage relative efficiency (PRE) of the estimators ![]() ,

, ![]() ,

, ![]() for (i) real data and (ii) artificially generated data.

for (i) real data and (ii) artificially generated data.

The empirical study has been carried out to

illustrate and compare the performance of the proposed imputation methods with

the existing conventional imputation methods and the method proposed by Diana and Perri (2010) and Bhushan and Pandey (2010) utilizing Searl () constant with the Diana and Perri (2010)

estimator for

(i) real data described in Horvitz

and Thompson (1952), Singh (2003), described in Table 1, Table 2.

Table 1

|

Table 1 Description of Populations considered

for empirical study |

||

|

Population 1 |

Population 2 |

|

|

Description |

Horvitz and Thompson (1952),

|

Singh (2003, pp 1114), the

season-average price for commercial crop: season average price in $ per pound,

by states,1994-96; |

|

|

20 |

36 |

|

|

7 |

18 |

|

|

5 |

8 |

|

|

21.15 |

0.2033 |

|

|

19.7 |

0.1856 |

|

|

94.028947 |

0.006458 |

|

|

61.8 |

0.005654 |

|

|

0.8526154 |

0.8775 |

2)

Ratio Method of imputation, ![]()

3)

Diana and Perri method of imputation ![]()

4)

Diana and Perri method of imputation ![]()

5)

Diana and Perri method of imputation ![]()

6)

Proposed method of imputation, ![]()

![]()

Table 2

|

Table 2 Mean square error and percent relative

efficiency based on Population I(Singhpop) |

|||||

|

Estimator |

MSE |

PRE |

MSE |

PRE |

|

|

|

0.000627874 |

100 |

14.1043421 |

100 |

|

|

|

0.00029219 |

214.8858518 |

10.2000587 |

138.2771 |

|

|

|

0.00048973 |

128.2082427 |

7.75712694 |

181.8243 |

|

|

|

0.000144369 |

434.9080453 |

3.85114837 |

366.2373 |

|

|

|

0.000282514 |

222.2456233 |

10.1983635 |

138.3001 |

|

|

|

|

MSE

and PRE of Proposed Estimator for different choices of |

|||

|

-1 |

*-0.000109667 |

*-572.5264505 |

*-5.07540636 |

*-277.8958 |

|

|

-0.9 |

*-5.54806E-05 |

*-1131.701446 |

*-2.98949277 |

*-471.7972 |

|

|

|

-0.8 |

*-1.13765E-05 |

*-5519.055982 |

*-1.36603234 |

*-1032.5043 |

|

-0.7 |

2.43566E-05 |

2577.844737 |

*-0.09897433 |

*-14250.5046 |

|

|

-0.6 |

5.31303E-05 |

1181.763804 |

0.89001809 |

1584.7253 |

|

|

-0.5 |

7.61179E-05 |

824.8708681 |

1.66003196 |

849.6428 |

|

|

-0.4 |

9.4301E-05 |

665.8194857 |

2.25644120 |

625.0702 |

|

|

-0.3 |

0.000108506 |

578.656658 |

2.71463222 |

519.5673 |

|

|

-0.2 |

0.00011943 |

525.7257808 |

3.06257328 |

460.5389 |

|

|

-0.1 |

0.000127667 |

491.8054912 |

3.32262502 |

424.4939 |

|

|

0 |

0.000133722 |

469.5370246 |

3.51284069 |

401.5082 |

|

|

0.1 |

0.000138025 |

454.8999563 |

3.64791560 |

386.6411 |

|

|

0.2 |

0.000140943 |

445.4819583 |

3.73989064 |

377.1325 |

|

|

0.3 |

0.000142789 |

439.7214493 |

3.79868012 |

371.2959 |

|

|

0.4 |

0.00014383 |

436.5391782 |

3.83247219 |

368.0220 |

|

|

0.5 |

NaN |

#VALUE! |

NaN |

- |

|

|

0.6 |

0.000144359 |

434.9406963 |

3.85095252 |

366.2559 |

|

|

0.7 |

0.00014419 |

435.4483623 |

3.84580584 |

366.7461 |

|

|

0.8 |

0.000143911 |

436.2925635 |

3.83631355 |

367.6535 |

|

|

0.9 |

0.00014362 |

437.1774822 |

3.82543836 |

368.6987 |

|

|

1 |

0.000143389 |

437.8833031 |

3.81546698 |

369.6623 |

|

8. Interpretations of the computational results

The

following interpretations may be read out from above Tables:

1) For the real

populations, HT data and Singh Population where the correlation between ![]() and

and ![]() is 0.852615 and 0.877534, the results are

shown in Table 1. It is clear that the proposed imputation method

is 0.852615 and 0.877534, the results are

shown in Table 1. It is clear that the proposed imputation method ![]() is superior to all the imputation methods i.e.,

is superior to all the imputation methods i.e.,

![]() and the

imputation methods suggested by Diana and Perri

and the

imputation methods suggested by Diana and Perri ![]() for a wide choice of the constant

for a wide choice of the constant ![]() for the proposed estimator.

for the proposed estimator.

CONFLICT OF INTERESTS

None.

ACKNOWLEDGMENTS

None.

REFERENCES

Heitjan, D.F. and Basu, S. (1996). Distinguishing 'Missing at Random' and 'Missing Completely at Random'. The American Statistician. 50(3), 207-213. https://doi.org/10.1080/00031305.1996.10474381.

Horvitz, D. G. and Thompson, D.J. (1952). A Generalization of Sampling Without Replacement From a Finite Universe. Journal of the American Statistical Association, 47(260), 663-685. https://doi.org/10.1080/01621459.1952.10483446.

Lee, H., Rancourt, E., and Sarndal, C.E. (1994). Experiments with Variance Estimation from Survey Data with Imputed Values. Journal of Official Statistics,10(3),231-243.

Rubin, R. B. (1978). Multiple Imputation for Nonresponse in Surveys. New York : John Wiley.

Singh, S. (2003). Advanced Sampling Theory with Applications. How Michael Selected Amy. Kluwer, Dordrecht, 1(2). https://doi.org/10.1007/978-94-007-0789-4.

Singh, S. and Horn, S. (2000). Compromised Imputation in Survey Sampling. Metrika, 51, 267-276. https://doi.org/10.1007/s001840000054.

|

|

This work is licensed under a: Creative Commons Attribution 4.0 International License

This work is licensed under a: Creative Commons Attribution 4.0 International License

© IJETMR 2014-2022. All Rights Reserved.